As I noted last night, thanks to the federal Rate Review website finally being updated to include the final, approved 2022 rates for both the individual and small group markets in all 50 states (+DC), I've been able to fill in the missing data for my annual ACA Rate Change Project.

As I note there, the overall weighted average looks like it'll be roughly +3.5% nationally.

Normally I write up a separate entry for both the preliminary and approved rate changes in each individual state, but it seems like overkill to create 14 separate entries at once. Besides, in many of these states there's been few if any changes between the preliminary and approved rate changes.

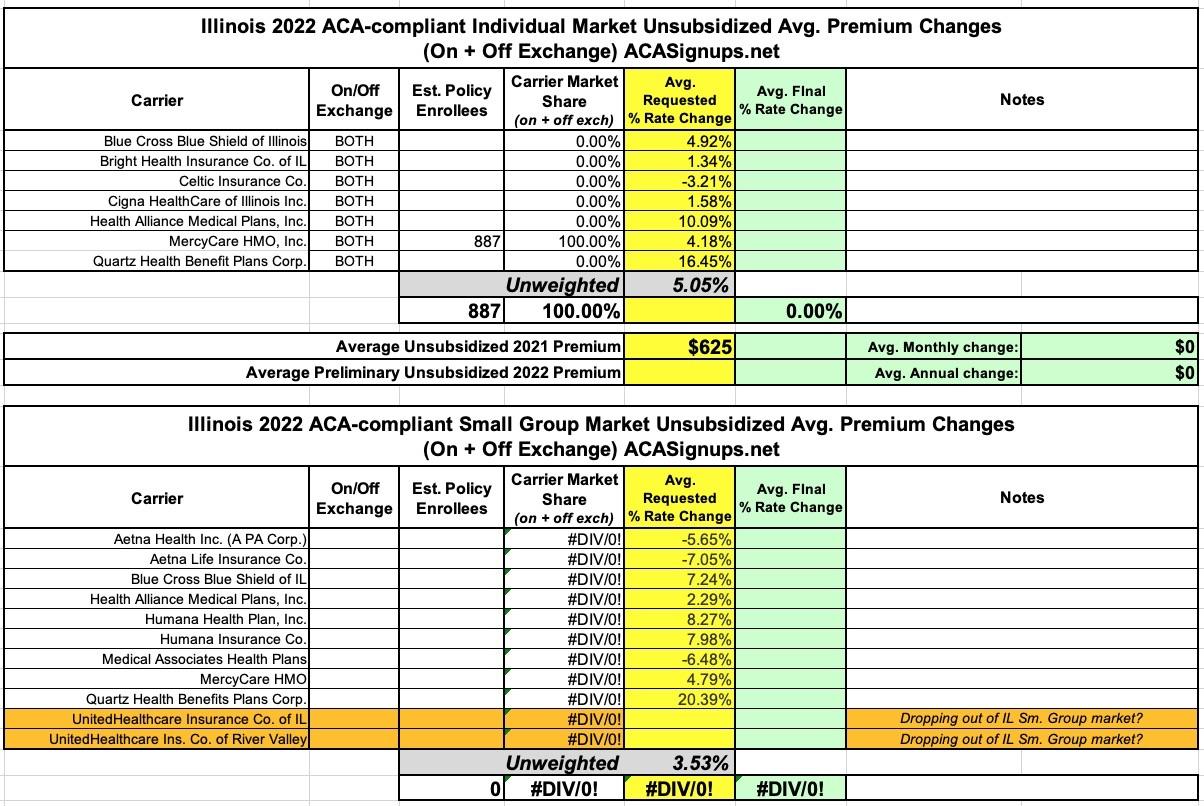

Unfortuantely, Illinois is another state which doesn't make it easy to analyze annual health insurance premium rate filings. There's no details on their insurance department website, their SERFF listings don't seem to include the actuarial memos or URRT forms, and even the federal Rate Review listings only include the average requested rate changes; the actuarial memos there are mostly heavily redacted.

The unweighted average rate changes requested for 2022 come in at +5.1% for the individual market and +3.5% for small group plans. It's worth noting that neither of the UnitedHealthcare listings from 2021 (on the small group market) show up in the federal database, which either means they're pulling out of the Illinois market entirely or they just haven't been added to the listings yet. Given that it's mid-October, the former seems more likely.

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In some states I've been able to get more recent enrollment data from state websites and other sources.

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

(sigh) Once again, I only have actual enrollment data for a one of the five carriers offering individual market policies in Illinois next year, and for two of the eleven selling small group plans. That means I can't run a weighted average rate change for either market, just unweighted ones.

That being said, the unweighted average change on the individual market is a 1.8% premium reduction, while the small group market is increasing by 5.2%.

Louisiana's 2020 Presidential primary was scheduled for April 4th, but the other day Democratic Governor John Bel Edwards and Republican Secretary of State Kyle Ardoin agreed to reschedule it for June 20th...which is actually later than the last previously-scheduled primary in the U.S. Virgin Islands on June 6th:

The presidential primary elections in Louisiana slated for April will be delayed by two months, the latest in a series of dramatic steps government leaders have taken to slow the spread of the new coronavirus.

Secretary of State Kyle Ardoin, Republican, and Gov. John Bel Edwards, a Democrat, both said Friday they would use a provision of state law that allows them to move any election in an emergency situation to delay the primary.

The presidential primary elections, initially scheduled for April 4th, will now be held June 20th. Ardoin said in a press conference he does not know of any other states that have moved elections because of the new coronavirus, or COVID-19.

TO CLARIFY: In pretty much all cases below, when it comes to restaurants, "shut down" refers to dining in only; they're pretty much all still allowing delivery/carryout orders.

Last March I wrote an analysis of H.R.1868, the House Democrats bill that comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or make improvements in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

Back in March I wrote an analysis of H.R.1868, the House Democrats bill which comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

When I ran the preliminary 2020 average unsubsidized premium rate change requests for Illinois in early August, I was frustrated because I had no idea what the actual enrollment numbers for the individual carriers were, making it impossible to run a weighted average change. I had to go with an unweighted average increase of 1.4% statewide.

Fortunately, since then, not only have the final rate changes been approved and posted, I've also acquired the enrollment data, allowing for a weighted average. In the end, average unsubsidized premiums are dropping ever so slightly (0.3%)...versus going up ever so slightly (0.1%) statewide.

{kind=link}