NOTE: This is an updated version of a post from a couple of months ago. Since then, there's been a MASSIVELY important development: The passage of the American Rescue Plan, which includes a dramatic upgrade in ACA subsidies for not only the millions of people already receiving them, but for millions more who didn't previously qualify for financial assistance.

Much has been written by myself and others (especially the Kaiser Family Foundation) about the fact that millions of uninsured Americans are eligible for ZERO PREMIUM Bronze ACA healthcare policies.

I say "Zero Premium" instead of "Free" because there's still deductibles and co-pays involved, although all ACA plans also include a long list of free preventative services from physicals and blood screenings to mammograms and immunizations with no deductible or co-pay involved.

Much has been written by myself and others (especially the Kaiser Family Foundation) about the fact that millions of uninsured Americans are eligible for ZERO PREMIUM Bronze ACA healthcare policies.

I say "Zero Premium" instead of "Free" because there's still deductibles and co-pays involved, although all ACA plans also include a long list of free preventative services from physicals and blood screenings to mammograms and immunizations with no deductible or co-pay involved.

If you have a fairly healthy year, you really could go the entire year without paying a dime in healthcare costs while still taking advantage of many of these free services, and also having the peace of mind that in a worst-case scenario, at least you wouldn't go bankrupt. Not perfect, but a lot better than going bare especially since you wouldn't pay a dime in premiums.

I've written several times about how Republican Senator Cory Gardner of Colorado has repeatedly shown sickening levels of chutzpah and gaslighting when it comes to the Affordable Care Act:

In a pathetic attempt to gaslight Colorado voters, Gardner is now trying to paint himself as supporting healthcare expansion, going so far as to try to claim credit for passage and approval of last year's Section 1332 Reinsurance Waiver program which dramatically reduced premiums for unsubsidized individual market enrollees throughout Colorado...even though a) he didn't have a damned thing to do with it and b) the reinsurance program was only able to be developed thanks to the Affordable Care Act...which Gardner has repeatedly voted to repeal.

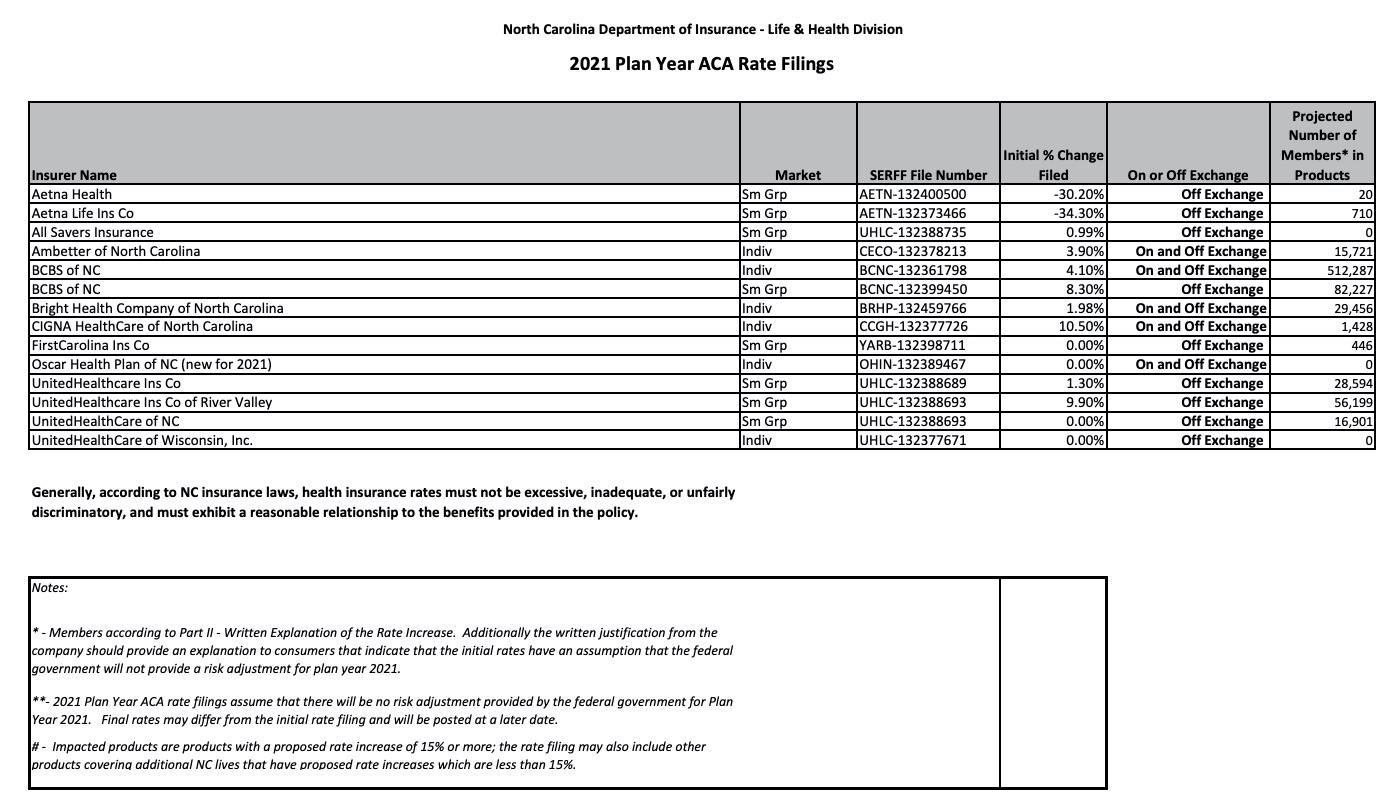

The good news is they include the number of people enrolled by each carrier in both markets, making it easy to calculate a weighted average, and th ey even include the SERFF tracking number for each.

The bad news is they don't include links to the actuarial memos, and even plugging the tracking numbers into the SERFF database only brings up the memos for three of the six carriers on the individual market...and of those, two of the three have been redacted (Oscar and Cigna), while the third (UnitedHealthcare) is brand-new to the North Carolina market anyway and therefore has no COVID-19 impact on their rate changes to speak of.

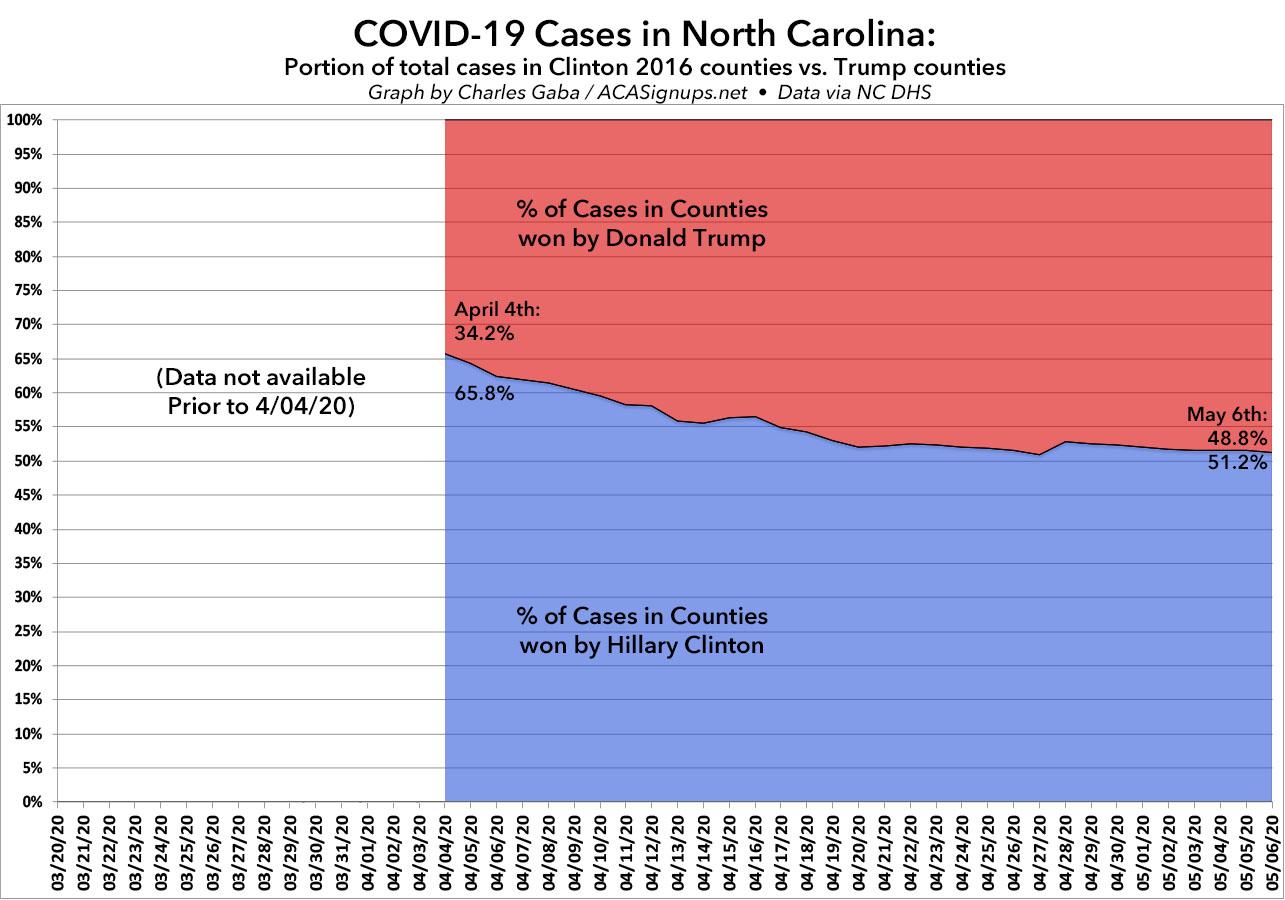

As you can tell, I've become a bit obsessed with tracking the COVID-19 outbreak on the county level within each state, along with the corresponding partisan divide.

Today, I'm looking at North Carolina. The good news is that I was able to acquire daily case & death data going back over a month. The bad news is that it stops a month ago...that is, the earliest day I could find county-level data for was April 4th, which means I'm missing about two weeks worth of numbers from the second half of March (most states I've looked at so far start around March 20th).

Still, even with the first two weeks missing, the trendline is pretty clear: Once again, what started out as a "Democratic area problem" has quickly shifted into an Everyone problem. It looks like things have stabilized at roughly a 50/50 divide, with around the same number of cases appearing in counties which voted for Donald Trump in 2016 as HIllary Clinton:

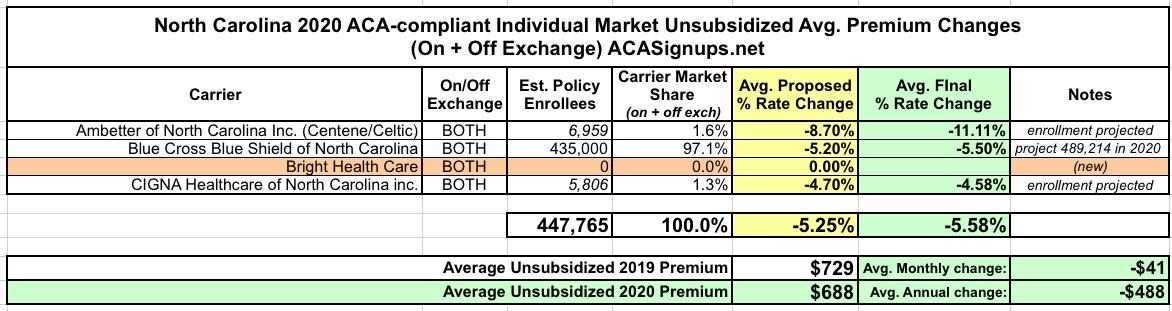

North Carolina has three individual market carriers in 2019. For 2020, that's increasing to four, as Bright Health Care is expanding into the NC market. The other three carriers (Blue Cross Blue Shield has a near monopoly at the moment) had requested average unsubsidized rate drops of 5.3% previously; in the end the final rates are dropping slightly more, to -5.6%.

Cigna extended its individual healthcare exchange products for the 2020 plan year, the insurer said Sept. 18.

For 2020, individuals can purchase individual health plans in 19 markets across 10 states. The expansions will take place in counties in Kansas, South Florida, Utah, Tennessee and Virginia. The other states include Arizona, Colorado, Illinois and North Carolina.

The plans will be available for purchase on the individual marketplace during the 2020 open enrollment period, which begins Nov. 1. Plans will take effect Jan. 1.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

NOTE: This post re. North Carolina's 2020 individual market premium rate change is incomplete because it only includes one of the three carriers participating in NC's market (Blue Cross Blue Shield of NC). The rate change requests for Cigna and Centene haven't been released yet.

Normally I'd wait until I had data for the other two as well, but BCBSNC held around 95% of the state's Individual Market share last year, with Cigna holding the other 5% (Centene was a new entry to the market, so they didn't have any of it). I don't know how much the relative share has changed this year, but I'm assuming that BCBSNC still holds the lion's share of the total.

Blue Cross NC is decreasing 2020 Affordable Care Act (ACA) rates by an average of 5.2 percent for plans offered to individuals and an average of 3.3 percent for plans offered to small businesses with one to 50 employees. With this reduction, we take 238 million steps towards more affordable care in North Carolina.

{kind=link}