As I just noted, the end of the official COVID-19 Public Health Emergency, whenever it happens (it's currently scheduled to end as of April 16th but could be extended once again at any point before then) will cause a new problem:

Millions of Americans currently enrolled in Medicaid will likely no longer be legally eligible to remain on the public healthcare program, threatening to cause a massive overload of agencies and potentially leaving many of them stranded without any healthcare coverage at all.

Legislation to help about 300,000 Oregonians on Medicaid to maintain their coverage after the Covid-19 public health emergency ends advanced out of committee on Monday.

(sigh) It's a bit silly for me to write about this now, given that the 2022 Open Enrollment Period ended a few weeks ago, but it's still relevant going forward.

As long-time readers know, I was one of a handful of healthcare wonks who coined the phrase "Silver Loading" to describe a wonky policy pricing strategy which insurance carriers started using back in late 2017 to counteract the Trump Administration's decision to terminate Cost Sharing Reduction subsidy reimbursement payments:

Let's say in 2017 a carrier projected that overall claim expenses in 2018 would increase around 5%. To keep things simple, let's say they offered just 3 plans: One Bronze, one Silver (which happends to also be the "benchmark Silver" used to determine subsidies) and one Gold, priced at an average of $450, $600 and $750/month.

Every year, I spend months tracking every insurance carrier rate filing for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need. The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier:

How many effectuated enrollees they have enrolled in ACA-compliant individual market policies;

What their average projected premium rate change is for those enrollees (assuming 100% of them renew their existing policies, of course); and

Ideally, a breakout of the reasons behind those rate changes, since there's usually more than one.

Usually I begin this process in late April or early May, but this year I've been swamped with other spring/summer projects: My state-by-state Medicaid Enrollment project and my state/county-level COVID-19 vaccination rate project.

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In most states I've been able to get more recent enrollment data from state websites and other sources.

For Oregon, I'm relying on raw data from the Oregon Health Authority for January 2021 and later.

Total Medicaid enrollment in Oregon (including ACA expansion peaked at a little over 1.1 million back in 2015, but dropped off to around 950,000 for a couple of years before COVID hit the country. Since then, non-ACA enrollment has gone up about 14%, ACA expansion has increased by over 30% and overall enrollment is 22% higher than it was in February 2020.

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

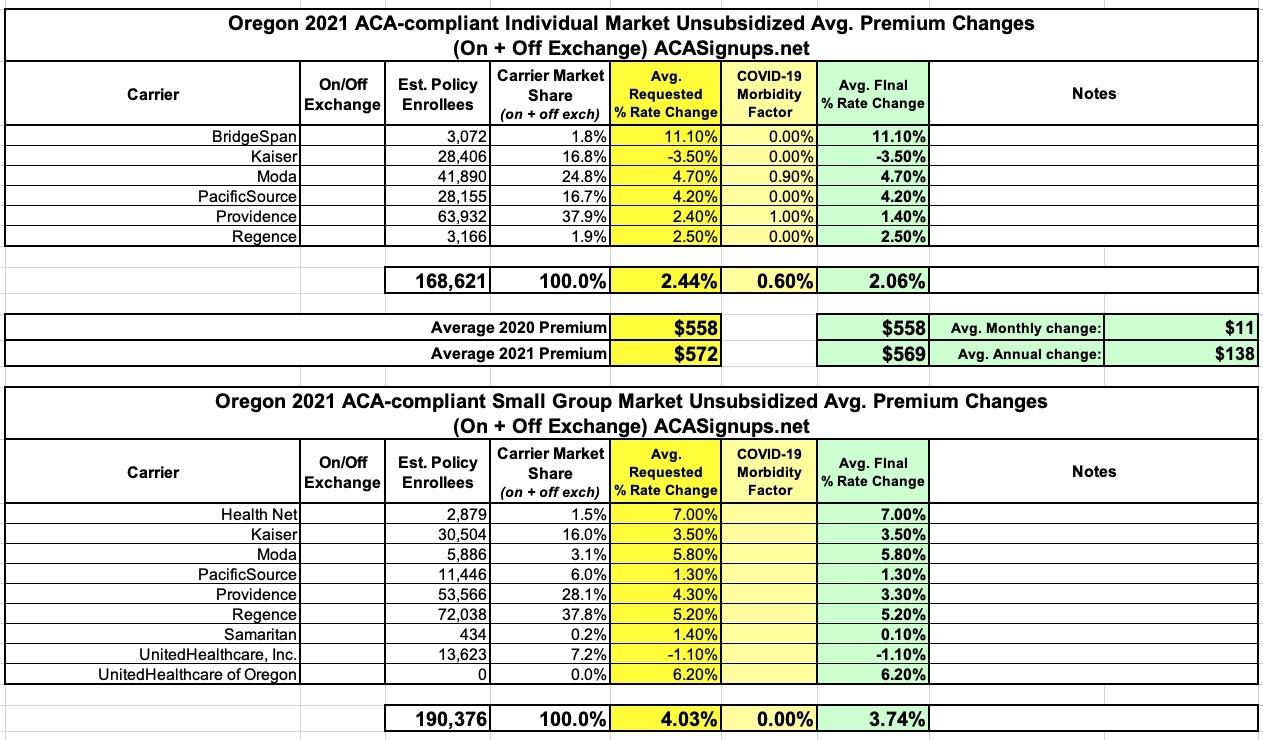

Way back in May (a lifetime ago!), the Oregon Insurance Dept. was one of the first states to release their preliminary 2021 ACA premium rate filings for the individual and small group markets.

At the time, the carriers were asking for a weighted average 2.4% increase on the indy market (OR DOI put it at 2.2%) and a 4% increase for small group policies.

They issued some slightly revised rates later on in the summer, and sometime in August I believe they issued the final approved rates...which are just slightly lower on a few carriers.

In the end, 2021 Oregon enrollees are looking at weighted average premium hikes of 2.1% for indy plans and 3.7% for small group policies:

In the middle of a deadly global pandemic which has already killed more than 100,000 Americans and completely disrupted the entire U.S. healthcare system, private insurance carriers still have to go about preparing their annual premium rate change filings for 2021. This is a long, complicated process which begins a good nine months before the new plans and prices are actually enrolled in.

The task of setting 2020 premiums was the first time since the ACA went into effect which was relatively calm for insurance carrier actuaries:

Governor Whitmer Announces Statewide Closure of All K-12 School Buildings; School building closures will last Monday, March 16 through Sunday, April 5

Today, Governor Gretchen Whitmer announced that in order to slow the spread of Novel Coronavirus (COVID-19) in Michigan, she is ordering the closure of all K-12 school buildings, public, private, and boarding, to students starting Monday, March 16 until Sunday, April 5. School buildings are scheduled to reopen on Monday, April 6.

As of tonight, the number of presumptive positive cases of COVID-19 in Michigan is 12.

I noted yesterday that Virginia is the latest state to consider jumping onboard the State-Based Exchange train, joining Nevada, New Mexico, New Jersey, Pennsylvania, Maine and possibly Oregon in making the move. Every time I've mentioned Oregon, however, I've had to put a bit of an asterisk on it because I wasn't quite sure whether or not their shift back to their own full tech platform was still a go or not.

Like Nevada, Oregon did have their own full exchange once upon a time. Back in the first ACA Open Enrollment Period from 2013-2014, both states were among those which ran their own exchange websites. Nevada's was developed by Xerox; Oregon's was developed by Oracle.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

{kind=link}