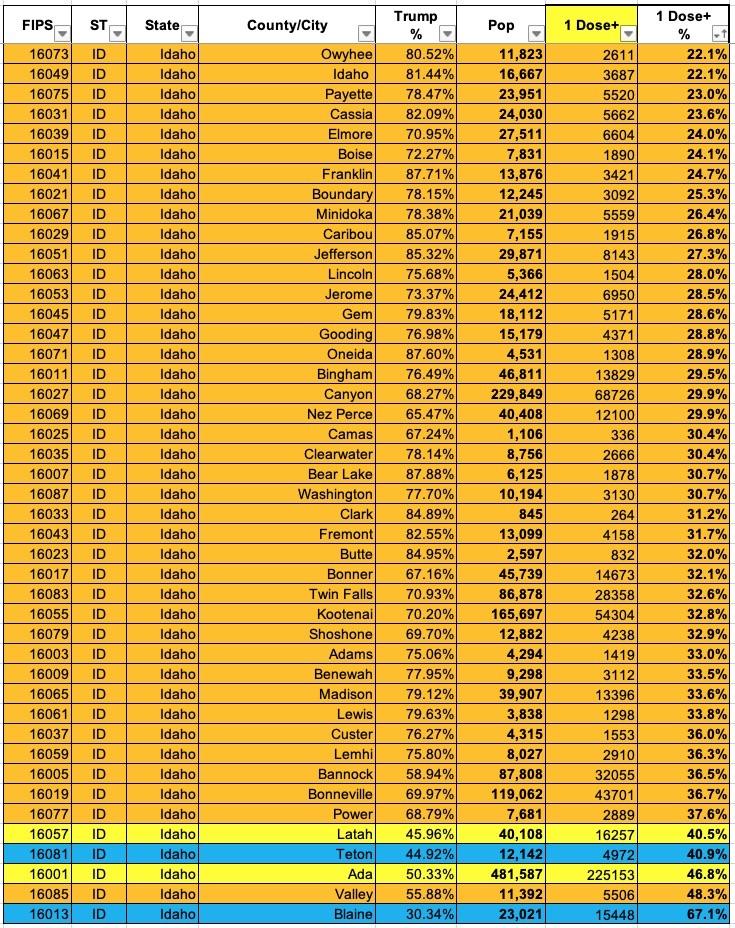

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

NOTE: This is an updated version of a post from a couple of months ago. Since then, there's been a MASSIVELY important development: The passage of the American Rescue Plan, which includes a dramatic upgrade in ACA subsidies for not only the millions of people already receiving them, but for millions more who didn't previously qualify for financial assistance.

Much has been written by myself and others (especially the Kaiser Family Foundation) about the fact that millions of uninsured Americans are eligible for ZERO PREMIUM Bronze ACA healthcare policies.

I say "Zero Premium" instead of "Free" because there's still deductibles and co-pays involved, although all ACA plans also include a long list of free preventative services from physicals and blood screenings to mammograms and immunizations with no deductible or co-pay involved.

Much has been written by myself and others (especially the Kaiser Family Foundation) about the fact that millions of uninsured Americans are eligible for ZERO PREMIUM Bronze ACA healthcare policies.

I say "Zero Premium" instead of "Free" because there's still deductibles and co-pays involved, although all ACA plans also include a long list of free preventative services from physicals and blood screenings to mammograms and immunizations with no deductible or co-pay involved.

If you have a fairly healthy year, you really could go the entire year without paying a dime in healthcare costs while still taking advantage of many of these free services, and also having the peace of mind that in a worst-case scenario, at least you wouldn't go bankrupt. Not perfect, but a lot better than going bare especially since you wouldn't pay a dime in premiums.

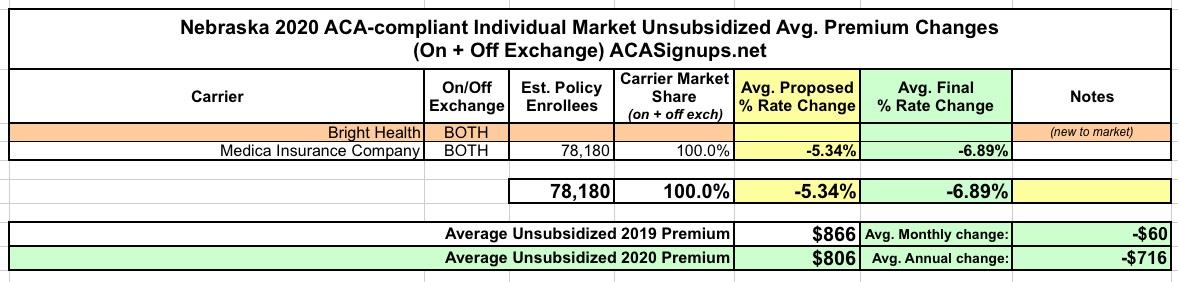

I'm not sure what's going on with Bright Health Care in Nebraska. They entered the state's ACA market in 2020, but for whatever reason they aren't showing up in the HealthCare.Gov Rate Review database. The only carrier listed for the state's individual market is Medica, and the SERFF database for Nebraska doesn't bring up either one.

Even more curious, when I ran a search to make sure that Bright hadn't simply jumped in and then out again the following year, I found this article:

Bright Health Plan announced today its 2021 expansion plan. It will expand access to its Medicare Advantage, individual and family-plan products in select areas, and to add fully-insured small business plans to its available products in certain markets.

When I first ran the preliminary 2020 avg. rate hike numbers for Nebraska in August, the sole carrier offering ACA-compliant policies in the state (Medica) was planning on reducing their average premiums by 5.3%. Yesterday the final, approved rates were posted by CMS, and unsubsidized 2020 premiums will be even lower, by 6.9% on average.

For 2020, Bright Health is joining the Nebraska exchange.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

The floodgates are now officially open for preliminary (not final) 2020 ACA rate filings for both the Individual and Small Group markets. There are several states which only have a single insurance carrier offering policies on the Individual Market, which makes it very easy to calculate the weighted average rate changes...seeing how a single carrier holds 100% of the market.

Among these states are Alaska, Nebraska and Wyoming, where the sole Indy Market carriers are once again Premera BCBS (AK), Medica (NE) and BCBS of Wyoming. Unfortunately, the rate filing forms for all three are partly redacted, making it impossible for me to determine how many total enrollees they have, although I have a pretty good estimate of the on-exchange number as of the end of March for each.

In Alaska, Premera's 2020 rates are virtually unchanged year over year. In Nebraska, Medica expects to reduce rates an average of 5.3%. And in Wyoming, BCBS is only looking to bump up average unsubsidized premiums by 1.6%.

I realize this may seem a bit late in the game seeing how the 2019 ACA Open Enrollment Period has already started, but I do like to be as complete and thorough as possible, and there were still 9 states missing final/approved premium rate change analyses as of yesterday which I wanted to check off my 2019 Rate Hike Project list.

Fortunately, RateReview.HealthCare.Gov has finally updated their database to include the approved rate changes for every state, which made it easy to take care of most of these.

Nebraska has a slightly confusing siutation, which is surprising since Medica is the only carrier offering ACA policies in the state, When I first took a look at the requested premium changes for 2019 back in August, it looked like the average was around 1.0%...that was based on splitting the difference between the 3.69% and -2.60% listings, since the filing form was redacted and I didn't know what the relative market split was between Medica's product lines.

I just realized that while I've written quite a bit about the potential loss of Medicaid coverage for thousands of residents of Michigan, Kentucky and Arkansas over the past few months due to the new work requirement laws in those states, It's been far too long since I've given a shout-out to the four states which are hoping to add Medicaid expansion (or at least continue it, in one case) exactly one week from today.

For years, elected leaders in conservative states have resisted expanding Medicaid, the government health program for low-income Americans. Now voters in four of those states will decide the question directly.

A Lancaster County District judge has dismissed a challenge to the Medicaid expansion petition initiative, allowing the initiative to be placed on the November ballot.

The lawsuit was brought by former state Sen. Mark Christensen and Sen. Lydia Brasch. They alleged the initiative was an unconstitutional delegation of legislative authority, contained more than one subject, which the state Constitution prohibits, and that it failed to identify Nebraska Appleseed as a sworn sponsor.

Last week, Secretary of State John Gale confirmed that enough signatures were gathered by petition circulators to put the question of whether to expand Medicaid to about 90,000 uninsured adult Nebraskans on the Nov. 6 ballot.

...The campaign has said Medicaid expansion will create and sustain 10,000 new jobs, reduce medical bankruptcies, bring $1.1 billion of Nebraskans’ tax dollars back from Washington, D.C., and produce savings by reducing uncompensated care for those who lack health coverage.

{kind=link}