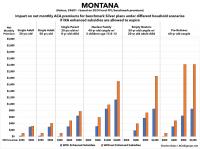

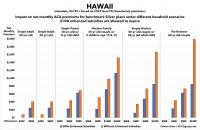

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

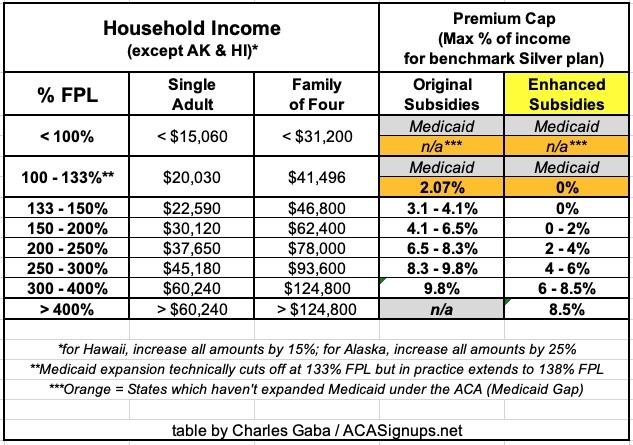

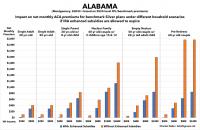

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

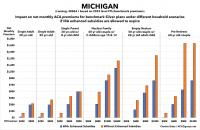

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

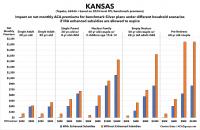

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

It's been another several months since the last time I wrote about the seemingly never-ending Braidwood v. Becerra lawsuit which threatens to not only end many of the ACA's zero-cost preventative services, but which could also throw all sorts of regulatory authority into turmoil depending on what precedents it sets.

On March 30, 2023, a federal district court judge issued a sweeping ruling, enjoining the government from enforcing Affordable Care Act (ACA) requirements that health plans cover and waive cost-sharing for high-value preventive services. This decision, which wipes out the guarantee of benefits that Americans have taken for granted for 13 years, now takes immediate effect.

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

Covered California announced today that more than 158,000 Californians remained covered through the Medi-Cal to Covered California enrollment program over the past year.

Beginning in April 2023, following the end of the federal continuous coverage requirement put in place during the COVID-19 pandemic, Medi-Cal resumed its renewal process by redetermining eligibility for over 15 million of its members. In May 2023, Covered California and the Department of Health Care Services (DHCS), which administers California’s Medi-Cal program, launched the Medi-Cal to Covered California enrollment program.

Under the program, Covered California automatically enrolls individuals in one of its low-cost health plans when they lose Medi-Cal coverage and gain eligibility for financial help through Covered California. Through early June of 2024, the program has helped 158,100 Californians remain insured.

The Michigan Dept. of Financial Services hasn't issued any press release yet, but nearly all 2025 preliminary rate filings for the MI individual and small group markets are available via the SERFF database.

The most noteworthy item in Michigan's individual market is that there's a new entry: HAP CareSource. I'm assuming this is some sort of joint insurer effort by CareSource and Health Alliance Plan (which has only offered off-exchange ACA plans for several years now) but am not certain about that.

In terms of actual rate hikes, most of them are in the mid single digits, but Priority Health, which holds exactly 1/3 of the market share (equal to Blue Cross when you combine their PPO & HMO divisions), is seeking an eye-opening 18.9% average rate increase.

With Priority Health included in the mix, rate increases being requested by Michigan indy market carriers average 10.5% for 2025.

Every month for years now, the Centers for Medicare & Medicare Services (CMS) has published a monthly press release with a breakout of total Medicare, Medicaid & CHIP enrollment; the most recent one was posted in late February, and ran through November 2022.

Normally, states will review (or "redetermine") whether people enrolled in Medicaid or the CHIP program are still eligible to be covered by it on a monthly (or in some cases, quarterly, I believe) basis.

However, the federal Families First Coronavirus Response Act (FFCRA), passed by Congress at the start of the COVID-19 pandemic in March 2020, included a provision requiring state Medicaid programs to keep people enrolled through the end of the Public Health Emergency (PHE). In return, states received higher federal funding to the tune of billions of dollars.

As a result, there are tens of millions of Medicaid/CHIP enrollees who didn't have their eligibility status redetermined for as long as three years.

In February 2024, 83,387,167 individuals were enrolled in Medicaid and CHIP, a decrease of 654,280 individuals (0.8%) from January 2024.

76,289,951 individuals were enrolled in Medicaid in February 2024, a decrease of 640,417 individuals (0.8%) from January 2024.

7,097,216 individuals were enrolled in CHIP in February 2024, a decrease of 13,863 individuals (0.2%) from January 2024

As of February 2024, enrollment in Medicaid and CHIP has decreased by 10,480,839 individuals (11.2%) since March 2023, the final month of the Medicaid continuous enrollment condition under the Families First Coronavirus Response Act (FFCRA) and amended by the Consolidated Appropriations Act, 2023.

Medicaid enrollment has decreased by 10,440,608 individuals (12.0%).

CHIP enrollment has decreased by 40,231 individuals (0.6%).

Between February 2020 and March 2023, enrollment in Medicaid and CHIP increased by 22,992,937 individuals (32.4%) to 93,868,006.

Medicaid enrollment increased by 22,650,766 individuals (35.3%).

CHIP enrollment increased by 342,171 individuals (5.0%).

A former Democratic Senate majority leader and former HHS secretary are calling on the Biden administration to correct a longstanding loophole in the Affordable Care Act (ACA) they say is preventing the law from permitting as much cost-free access to vaccines for patients as is intended, joining a bipartisan group of lawmakers and a coalition of health groups that have asked top HHS officials to make the change in recent months.

OK, I'm back from the Doctors for America conference! I'll be posting a write-up about that soon, but in the meantime I have a backlog of healthcare policy developments to catch up on...

Oregon becomes 3rd in nation to seek federal approval for a basic health program

A group of volunteer advisors to the Oregon Health Authority has voted Tuesday to make the state the third in the nation to seek federal approval for a basic health program.

...The Oregon Health Policy Board voted unanimously to approve Oregon’s blueprint application. It was the last step in a lengthy policy-making process needed for state approval of the plan after a task force last year recommended moving forward with it.

Doctors for America mobilizes doctors and medical students to be leaders in putting patients over politics on the pressing issues of the day to improve the health of our patients, communities, and nation.