According to a release from the company on Tuesday, the firm will no longer offer individual market plans through the Affordable Care Act in Dallas, Texas, and New Jersey.

..."We hope to return to these markets as we carry on with our mission to change healthcare in the US."

The "we hope to return" part suggests that Oscar will continue to be available off the exchange in New Jersey, since completely pulling out of a state means a carrier has to wait at least 5 years before re-entering. So...there's that, anyway.

...Oscar currently covers 7,000 people in Dallas and 26,000 in New Jersey.

As noted a couple of weeks ago, all three of the major insurance carriers participating in Tennessee's individual market ACA exchange asked for massive rate hikes this year, ranging from 44-62%. Blue Cross Blue Shield asked for 62% in the first place; Cigna and Humana resubmitted their original requests for higher ones.

Tennessee's insurance regulator approved hefty rate increases for the three carriers on the Obamacare exchange in an attempt to stabilize the already-limited number of insurers in the state.

...BlueCross BlueShield of Tennessee is the only insurer to sell statewide and there was the possibility that Cigna and Humana would reduce their footprints or leave the market altogether.

This was a double headache: First, because the actual enrollment numbers were only available for 3 out of 11 carriers via the filings; I had to get the rest from the MA exchange's monthly dashboard report. Secondly, even with the dashboard report, I had to merge together 2 different enrollment numbers for each carrier due to MA's unique "ConnectorCare" program.

There are a few states which have technically expanded Medicaid under the ACA, but have done so using an approved waiver which allows them to actually enroll expansion-eligible residents in private Qualified Health Policies (QHPs)...using public Medicaid funding to do so. To be honest, this has always struck me as being essentially no different than someone simply receiving 99.9% APTC/CSR subsidies for enrolling in an exchange policy anyway; it's just a question of which pool of federal funds the subsidies come from. The two states which I know for a fact do it this way are Arkansas and New Hampshire, with Arkansas calling their "Private Medicaid Option" program the "Health Care Independence Program".

In any event, AR "Private Option" enrollees may be categorized as "Medicaid expansion" in the official reports, but for purposes of estimating the risk pool, they're included in with every other ACA-compliant private individual policies, whether on or off the ACA exchange.

Amidst my Aetna Postapalooza yesterday, there's one important point which other outlets have brought up which I haven't addressed yet: Pinal County, Arizona.

Since participation in the ACA exchanges has always been voluntary for carriers selling ACA-compliant individual policies (except for the District of Columbia (and until recently, Vermont), where carriers are legally required to only sell individual policies via the exchange), there's always been the danger that sooner or later there might be a situation where no carriers are selling on the exchange. Not "a few", not "only one"...zilch.

In my mind, I've always thought of this problem in statewide terms; it wasn't until 2015 that I even realized that many carriers only sell policies in some of the counties in a given state, not all of them. That makes the list of 300+ exchange carriers nationwide a bit misleading; some of the carriers listed for a given state might only be selling in a few or just a single county, making the scenario above far more likely to happen.

You may have noticed that I recently set up a GoFundMe account as an alternate method of letting people help keep ACASignups.net going as we enter the 4th Open Enrollment Period.

Until now I've exclusively used PayPal for donations, but decided to add GoFundMe as well to see how that works out.

In addition to my general gratitude, I should also note that anyone who makes a donation is added to the official ACA Signups mailing list. Once a week* I send out a weekly digest including a wrap-up of the past week, along with special bulletins when there's a major ACA-related development.

*(well, nearly every week...occasionally I'm a bit late...)

Under the “third party” arrangements, nonprofit organizations work as a front for medical care providers trying to win higher payments from private insurers that pay more than government programs like Medicaid, insurers say. For example, UnitedHealth Group last month sued a dialysis chain, American Renal Associates, alleging fraud. In its suit, UnitedHealth said American Renal hooked patients up with a charitable organization that helped patients pay their premiums, according to media reports.

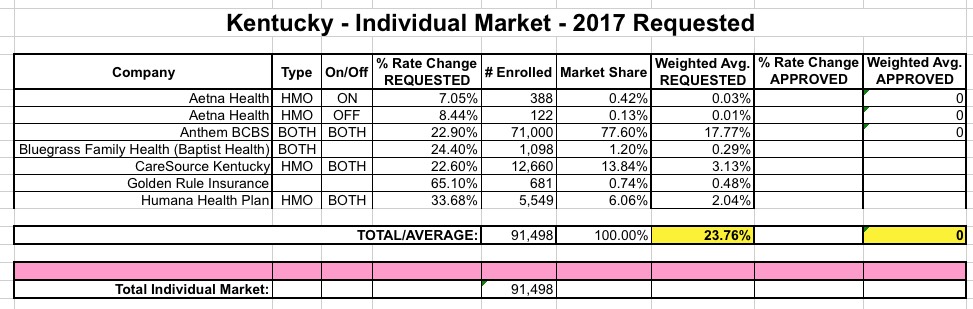

When I ran Kentucky's average requested rate hike numbers for the individual market back in May, I came up with a weighted average of 23.8%, but also cautioned that the weighting was likely based on less than 50% of the total ACA-compliant individual market state-wide.

Since then, it looks like a couple of the carriers resubmitted their filings with slightly different average requests, although nothing major. In fact, even Aetna dropping off the exchange doesn't change much, since it looks like they only have around 400 enrollees there anyway (plus, Aetna says they're sticking around the off-exchange market in "most" of the regions they're bailing on next year). Finally, as far as I can tell, Kentucky is among the states that Humana is not abandoning (though they might be reducing their footprint there?).

Anyway, just moments ago, according to SHADAC, the Kentucky DOI has posted their approved rates for the individual market:

Yesterday, in light of the Aetna announcement (coming on top of similar bombshells from UnitedHealthcare and Humana earlier this year), I took a stab at trying to calculate just how many current exchange-based enrollees will lose whatever plan they're currently enrolled in whether they want to switch to a different one or not. My conclusion is that up to 2 million of the 11 million or so will not, in fact, be able to "keep their plan if they like it" due to either the carrier going belly-up (4 more co-ops), the carrier pulling out of their county/state (UHC, Humana, Aetna) or the carrier dropping certain types of plans (BCBS of Minnesota). The number might be a few hundred thousand higher than that, actually, since there are other, smaller carriers here and there making changes to their plan offerings and/or participation levels.

This, of course, once again brings up President Obama's infamous "If You Like Your Policy, You Can Keep It!" promise, which he made a whole bunch of times throughout the contentious battle to get the ACA passed back in 2009-2010.

UPDATE: Wesley Sanders (via Twitter) pointed out that technically speaking, the headline above isn't quite accurate: In some cases, the enrollees in question will be automatically "mapped" to a different plan if they fail to actively shop around and pick a new policy themselves. So I suppose a more accurate headline would be "How many people will NOT have the same policy as of January 1st no matter what?"

The HHS guidelines indicate that an exchange cannot map enrollees to a plan offered by a different carrier. So if your health insurance carrier is exiting the exchange or pulling out of the individual market altogether – as is the case with 12 CO-OPs in November and December – the exchange generally won’t automatically re-enroll you in a similar plan from a different carrier. (New York State of Health made an exception for CO-OP members who lost coverage at the end of November.)

If your carrier is pulling out of the exchange but continuing to offer off-exchange coverage in your area, state regulations on guaranteed renewability will apply; the carrier may be able to auto-renew your coverage outside the exchange (which means you’d lose any premium subsidies and/or cost-sharing subsidies you were receiving in the exchange), or you may be directed to select a new plan during open enrollment.

That last paragraph is actually really important in the case of Aetna, who says that they plan on sticking around off-exchange in most of the areas that they're dropping on-exchange policies...if those enrollees aren't careful, they could end up "keeping their plans" after all...except that they'd suddenly go from paying, say, 20% of the full price to 100%.

UPDATE x2: OK, I've been informed by a source at the HHS Dept. that the above policies are NOT quite accurate after all:

"if an issuer no longer offers a particular plan, we work with states to enroll the consumer in as similar a plan, as best possible. Under some circumstances, this could be with a different issuer. (Of course, consumers still have the option to go back to HealthCare.gov and select a new plan during open enrollment.)

"Highlight #2 is not true."

I apologize for the confusion on this issue; it sounds like this policy may have changed for 2017. Louise assures me that she's updating her primer now.

Every year, both the HHS Dept. as well as myself make a point of strongly encouraging people to shop around, shop around, shop around when enrolling in ACA exchange policies, since doing so can usually result in a better deal being available. This remains the case this year: EVERYONE should shop around and see what's available, even if they end up sticking with the same plan in the end. You never know what you'll find.

However, there's a flip side to this advice: Every year, a substantial portion of current enrollees have no choice but to shop around, for a variety of reasons:

In 2013, a couple million people's policies were cancelled for not being ACA-compliant (about 5 million more were given a "transitional" period of up to three years, depending on the state).

In 2014, a million or so of those extended "transitional" policies expired. In addition, enrollees in Massachusetts, Maryland, Oregon and Nevada had to manually re-enroll whether they kept the same policy or not as those states switched to brand-new tech platforms.

In 2015, a dozen or so ACA-created Co-Ops failed, forcing around 800,000 people to have to shop around for a new carrier. Moda pulled out of a couple of states, Blue Cross dropped out of New Mexico and so on.

In 2016, 4 more co-ops have failed, plus the big drop-out announcements from UnitedHealthcare, Humana and Aetna.

In addition, throughout all 3 years, various carriers have dropped some types of policies in given states while retaining others...usually dropping PPOs but keeping HMOs, as Blue Cross did in Texas this year and is doing in Minnesota next year. In these cases, the enrollees may or may not have to switch carriers, but they will have to choose a different plan one way or the other.

Ever since the big Aetna news the other day, several people have asked me for my estimate of just how many people will have to shop around next year. Here's my best attempt to tally them up: