With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

It was in early 2021 that Congressional Democrats passed & President Biden signed the American Rescue Plan Act (ARPA), which among other things dramatically expanded & enhanced the original premium subsidy formula of the Affordable Care Act, finally bringing the financial aid sliding income scale up to the level it should have been in the first place over a decade earlier.

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

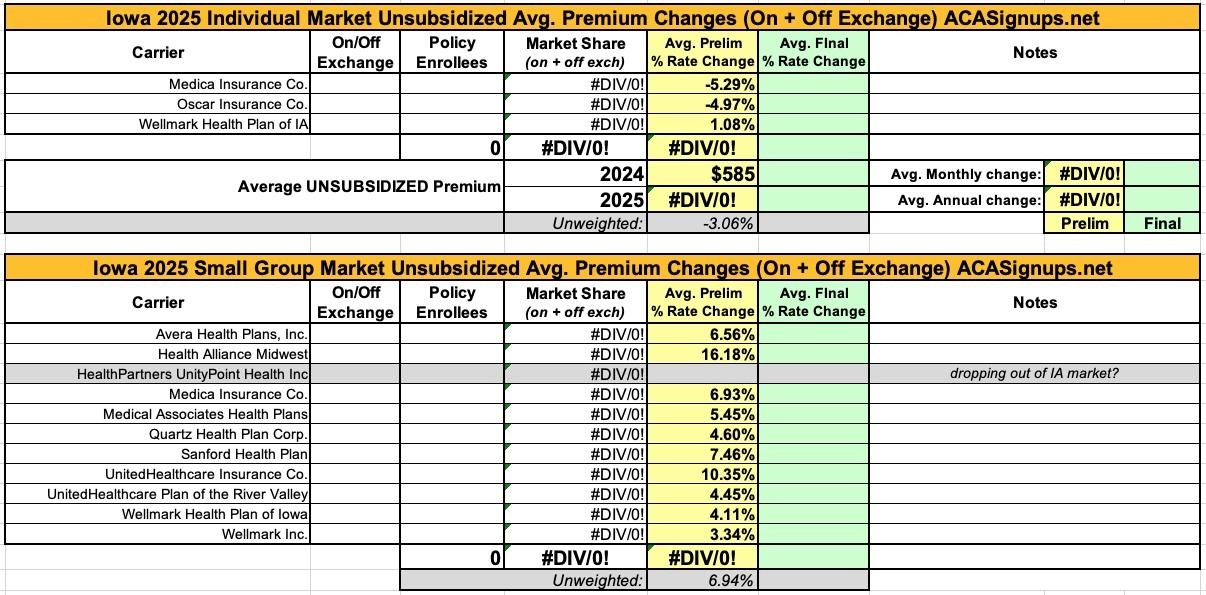

Here's the preliminary 2025 ACA individual and small group market rate filings. Unfortunately, the effectuated enrollment isn't available this year for the carriers in either market, so I can only offer unweighted averages...which include a 3.1% reduction on the indy market and a 6.9% increase for small group enrollees.

the only other noteworthy item is that it looks like HealthPartners UnityPoint is dropping out of Iowa's small group market next year...but with 9 other carriers participating there's still plenty of options for that population.

Back in November, I noted that Georgia, one of the ten states STILL refusing to expand Medicaid coverage to hundreds of thousands of low-income residents a decade after they could have done so under the ACA, may finally be coming around...albeit via a rather silly & inefficient method. via the Atlanta Journal-Constitution:

Could Georgia adopt an Arkansas-style Medicaid plan?

Senior Republicans see an opening for a health care overhaul

Key Republicans say they’re open to legislation that would add hundreds of thousands of poor Georgians to the state’s Medicaid rolls — and bring in billions of federal dollars to subsidize it — as part of a compromise to roll back hospital regulations.

Here's the preliminary 2024 rate filings for Iowa's individual & small-group markets. Unfortunately, I only have the enrollment data for the two smaller carriers on the individual market (and for only one carrier on the small group market). Oddly, while the Iowa Insurance Dept. has detailed rate filings for Medica and Oscar, it doesn't have one for Wellmark posted...and on the small group market, they only have publicly-available filing documentation for two of the eleven carriers.

Interestingly, CareSource Iowa, which only joined the state's individual market this year, appears to be dropping out of it again in 2024...or at least they don't have a listing showing up at RateReview.HealthCare.Gov as of this writing. Similarly, Aetna seems to be dropping out of the small group market as well.

In any event, based on my estimate of Iowa's total ACA-compliant individual market, I can make an educated guess as to the former's weighted average, which should be roughly a 5.7% drop in premiums.

The Children’s Health Insurance Program (CHIP) is offered through the Healthy and Well Kids in Iowa program, also known as Hawki. Iowa offers Hawki health coverage for uninsured children of working families.

No family pays more than $40 a month. Some families pay nothing at all. A child who qualifies for Hawki health insurance will get their health coverage through a Managed Care Organization (MCO).

Here's the preliminary 2023 rate filings for Iowa's individual & small-group markets. Unfortunately, I only have the enrollment data for the two smaller carriers on the individual market (and none for the small group market), but based on my estimate of Iowa's total ACA-compliant individual market, I can make an educated guess as to the weighted average, which should be roughly 2.0%.

Unfortunately I can't do the same for the small group market; for that, the unweighted average rate increase is around 5.1%.

I should also note that Iowa also has 35,400 residents still enrolled in pre-ACA ("transitional" or "grandmothered") medical policies, with nearly all of them being via Wellmark:

Back in August, I analyzed the preliminary rate filings for the 2022 individual & small group markets in Iowa. At the time, I was unable to run a weighted average due to only having the enrollment data for one of the three individual market carriers (and none of the small group market).

At the time, the unweighted average rate change for the individual market came in at +0.7%, while small group plans averaged out at +0.9%. Unfortunately, this isn't terribly useful since it assumes every carrier has the same market share.

More recently, Iowar regulators have approved the rate filings (with almost no changes at all)...and the SERFF database now includes the Unified Rate Review Templates for every carriers, which allows me to fill in the enrollment of each in both markets. This lets me run the weighted average rate changes.

With that data, individual market plans are going up 6.6% for unsubsidized individual market enrollees and 1.2% for small group plans on average:

The only way I was able to find the rate changes was by using the federal Rate Review website, and even then, the actuarial memos are all heavily redacted, making it impossible to know what the enrollment for each carrier si (with one exception: Wellmark Health Plan reported having 32,000 ACA-compliant individual market enrollees as of March 2021).

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In some states I've been able to get more recent enrollment data from state websites and other sources.