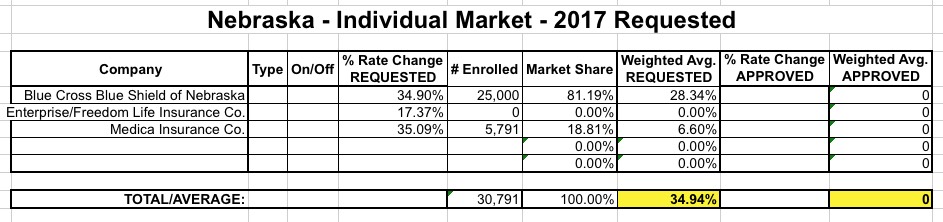

Nebraska is about as simple as it gets--there's only one carrier offering ACA individual market plans. Unfortunately, they've redacted the combined average rate change request between their two plan entries, so all I can do is split the difference and assume around a 1% average increase.

The Urban Institute projected that Nebraska rates would see a whopping 20.4 percentage point increase due to #MandateRepeal and #ShortAssPlans, which are both referenced in Medica's filing. Since they don't get more specific than that, I'm assuming 2/3 of Urban's estimate, or a 13.6% increase.

Unsubsidized Nebraska enrollees are currently paying an average of $854/month, so if accurate, that's a difference of around $116/month or nearly $1,400 for the year. Ouch.

A couple of weeks ago, a joint letter was sent to all four Congressional leaders from AHIP (America's Health Insurance Plans), the BlueCross BlueShield Association, the American Academy of Family Physicians, the AMA, the American Hospital Association and the Federation of American Hospitalsm warning them, in no uncertain terms, of what the consequences of repealing the individual mandate would be:

We join together to urge Congress to maintain the individual mandate. There will be serious consequences if Congress simply repeals the mandate while leaving the insurance reforms in place: millions more will be uninsured or face higher premiums, challenging their ability to access the care they need. Let’s work together on solutions that deliver the access, care, and coverage that the American people deserve.

I noted back in August that there will only be one insurance carrier offering policies on the Nebraska individual market next year (Medica), with Blue Cross Blue Shield dropping out.

Medica has 35,269 members on their ACA-compliant individual market plans in 2017. But all of the current Aetna enrollees, as well as off-exchange BCBSNE enrollees, will need to switch to Medica plans at the end of 2017, as Medica will be the only insurer offering plans in Nebraska’s individual market for 2018.

With Blue Cross Blue Shield of Nebraska declining to participate in the Nebraska exchange, that leaves just Medica as the sole individual market carrier. They're asking for a 16.9% average rate hike,

Interestingly, while Medica's rate filing letter clearly states that the 16.9% request assumes CSR payments will be made and the mandate will be enforced, they also list "unprecedented uncertainty/risk inherent in the marketplace" as one of the key drivers of the increase.

Between updating the "Who could lose coverage" graphics, prepping for my town hall thing last night and updating the 2018 Rate Hike project, I've gotten way behind on my "Who's saying 'screw rate hikes, I'm just gonna bail completely next year' updates. Let's take care of that now, OK? The first three updates are courtesy of Louise Norris writing for healthinsurance.org; the fourth is vai Kimberly Leonard for the Washington Examiner:

Insurers in Idaho had to submit forms for 2018 plans by May 15, but they have until June 2 to file rates. Mountain Health CO-OP, SelectHealth, PacificSource and Blue Cross of Idaho all filed forms to continue to offer Your Health Idaho plans in 2018.

As I noted when I crunched the numbers for Texas, it's actually easier to figure out how many people would lose coverage if the ACA is repealed in non-expansion states because you can't rip away healthcare coverage from someone who you never provided it to in the first place.

A few days ago I noted that up to 50,000 South Dakota residents who previously held out at least had some hope that the state might expand Medicaid under the ACA next year have already had that hope yanked out from under them like a rug:

A proposal to expand a federal health insurance program for needy people could be off the table following the results of Tuesday's election.

The victory of Republican Donald Trump, who has called for a repeal of Obamacare, along with the increasingly conservative Republican make-up of the South Dakota state Legislature could thwart Gov. Dennis Daugaard's efforts to expand Medicaid in the state.

Today (Friday, Sept. 23) happens to be the deadline for insurance carriers to sign agreements with the federal government for participating in the exchange this Open Enrollment period (I'm not sure if today's deadline also applies to the state-based exchanges or not; they might be different). Until today, it looked as though there were going to be 3 carriers offering individual policies on the Nebraska exchange:

The figures compared 2016 and 2017 rates for Blue Cross Blue Shield of Nebraska, Aetna Health Inc. and Medica, the three companies that will offer policies to Nebraskans on the exchange when open enrollment starts Nov. 1.

However, as commenter M E noted, it looks like BCBSNE decided to wait until literally the last minute (last hour, anyway) to change their minds:

Huh. Back in June, when I first ran the requested rate hike numbers for Nebraska, it looked as though there were only two real carriers offering individual plans, either on or off the exchange: Blue Cross Blue Shield and Medica. UnitedHealthcare announced they were leaving NE along with a bunch of other states, and Coventry (aka Aetna) didn't have any filings for 2017, so I assumed they were bailing as well. Finally, the less time spent talking about "Enterprise/Freedom Life" the better. So...it looked like BCBS and Medica were it. Here's what the table looked like: