Virginia is slated to become the nation’s 19th state-based exchange now that CMS has given officials the greenlight to fully transition away from healthcare.gov starting Nov. 1 for the 2024 plan year. Meanwhile, the State Corporation Commission (SCC), which administers the exchange, has suspended the state’s reinsurance program that had lowered premiums by about 20% for 2023, so individual plan rates are set to increase by an average 28.4%, according to a presentation made during an Aug. 9 hearing on the 2024 rates.

Virginia’s Health Benefit Exchange (VHBE) was enacted in 2020 by former Gov. Ralph Northam (D) and has been operating as a state-based exchange reliant on the federal platform (SBE-FP) since plan year 2021. The state paused the transition activity in 2021 after the enhanced premium tax credits were enacted but restarted it the following year.

CMS Approves Added Benefits to Essential Health Benefits (EHB) Benchmark Plans in North Dakota and Virginia

September 6: CMS approved added benefits to the Essential Health Benefits (EHB) benchmark plans for North Dakota and Virginia for the 2025 plan year. The Affordable Care Act requires non-grandfathered health plans in the individual and small group markets to cover essential health benefits (EHB), which include items and services in ten benefit categories. For plan year 2020 and after, the Final 2019 HHS Notice of Benefits and Payment Parameters provides states with greater flexibility by establishing new standards for states to update their EHB-benchmark plans, and for tailoring them to fit the health care needs of their states.

Here's the best summaries I could find of the additional benefits for each state:

A few weeks ago, I noted that Virginia's average 2023 unsubsidized ACA individual market premiums dropped by nearly 13% thanks to the newly-implemented state-based reinsurance program...but that they were at risk of skyrocketing by as much as 25% in 2024 due to that same reinsurance program being at risk of not continuing for a second year because of a budget standoff:

During 2021, the Virginia General Assembly passed HB 2332, the Commonwealth Health Reinsurance Program, which was signed into law on March 31, 2021 as Chapter 480, of the 2021 Virginia Acts of Assembly. This bill requires the State Corporation Commission to submit a waiver request for federal approval to establish a reinsurance program beginning January 1, 2023.

Last month the Centers for Medicaid & Medicaid Services (CMS) director of the Center for Consumer Information & Insurance Oversight (CCIIO...yeah, those names & acronyms just roll off the tongue, don't they?) informed the state of Georgia that they're gonna have to wait one more year before launching their own fully state-based ACA exchange (SBE) platform.

There were several reasons given for the 1-year delay, but many of them stemmed from the fact that Georgia was attempting to skip the "Federally-Facilitated" SBE phase which every other state which has made the transition to their own full state-based platform has undergone for at least one year.

The main reason for this was the implementation of a so-called "reinsurance" program which was originally passed by the (then Democratically-controlled) state legislature:

The most significant thing to impact Virginia carriers 2023 filings was the state's Section 1332 Reinsurance Waiver. I wrote about this way back in 2018 when the state was originally considering applying for one, but it didn't actually go into effect until January 2023:

Back in 2019, long before the American Rescue Plan passed, I embarked on an ambitious project. I wanted to see what the real-world effects would be of passing a piece of legislation which would eliminate the Affordable Care Act's so-called "Subsidy Cliff" while also strengthening the subsidy formula for those who qualified. Call it "ACA 2.0" for short, if you will (that's what I do, anyway).

This legislation has been around in near-identical form under one official title or another for years, usually bundled within a larger healthcare package. In 2018 it was called the "Undo Sabotage & Expand Affordability of Health Insurance Act of 2018" (or "USEAHIA" which is about as awkward a title as I can imagine.

MICHIGAN: Another One (Mostly) Bites The Dust; 12th CO-OP Drops Off Exchange, May Go Belly-Up

It appears that East Lansing-based Consumers Mutual Insurance of Michigan could wind down operations this year as it is not participating in the state health insurance exchange for 2016.

But officials of Consumers Mutual today are discussing several options that could determine its future status with the state Department of Insurance and Financial Services, said David Eich, marketing and public relations officer with Consumers Mutual.

Consumers Mutual CEO Dennis Litos said: "We are reviewing our situation (financial condition) with DIFS and should conclude on a future direction this week.”

While Eich said he could not disclose the options, he said one is “winding down” the company, which has 28,000 members, including about 6,000 on the exchange.

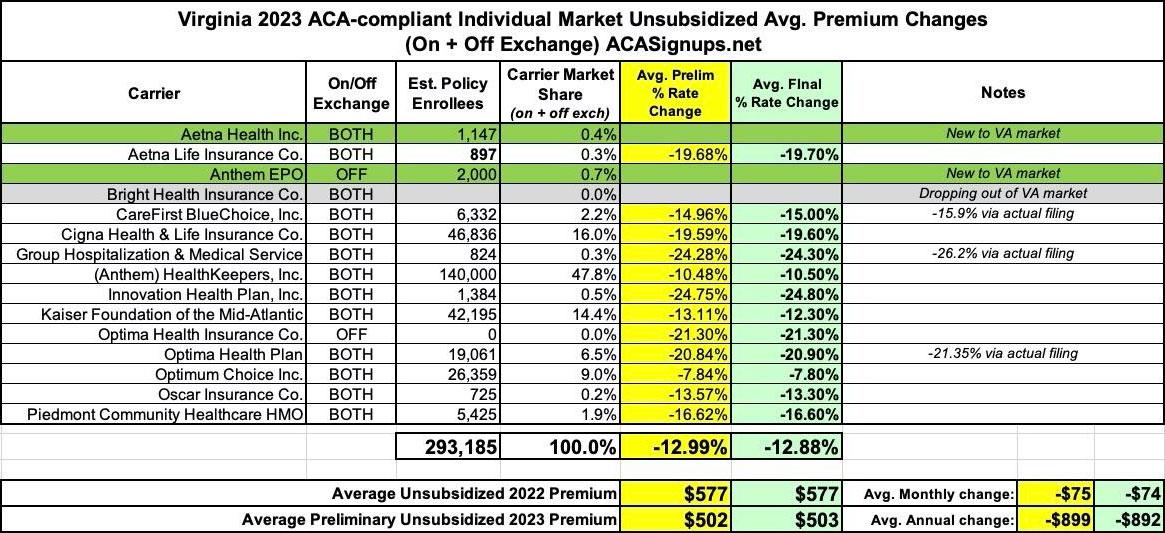

Virginia has an extremely robust, competitive individual & small group insurance market...and in 2023 it's getting even more competitive, with what appear to be two new carriers joining the individual market (Aetna Health Inc. and Anthem EPO), although Anthem is only offering off-exchange policies (why??) while Bright Health Insurance appears to be dropping out of the individual market (which is a common theme for Bright this year...)

Virginia used to be one of the first states to release their preliminary rate filings for the upcoming year, but for the past year or two it's been among the later ones. I don't know how much of this is due to COVID-related issues or if it's just an internal policy change for some other reason. Regardless, as a result, VA also happens to be the first state to release their annual rate filings since the Inflation Reduction Act (which includes a 3-year extension of the enhanced ACA subsidies) passed both the U.S. House and Senate.