Over the past few weeks, in the midst of the failed Republican-sponsored "ACA stabilization bill" known as Alexander-Collins (which laughably included "Bipartisan" in the title evne though it had changed dramatically from the actual bipartisan bills which Senators Patty Murray and Bill Nelson had worked with Lamar Alexander and Susan Collins on last fall), Democrats in both the House and Senate introduced real ACA stabilization/improvement bills of their own.

OK, it's taken me way too long to get around to doing this, but I'm finally going to do livestreaming via Periscope.

You can follow public streams via Twitter, of course (which I may do from time to time), but in order to receive notices of scheduled livestreams, you have to follow me on Periscope itself:

Louisiana officials will have to notify around 60,000 people who are elderly or disabled in early May that they are slated to lose their Medicaid benefits in July as a result of the Legislature's stalemate over the state budget and taxes.

Gov. John Bel Edwards has proposed eliminating some Medicaid programs that provide long-term care in order to cope with a $994 million budget deficit. The governor said he doesn't want to put forward such cuts, but he doesn't have much of a choice given the state's financial restrictions starting July 1, when the new budget year begins.

The Louisiana Department of Health is legally obligated to warn people about what might cuts be coming in July two months ahead of time, even if the programs are ultimately spared.

Here is our call to action for employers: Guide employees of any eligibility status to health coverage, whether employer-sponsored or government-supported, because it will benefit both employees and your company.

The main thrust of the article is that while most employers offer some sort of healthcare coverage option to their employees (in fact, most did so before the ACA mandated it), most of them don't appear to make a whole lot of effort to actually get the employees to enroll in that coverage...and even fewer make any sort of effort to encourage their staff to enroll in other types of healthcare coverage outside of the employer plan.

They include several charts and graphs, but this is the key one to me:

Gov. Gary Herbert signed a measure Tuesday to give more than 70,000 needy Utahns access to government health coverage, ending years of failed attempts on Capitol Hill to expand Medicaid in the state.

But whether House Bill 472 ever takes effect still remains uncertain. Under President Obama’s signature Affordable Care Act (ACA), the Utah law needs approval by the federal Centers for Medicare and Medicaid Services (CMS), which has sent mixed signals on whether it will fully sign off.

Even if CMS does approve HB472, it will likely be about a year — even on an aggressive schedule — before the state can begin enrolling people for coverage. Meanwhile, a competing Utah citizens initiative that would expand Medicaid coverage more widely than HB472 also continues to gather signatures for a spot on November’s ballot.

Well, sure enough, just yesterday the Iowa state Senate voted to allow unregulated junk plans to be sold to...pretty much anyone in the state:

The Iowa Senate voted Wednesday to let the Iowa Farm Bureau Federation and Wellmark Blue Cross & Blue Shield sell health insurance plans that don't comply with the federal Affordable Care Act.

The new coverage could offer relatively low premiums for young and healthy consumers, but people with pre-existing health problems could once again be charged more or denied coverage.

While many want Democrats in Congress to focus on improving the way the ACA is working rather than trying to pass a national health care plan, there is support for such a proposal. This month’s Kaiser Health Tracking Poll finds six in ten (59 percent) favor a national health plan, or Medicare-for-all, in which all Americans would get their insurance from a single government plan.

MILWAUKEE -- State insurance commissioners and officials coming out of a closed-door meeting with CMS said the administration announced it will not finalize the rule on longer duration short-term plans until the fall and will delay implementation of that rule until January 2019 -- though CMS disputed this characterization of the meeting when asked by Inside Health Policy . Several sources stressed that the delay of the rule means that issuers will be unable to factor in the potential impact...

I've obviously already written a bunch of stuff about this, including links to a few impact projection analyses, but this one was put together by Avalere Health on behalf of America's Health Insurance Plans (AHIP), which is one of the two major insurance carrier lobbying groups (the other one is BCBSA). On the surface you may expect a whitewash: "Oh, look at that, a report commissioned by Big Insurance is releasing a report claiming that these policies would be awesomesauce, big surprise!"

For some time now, I've been railing against Donald Trump's executive order pushing for the expansion of both "Short Term, Limited Duration" plans as well as "Association Plans". I've scornfully referred to his EO with the hashtag #ShortAssPlans.

Something which has gotten lost in the shuffle, however, is that I don't think short-term plans should necessarily be scrapped altogether, at least until we're able to achieve a comprehensive, universal coverage system in the future. Under our current patchwork heatlhcare system, I do think they serve a purpose for certain people in certain circumstances. I just think they need to be strongly regulated and limited in scope, partly to prevent siphoning off healthy people from the individual market risk pool...but partly to prevent people from being hit with financial catastrophe in the event of unexpected high medical expenses.

The problem is that Trump's executive order--which would effectively open the floodgates for them to be mutated into year-round plans, completely destroying one of the major points of the ACA in the first place.

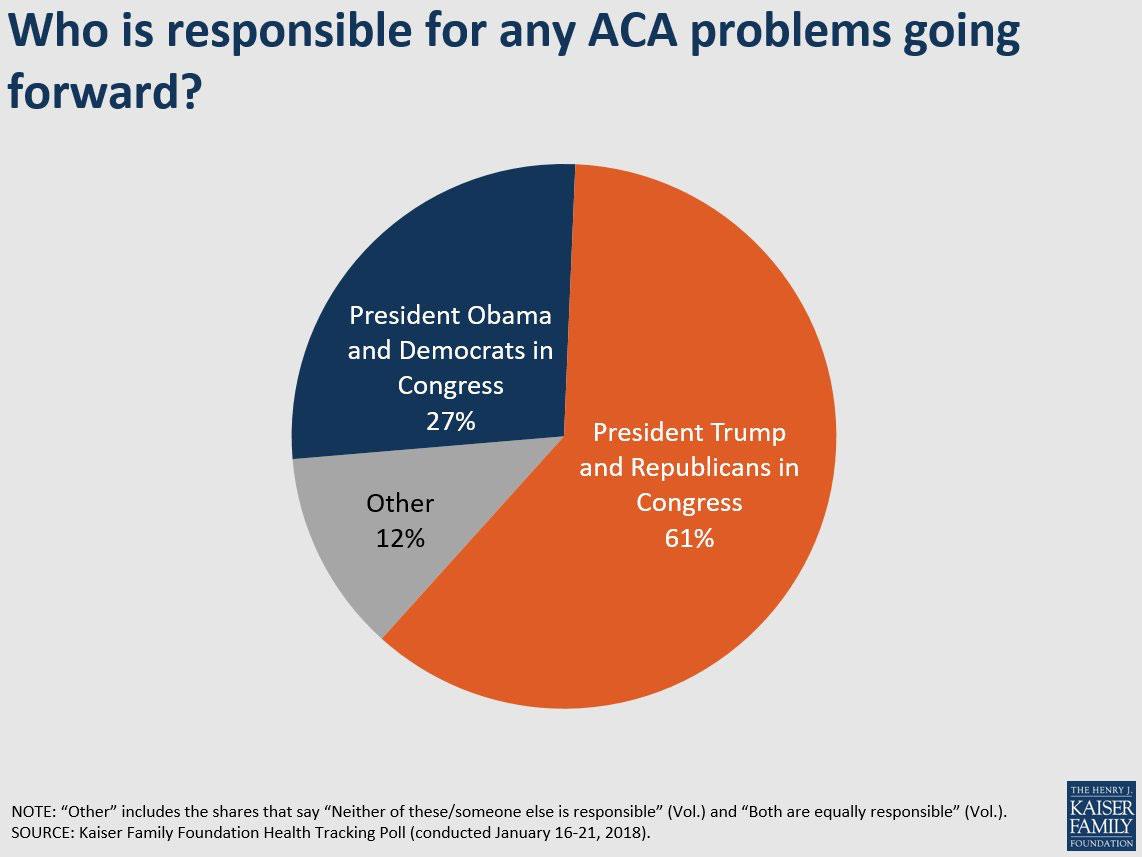

Yesterday morning, Larry Levitt of the Kaiser Family Foundation posted this tweet:

Our polling suggests the public is most likely to blame President Trump and Republicans in Congress for any problems in the insurance market going forward.

With all the discussion about subsidized enrollees, unsubsidized enrollees, short-term plans, association plans, health sharing ministries and so forth swirling around the ACA stabilization/CSR reimbursement payment/Silver Loading debate, I just wanted to take a quick moment to remind everyone that "The Uninsured" isn't a single amorphous blob; it consists of several fairly specific subsets.

The good news is that the Kaiser Family Foundation is among the most reliable sources for this sort of data in the business. The bad news is that their estimates are out of date--this analysis/breakout was last updated in October 2017, but the actual survey data is from 2016. Needless to say, a lot has changed in the intervening year and a half...namely, the Trump Administration and two full ACA Open Enrollment Periods.

TODAY IS THE 8TH ANNIVERSARY OF THE AFFORDABLE CARE ACT.

On March 23, 2010, President Barack Obama signed into law the Patient Protection & Affordable Care Act.

Since then, despite a number of real problems with the law and an endless series of ferocious attacks by the GOP, the ACA is still standing. It’s beaten and bloodied, but it’s still the law of the land, and it’s resulted in the uninsured rate being slashed from 48 million Americans in 2013 to 29 million today. 16 million people have been added to Medicaid coverage via ACA expansion, and 9 million are receiving subsidized healthcare coverage via the ACA exchanges.

Thanks to the ACA, no one can be denied coverage based on their medical condition. Women can’t be charged more for their gender. Maternity and mental health services now have to be covered. People undergoing chemotherapy and premature infants requiring neonatal care no longer eat up their lifetime coverage maximum cap within a few months.

OK, this is kind of beating a dead horse since the Alexander-Collins bill is dead anyway, but just for completeness sake:

Last week I pointed out that aside from everything else that's problematic about the abortion restriction language included in the A-C bill, it would also have run into a big legal problem because three states (California, New York and Oregon) legally mandate that major medical healthcare policys cover abortion, in direct opposition to the A-C provision which would deny federal subsidies, CSR assistance or reinsurance funds to...any healthcare policy which covers abortion.

OLYMPIA, Wash. (AP) — Gov. Jay Inslee has signed a measure that requires Washington insurers offering maternity care to also cover elective abortions and contraception.

The Washington Health Benefit Exchange today announced that 209,802 customers used Washington Healthplanfinder to purchase a Qualified Health Plan (QHP) for 2018 coverage during the most recent open enrollment period. This total is a nearly three percent increase over last year and is 50 percent higher than the number of enrollees recorded following the first open enrollment period in 2014.

A year ago I wrote up my own "wish list" of 22 recommendations for fixing, improving, strengthening and expanding the Affordable Care Act (it's officially 20 items but two of them really should have been split into two entries apiece). I called it "If I Ran the Zoo", and it received quite a bit of praise, even though I didn't come up with most of them myself; it was mostly a compilation of ideas which had been floating around progressive healthcare wonk circles for awhile.

In any event, now that the Republican "ACA stabilization bill" (Alexander-Collins) appears to be dead and buried, I figured it might be helpful to line up both the House and Senate versions of the ACA 2.0 bills to see how they compare to each other as well as to my own list of recommendations.

NOTE: I've modified the headline to clarify that it's CSR reimbursements which are dead, not the actual CSR subsidies. Those eligible for CSR assistance will still receive it from the insurance carriers..it's just that the carriers aren't/won't be reimbursed for doing so. In response, they've jacked up the premium rates on others to cover their losses.

As I understand it, this means that unless a standalone bill of some sort passes, there will be no significant legislative changes to the ACA exchange/individual market status for the 2019 Open Enrollment Period at the federal level...and that's extremely unlikely to happen this year.

The House ACA 2.0 bill would check off a half-dozen or so of the 20 items on my (now outdated) wish list of ACA fixes/improvements...but also includes another half-dozen provisions on top of that (many of the additional items would cancel out Trump/GOP sabotage efforts which hadn't even happened when I wrote my "If I Ran the Zoo" wish list a year ago).

A few days ago I warned Congressional Democrats that while I agree that appropriating CSR reimbursement payments at this point would be a net negative move thanks to the clever Silver Load/Silver Switcharoo workaround developed last year, there's one possible cloud surrounding that silver lining, so to speak: What if the Trump Administration were to attempt to put the kibosh on Silver Loading altogether?

I don't know the legality of such a move, mind you, but It has been thrown around the rumor mill of late, so I figured I should remind them to keep that possibility in mind.

New legislation will allow Vermont insurers to load cost of CSR only onto on-exchange silver plans for 2019

For 2018 coverage, Vermont, North Dakota and the District of Columbia were the only states that didn’t allow insurers to add the cost of cost-sharing reductions (CSR) to premiums after the Trump Administration cut off federal funding for CSR. In most states, insurers were allowed to either add the cost of CSR to all silver plan premiums, to all on-exchange silver plan premiums, or, in a few cases, to all metal-level plan premiums. But in Vermont, North Dakota and DC, insurers simply had to absorb the cost of CSR, estimated at $12 million a year in Vermont.

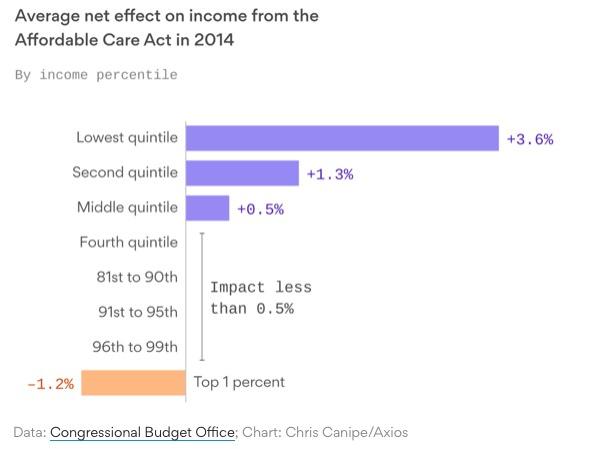

It's not about healthcare. It's not about "freedom". It's not about "tyrrany". It's not about "choice". It's about a tiny cadre of absurdly wealthy plutocrats being upset about a tiny fraction of their hoard being used to help out the least-fortunate among us. Via the Congressional Budget Office (graph via Axios):

Minnesota's 2018 Open Enrollment Period was a month longer than the official half-length period pushed by HealthCare.Gov, but was still over 2 weeks shorter than it had been in prior years, ending on January 14th, 2018. Even so, they reported a slight increase in year-over-year policy enrollees, ending OE5 with 116,358 QHP selections.

Typically, you'd see the official QHP selection number drop off noticeably by the end of the first quarter...usually by around 13% or so. Roughly 10% of those who select policies don't ever actually pay for their first monthly premium, and another 2-3% generally drop off after only paying for the first couple of months.

We released our End of Open Enrollment report this week, our most detailed look at the impact we are having across Colorado. This year, you will see that more of our customers are receiving help through the Advance Premium Tax Credit – 69 percent, compared to 61 percent last year – and the average level of monthly tax credit help climbed to $505 from $369 last year.

Not surprising...the 34% average rate increases (about 6 points of which is due specifically to CSR reimbursement payments being cut off...much lower than most states) meant that a lot more people qualified for tax credits in the first place, and of course the amount of credits went up accordingly...a bit more, actually (37% on average).

Consumer Choice Continues to be a Hallmark of the Marketplace

ALBANY, N.Y. (March 14, 2018) -- NY State of Health, the state’s official health plan Marketplace, today released data showing 2018 health plan enrollment by insurer. Statewide, 12 health insurers offer Qualified Health Plans (QHP) to individuals and 15 health insurers offer coverage to Essential Plan (EP) enrollees through the Marketplace. Ten health insurers participate in all individual market programs offered through NY State of Health allowing consumers a smooth transition if their program eligibility changes. Throughout the 2018 Open Enrollment Period, most consumers had a choice of at least four health insurer options in every county of the State.

The Bipartisan Health Care Stabilization Act of 2018 (BHCSA) would make several changes to health care laws. It would:

Change the state innovation waiver process established by the Affordable Care Act (ACA),

Appropriate a total of $30.5 billion for reinsurance programs or invisible high-risk pools in the nongroup insurance market,

Appropriate funds for the direct payment for cost-sharing reductions (CSRs) through 2021,

Allow any enrollee in the nongroup market to purchase a catastrophic plan, and

Require some existing funding for operations in the health insurance marketplaces to be used specifically for outreach and enrollment activities in 2019 and 2020.

As regular readers will recall, after three years of full 3 month Open Enrollment Periods across every state, last year the Trump Administration slashed the official Open Enrollment Period in half, down to just 6 weeks, from November 1 - January 31 down to November 1 - December 15th.

In response, most of the state-based exchanges announced that they were sticking with a longer period anyway, ranging anywhere from a 7th week all the way out to the full 3 month period, in the case of California, New York and the District of Columbia...each of which kept things going all the way through January 31st as had become the norm.

California even went one step further, passing a state law specifically mandating a 3-month Open Enrollment Period for 2018 and beyond.

Until today, I've been operating on the assumption that they'd be sticking with the November/December/January schedule which had become the default.

What’s next: Alexander and Collins are hoping to get this proposal included in the omnibus spending bill Congress needs to pass this week. We should find out soon whether it's in or out.

I just did a light analysis of how many people would be helped or hurt by CSR funding in 2019 in Rhode Island, and concluded that at least 28% of exchange enrollees would see their premiums increase if CSR funding was restored, while only perhaps 2-3% would see their premiums drop.

So there you have the enrollment results of full-bore on-exchange silver-loading of CSR costs in one state. In all, 49,993 on-exchange enrollees with incomes up to 400% FPL chose plans other than silver. About 48,000 of them were subsidized. That's 31.2% of all enrollees, within striking distance of Aron-Dine's upper bound of 36% for all marketplace enrollees.

HealthSource RI, Rhode Island's ACA exchange, released preliminary 2018 Open Enrollment data awhile ago, but this morning they released their final, official demographic data breakout, and there's a lot going on here:

HealthSource RI sees 5% enrollment increase and nation leading lowest benchmark plan cost

State-based marketplace sees rise in enrollment of “young invincibles”

Under the Guise of “Health Insurance Stabilization,” Congress Should Not Axe Financial Help for Low-Wage Families

In negotiations over stabilizing the individual health insurance market, lawmakers are considering slashing federal health care assistance for low- and moderate-income consumers by more than $27 billion a year. In dollars terms, this would be a greater blow than completely eliminating, in one stroke, the Low-Income Home Energy Assistance Program, the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC), the Child Care and Development Block Grant, the Community Development Block Grant, and federal grant programs for community-based mental health services and substance abuse prevention and treatment.

Health insurers and the Trump administration face a court decision shortly that will determine whether the government must pay insurers billions of dollars despite Republican efforts to block payments they view as an industry bailout.

Insurers have filed roughly two-dozen lawsuits claiming the federal government reneged on promises it made to pay them under the Affordable Care Act.

...It could also shape the outcome of other insurer lawsuits that would leave the government potentially owing as much as roughly $20 billion in past and future payments. Those cases, legal experts say, amount to the largest civil lawsuits ever.

Between the lines: This doesn't solve the partisan dispute over abortion language, as it'd bar plans that offer abortion coverage from receiving federal subsidies. But it hints that there's Republican support behind a set of policy changes that could substantially lower premiums ahead of the 2018 elections.

I wrote an extensive piece about the way abortion coverage is currently handled for ACA exchange policies back in October 2017:

Yesterday I came out against the pending ACA stability package because one of the 5 proposed provisions should be a flat-out dealbreaker for Democrats (the abortion ban), while another one is would hurt more people than it helps (CSR funding).

Today, I need to explain the problem with CSR funding in a bit more detail but to also note a new twist which makes it even more complicated...as well as taking note of a sixth provision being thrown into the mix by the GOP which, again, should be a dealbreaker for Democrats.

First up: CSR funding.

I'm on the record as being strongly in favor of a bill recently proposed by House Democrats Frank Pallone, Jr., Richard Neal and Bobby Scott which would repair, strengthen and expand the ACA in a half-dozen ways while also preventing or reversing another half-dozen types of sabotage of the ACA by the Trump Administration. Here's the full list of what would be included in what I've shorthanded "ACA 2.0":

As long as I'm snarking on Washington's exchange for getting so excited over what appear to be pretty minor tweaks (to the average Joe, anyway), I might as well also give a shout-out to Connect for Health Colorado as well, which just posted this tidbit:

To Our Valued Stakeholders,

We took an important step forward this week with our board’s decision to move ahead on building a new eligibility system. With our own system, we will be able to provide customers a better application and enrollment experience and at the same gain more control and predictability for IT expenses.

A simplified path for enrolling with financial help can be expected to help us grow enrollment while getting more Coloradans the Advance Premium Tax Credit and Cost Share Reduction benefits that they are eligible to receive. We will continue to support Health First Colorado (Medicaid) enrollments and ensure that customers are routed to the right program, whether they begin at our site or with the PEAK application.

Sens. Lamar Alexander and Susan Collins have proposed a market stabilization package that would include funding for the Affordable Care Act's cost-sharing reduction subsidies for three years, three years of federal reinsurance at $10 billion a year, additional ACA waiver flexibility for states, and expanded eligibility for "copper" plans.

Alexander presented the plan yesterday to America's Health Insurance Plan's board of directors, adding that if Democratic leadership supports the bill, “it’ll be law by the end of next week." Alexander has long said the package should be included on the omnibus spending bill.

Exit Poll of PA-18 Shows Lamb Won Big On Health Care

Date: March 14, 2018

Public Policy Polling conducted a telephone exit poll election survey of voters who cast ballots in Pennsylvania’s 18th Congressional District special election yesterday. Voters who voted in the contest were asked about the role of health care in their decision.

The exit poll shows that health care was a top priority issue to voters in this district and that voters believed Democrat Conor Lamb’s views were more in step with theirs.

In 2016, voters in this district backed Donald Trump by 20 points, but last night they backed a Democrat for Congress in a referendum on the health care plans of the Republican Congress:

Wisconsin Senator Tammy Baldwin has been on a bit of an "Improve the ACA" tear lately. A couple of weeks ago she introduced the "Fair Care Act" to try and nip Donald Trump's #ShortAssPlans proposal in the bud. Now she's introduced another bill which would help shore up the ACA exchanges themselves: The "Advancing Youth Enrollment Act" via Kimberly Leonard of the Washington Examiner):

The Advancing Youth Enrollment Act would give higher federal subsidies to people between the ages of 18-34 so that the cost of private Obamacare plans for them would be lower.

...Under the proposal, young adults would see the maximum percentage of income they must pay toward health insurance under Obamacare decrease by 2.5 percentage points for people between the ages of 18 to 30. Each year after, until the age of 34, they would see a gradual phaseout of 0.5 percentage points a year.

Today, Pam MacEwan, CEO of the Washington Health Benefit Exchange, issued the following statement on the signing of House Bill 2516:

“The Washington Health Benefit Exchange applauds today’s signing of House Bill 2516 by Gov. Jay Inslee.

“This state-level legislation protects important progress made in Washington state under the Affordable Care Act. Our position as the state’s health insurance gateway is now stronger than ever, and despite continued uncertainty we may see at the federal level, this bill enables us to continue improving the customer experience for the people in our state.

Last fall, Dem Senator Patty Murray and GOP Senator Lamar Alexander (among the few Republican Senators actually interested in improving the ACA) got together and hammered out a deal called Alexander-Murray. At the time, the bill would have done the following:

Two years of subsidy funding, along with funding for the rest of 2017. There will also likely be additional steps to help enrollees with their premiums in 2018.

A "copper plan" for people older than 30, which would be less comprehensive than other ACA plans but would have a lower premium.

$106 million in enrollment outreach funding in 2018 and 2019.

Shorter review time for states seeking waivers from some of the ACA's coverage requirements. It's unclear what other waiver changes have been agreed to at this time.

Authorization for funding to help states launch reinsurance programs, which would defray the costs of covering the sickest consumers.

Of these five items, it's really the first two which would have the biggest impact: CSR reimbursement payments and a low-end "Copper Plan".

I should note up front that despite the snarky headline, this is actually good news on the whole, and Premera does deserve some credit for it since part of the $250 million they refer to below is voluntary on their part.

Premera Blue Cross, the sole carrier offering ACA exchange individual market policies throughout the entire state of Alaska, and one of the major carriers on the indy market in Washington State, posted this press release today:

Premera Announces $250 Million Investment In Customers and Community

Mountlake Terrace, Wash. — (March 12, 2018) — Premera Blue Cross, a leading health plan in the Pacific Northwest, today announced $250 million in investments over five years across Washington and Alaska to help stabilize the individual market, improve access to care in rural areas and support local communities in their efforts to address the behavioral health issues impacting their residents.

Former CMS representative and current healthcare policy advisor for Sen. Brian Schatz, Aisling McDonough, made an important point last night:

If you have a pre-existing condition and live in a rural area, especially in VA, TN, OH, IN, MO, IA, or NV, then I'm worried there might not be a plan available for you next year.

People should be worried about bare ACA counties in 2019 b/c of GOP sabotage.

Between mandate repeal, short-term plans, health ministries, farm bureaus, etc, the guaranteed $ for the lone ACA insurer is getting smaller. It's not the same calculus as it was in 2017 & 2018.

UPDATE 4/11/18: I posted this piece about a month ago; I don't have any specifics, but I have reason to believe that the Michigan state legislature could be moving on this any day now. If you live in Michigan, CALL YOUR STATE SENATOR OR REPRESNTATIVE AND TELL THEM *NOT* TO IMPOSE WORK REQUIREMENTS ON "HEALTHY MICHIGAN" ENROLLEES!

State Senate introduces bill to add work requirements to Medicaid

The bill would require able-bodied adults to work or be in school for 30 hours a week in order to receive Medicaid.

Some lawmakers in Lansing want people to work to get Medicaid. The Senate introduced a bill Thursday. It would add work requirements to the Medical Assistance Program, or Medicaid.

...If passed, able-bodied adults would be required to work or continue school for 30 hours per week as a condition of receiving medical assistance.

Alabama, which has refused to expand Medicaid for low-income adults under the Affordable Care Act (ACA), is now proposing to make work a condition of Medicaid eligibility for very low-income parents, stating that it wants to encourage work. Its proposal, however, actually would penalize work: because Alabama hasn’t expanded its program, those who comply with the new requirements by working more hours or finding a job will raise their income above the state’s stringent Medicaid income limits, thereby losing their Medicaid coverage and likely becoming uninsured.

Five weeks ago, when Idaho Governor "Butch" Otter announced that Idaho had decided to basically just blow off federal law altogether and start offering non-ACA compliant health insurance policies on the individual market alongside the compliant versions, I wrote:

To be honest, I'm not entirely sure I understand why Idaho would do this. Yes, of course the deep red state government opposes the ACA in general and sure, they want to "lower premiums" on the individual market, but Trump's recent "ShortAss Plan" executive order would do pretty much the same thing(allowing non-ACA compliant off-exchange "Short Term/Association Plans" which amount to the same thing...without putting GOP Gov. Butch Otter's fingerprints all over the ugly stories which would soon follow if/when people started actually enrolling in these types of policies. Besides, as much as Idaho claims to hate the ACA, they seem to be quite proud (and rightly so) of their own state-based ACA exchange, Your Health Idaho.

Well, it sounds like CMS Administrator Seema Verma was thinking along the same lines, because this unexpected story broke a few hours ago: Verma sent a letter to Otter and his state Insurance Commissioner shooting down their "state-based plans" idea as being flat-out illegal.

Top Republican looks to codify move to short-term healthcare plans

Sen. John Barrasso, R-Wyo., introduced legislation Wednesday that would let more people enroll in short-term health insurance plans, an idea that builds off a Trump administration proposal issued last month.

The Improving Choices in Health Care Coverage Act would allow people to stay on less expensive, short-term medical plans for as long as 364 days and allow them to renew for subsequent years.

Yes, that's right: "Improving Choices in Health Care Coverage Act", or ICHCCA. I'm going with #IckyJunkPlan instead, it rolls off the tongue better.

In other words, this would codify Donald Trump's executive order into federal law. It might even trump (no pun intended) state laws against #ShortAssPlans, although perhaps not.

Today, Covered California issued a new study about the projected impact of Donald Trump and Congressional Republican efforts to undermine and sabotage the Affordable Care Act not just in 2019, but over the next 3 years. They main focus is on two sabotage moves which have already happened (repeal of the individual mandate and the shortened/underfunded marketing of the open enrollment period on the federal exchange) and one which is on the verge of happening (Trump's "Short Term and Association Plan" executive order, aka #ShortAssPlans).

*(except people who are actually sick, that is) --h/t Anne Paulson

I've written a lot about Idaho's decision to simply ignore ACA regulations by allowing non-ACA compliant healthcare policies which would destabilize the individual healthcare market even worse than it already is today.

But it would be a mistake to ignore what Idaho is up to. If the Trump administration doesn’t intervene, other red states will surely follow in its footsteps. The result will be widespread disregard of the law and the rise of state-to-state inequalities in the private market similar to those that already exist in Medicaid.

Every day I'm overwhelmed with so many important healthcare policy stories that I don't have time to do a full write-up on them all. Usually I just skip past most, but once in awhile I like to do quick posts on a bunch at a time.

Most people try to avoid reading their health insurance policies — that’s what employers and insurance agents are for. Anyone who plans to buy short-term health insurance, though, will need to read the policy carefully.

The Trump administration recently announced plans to allow consumers to buy short-term health insurance plans that last for up to a year. They are currently capped at 90 days.

Thanks to Twitter follower "@tweetmix" for bringing this to my attention.

Back in late January, I noted that while the ACA's Shared Responsibility Penalty (aka the Individual Mandate) was repealed by Congressional Republicans back in December, ithe repeal doesn't actually go into effect until spring 2020 (for lacking coverage in 2019). For 2017 and 2018, it's still on the books...and the IRS has stated point-blank that they will be rejecting tax returns that don't include a statement of ACA-compliant coverage. This, I noted, is going to piss off a whole bunch of confused people who are under the assumption tthat the mandate penalty has already been repealed. My suspicions were confirmed by last week's Kaiser Family Foundation survey, which found that sure enough, at least 21% of the country incorrectly thinks that they don't have to pay a fine for not having compliant coverage this year.

House Republicans are demanding a series of controversial abortion and health care policies in the annual health spending bill, setting up a showdown with Democrats and threatening passage of an omnibus spending package to keep the government open.

Democrats are vowing to block the slew of long-sought conservative priorities. The riders would cut off federal funding to Planned Parenthood, eliminate a federal family planning program and ax the Teen Pregnancy Prevention Program, according to sources on Capitol Hill. Republicans also want to insert a new prohibition on funding research that uses human fetal tissue obtained after an abortion.

Nearly three years ago, there was a big report about a bunch of Republican Governors of states which hadn't expanded Medicaid under the Affordable Care Act who claimed that they were willing to do so, but only if a work requirement was part of the deal:

In nearly a dozen Republican-dominated states, either the governor or conservative legislators are seeking to add work requirements to Obamacare Medicaid expansion, much like an earlier generation pushed for welfare to work.

The move presents a politically acceptable way for conservative states to accept the billions of federal dollars available under Obamacare, bringing health care coverage to millions of low-income people. But to the Obama administration, a work requirement is a non-starter, an unacceptable ideological shift in the 50-year-old Medicaid program and a break with the Affordable Care Act’s mission of expanding health care coverage to all Americans. The Health and Human Services Department has rejected all requests by states to tie Medicaid to work.

The White House is seeking a package of conservative policy concessions — some of which are certain to antagonize Democrats — in return for backing a legislative package bolstering Obamacare markets, according to a document obtained by POLITICO.

The document indicates the administration will support congressional efforts to prop up the wobbly marketplaces, in exchange for significantly expanding short-term health plans and loosening other insurance regulations.

Kreidler announces intention to being rulemaking on short-term medical plans

March 6, 2018

OLYMPIA, Wash. – Insurance Commissioner Mike Kreidler announced his intention today to begin rule-making to create protections for Washington consumers who buy short-term medical plans. He is taking this action in response to the recent rules the Trump administration proposed to increase the duration of short-term medical plans from 90 days to up to 364 days.

In a statement last week, Kreidler shared his concerns about short-term medical plans:

RUMFORD, RI (March 6, 2018) – HealthSource RI for Employers today announced it has hit a major milestone. The health insurance marketplace for small employers has now enrolled its 700th small business. These 700 local businesses reflect over 5,200 Rhode Islanders.

With the 2018 Open Enrollment Period coming up just 5 days from now, it's time to put this to bed: After 6 months of painstaking research and analysis, I've compiled a comprehensive analysis of the weighted average rate changes for unsubsidized ACA-compliant individual market policies in 2018, including both the on- and off-exchange markets. It's already been confirmed by a different analysis by healthcare consulting firm Avalere Health, which used a completely different methodology to arrive at the exact same conclusion: The national average increase isbetween 29-30%, ranging from as low as a 22% average premium drop in Alaska(thanks to their successful reinsurance program) to as high as a painful 58% increase in Virginia.

U.S. SENATOR TAMMY BALDWIN AIMS TO BLOCK PRESIDENT TRUMP’S PLAN TO ALLOW INSURERS TO SELL JUNK PLANS WITH LEGISLATION TO GUARANTEE PROTECTIONS FOR PRE-EXISTING CONDITIONS

“The Fair Care Act is an opportunity for lawmakers to keep their word on guaranteed protections for pre-existing conditions.”

WASHINGTON, D.C. – Following the Trump Administration’s recent proposed rule allowing insurance companies to once again sell ‘junk’ health care plans, U.S. Senator Tammy Baldwin today announced new legislation to block the rule and guarantee protections for people with pre-existing conditions.

UPDATE: Late last night I was able to dig up the actual legislative text of the bill introduced by the House Democrats yesterday; after reading over the details, I've decided that it's a strong enough package overall that, in software terms, it would be considered a full version upgrade (2.0) as opposed to "only" a service pack/point upgrade (1.5). I've therefore changed the headline to reflect this.

I've also updated some sections fo the analysis below to include the details from the text itself.

“But the plans were on display…”

“On display? I eventually had to go down to the cellar to find them.”

“That’s the display department.”

“With a flashlight.”

“Ah, well, the lights had probably gone.”

“So had the stairs.”

“But look, you found the notice, didn’t you?”

“Yes,” said Arthur, “yes I did. It was on display in the bottom of a locked filing cabinet stuck in a disused lavatory with a sign on the door saying ‘Beware of the Leopard.”

--Douglas Adams, The Hitchhiker's Guide to the Galaxy

Over a year and a half ago, I noticed that aside from the usual names being listed as insurance carriers offering individual market policies in various states (Humana, Molina, Blue Cross Blue Shield, etc), there was one other name which kept popping up over and over again: "Freedom Life":

Over the past few weeks,I've posted partial 2018 Open Enrollment Period demographic data from Connecticut, Idaho, Maryland, New York and Washington State. Still missing are final wrap-up reports from the other 7 state-based exchanges...as well as The Big One: The official report from the Assistant Secretary for Planning and Evaluation (ASPE).

The 2014 ASPE report was released on May 1st, 2014...just 17 days after the first, tumultuous 2014 Open Enrollment Period ended (only 12 days, really, since the report actually ran through April 19th, 2014 even though the "overtime" period technically ended on April 15th).

Sen. Orrin Hatch (R-UT) on Thursday called supporters of the Affordable Care Actsome “of the stupidest, dumbass people I’ve ever met” during a speech before the American Enterprise Institute.

“We […] finally did away with the individual mandate tax that was established under that wonderful bill called ‘Obamacare,’” Hatch said, according to Fox News 13. “Now, if you didn’t catch on, I was being very sarcastic.”

“[The Affordable Care Act] was the stupidest, dumbass bill that I’ve ever seen. Now, some of you may have loved it. If you do, you are one of the stupidest, dumbass people I’ve ever met. This was one—and there are a lot of ’em up on Capitol Hill from [that] time,” Hatch added.

Matt Whitlock, a spokesman for Hatch, defended the senators comments, telling Fox News 13, “The comments were obviously made in jest, but what’s not a joke is the harm Obamacare has caused for countless Utahns.”

To gauge the perspectives of Americans on the marketplaces, Medicaid, and other health insurance issues, the Commonwealth Fund Affordable Care Act Tracking Survey interviewed a random, nationally representative sample of 2,410 adults ages 19 to 64 between November 2 and December 27, 2017, including 541 people who have marketplace or Medicaid coverage. The findings are compared to prior ACA tracking surveys, the most recent of which was fielded between March and June 2017. The survey research firm SSRS conducted the survey, which has an overall margin of error is +/– 2.7 percentage points at the 95 percent confidence level.

SACRAMENTO, Calif. — Covered California Executive Director Peter V. Lee issued the following statement in connection with the Harvard Medical School Study, “Eliminating the Individual Mandate Penalty in California: Harmful but Non-Fatal Changes in Enrollment and Premiums,”published in Health Affairs. The Harvard study, conducted by a team lead by Dr. John Hsu, is the first national effort to measure the potential impacts of removing the individual mandate penalty based on surveying actual California consumers about their likely actions in the face of there being no penalty.

Millions of people who failed to make sure they were enrolled in ACA-compliant healthcare coverage are going to file their tax returns this spring thinking that they don't have to pay a penalty for not doing so only to discover that the penalty is still in effect.

Then, next spring (assuming the IRS sticks to its guns on the issue and there's no further legislative changes made), anyone who didn't #GetCovered for 2018 are also going to have to pay the penalty (which, again, is either $695 per adult/$348 per child or 2.5% of their household Modified Adjusted Gross Income).

The damage caused by the mandate being repealed to the individual market risk pool (and rate premiums) will be felt this November, when people start shopping around for 2019 coverage...but the actual "benefit" (i.e., those who don't get covered not having to pay the mandate penalty) won't show up until spring 2020.

The Kaiser Family Foundation runs a highly respected monthly national tracking poll on healthcare issues. Their latest was just released, and while there's a bunch of interesting stuff included, there are two main takeaways. Here's the first:

The February Kaiser Health Tracking Poll finds a slight increase in the share of the public who say they have a favorable view of the Affordable Care Act (ACA), from 50 percent in January 2018 to 54 percent this month. This is the highest level of favorability of the ACA measured in more than 80 Kaiser Health Tracking Polls since 2010. This change is largely driven by independents, with more than half (55 percent) now saying they have a favorable opinion of the law compared to 48 percent last month. Large majorities (83 percent) of Democrats continue to view the law favorably (including six in ten who now say they hold a “very favorable” view, up from 48 percent last month) while nearly eight in ten Republicans (78 percent) view the law unfavorably (unchanged from last month).