With only 5 days to go before the launch of the 2018 Open Enrollment Period, time is rapidly running out for me to wrap up my 2018 Rate Hike Project. I started this, as I have for 3 years now, back in late early May with the very first requested rate changes out of Virginia, and have been tracking all 50 states as the summer and fall have passed, following every twist and turn of the insane repeal/replace circus in Congress, Trump's bloviating and blathering about "blowing things up" and "letting Obamacare explode", the last-ditch "Graham-Cassidy" sideshow and everything else, right up to and through Trump lowering the boom on cutting off CSR reimbursement payments.

My 2018 Rate Hike project petered out a few weeks back with the requested rate increases posted for 46 out of 50 states (along with DC). Unfortunately, the last 4 states (Kansas, Missouri, Nevada and Utah) decided to keep their cards close to their chest, delaying any public viewing of even the requested rate increases for awhile longer.

Between updating the "Who could lose coverage" graphics, prepping for my town hall thing last night and updating the 2018 Rate Hike project, I've gotten way behind on my "Who's saying 'screw rate hikes, I'm just gonna bail completely next year' updates. Let's take care of that now, OK? The first three updates are courtesy of Louise Norris writing for healthinsurance.org; the fourth is vai Kimberly Leonard for the Washington Examiner:

Insurers in Idaho had to submit forms for 2018 plans by May 15, but they have until June 2 to file rates. Mountain Health CO-OP, SelectHealth, PacificSource and Blue Cross of Idaho all filed forms to continue to offer Your Health Idaho plans in 2018.

As I noted when I crunched the numbers for Texas, it's actually easier to figure out how many people would lose coverage if the ACA is repealed in non-expansion states because you can't rip away healthcare coverage from someone who you never provided it to in the first place.

Last week I noted that with 41 states accounted for and the 2017 Open Enrollment Period quickly bearing down on everyone, it was time to pull the plug on my 2017 Average Rate Hike project and move on. I had come up with an overall national weighted unsubsidized average rate increase of around 25% for ACA-compliant individual market plans.

However, I also noted that I'd make sure to fill in the approved rates for the remaining 10 states as they came in, for completeness sake...and today, thanks to the HHS Dept. cutting the ribbon on 2017 Window Shopping at HealthCare.Gov, I've also been able to fill in the blanks for five of the remaining states all in one shot (the other five remain elusive).

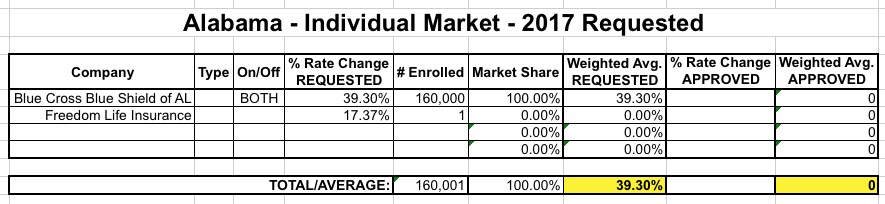

Lots of stuff happening fast & furious these days as #OE4 approaches. Instead of individual posts, I'm gonna cram 7 state updates into a single one...and am also cheating a bit by cribbing off of excellent work by Louise Norris over at healthinsurance.org (which is fair, since she also gets some of her data from me as well):

ALABAMA: Here's what my requested rate hike table looked like for Alabama on August 1st:

OK, there's something very odd going on with Missouri's 2017 rate filings for the individual market. According to the Kaiser Family Foundation, Missouri's entire individual market was around 344,000 people in 2014. While it's likely increased by around 25% since then, that would still only bring it up to around 430,000 people including both grandfathered and transitional enrollees, which sounds about right to me (290,000 enrolled via the ACA exchange, which would leave around 140,000 off-exchange).

And yet, when I plug in the official rate filings for Missouri's individual market for 2017, here's what it looks like:

Coalition cheers Health Insurance Rate Review bill passage

The House followed the Senate’s unanimous approval of SB 865, sponsored by Sen. David Sater, with a 140-6 vote, moving the “Health Insurance Rate Review” bill to the Governor’s desk on Tuesday.

In addition to rate review, the bill will modify provisions regarding licenses issued by the Board of Pharmacy and covered prescription benefits, delineates procedures for PBMs with regards to MAC lists, and requires health carriers to offer medication synchronization services.

The advancement was cheered by Missouri Health Care for All (MHCFA), who believe the bill will bring more transparency to insurance premiums.

When UnitedHealthcare announced last month that they were making good on their threat last fall to pull out of the individual market in over two dozen states next year, it caused shockwaves across the health insurance industry. It is an important development, as around 800,000 people will be impacted.

When Humana announced last week that they plan on pulling out of the individual market in at least 5 states next year, it was interesting and a bit of a bummer, but not nearly as earthshattering, because only about 25,000 people will have to shop around and find a new carrier.

Today, it is my duty to announce that Celtic insurance has also decided to pull out of the entire individual insurance market (both on and off-exchange) across at least 6 states, including:

When I was crunching the numbers to come up with my rough estimate of the weighted average rate increase requests for Florida yesterday, I had a revelation: While Healthcare.Gov's Rate Review database, frustratingly, only includes rate requests higher than 10% (thus ignoring dozens of requests of under 10%, or even rate reductions in some cases), it doesstill at least provide guidance as to what the maximum average could possibly be.

For instance, let's say that there's a state with 4 insurance carriers, each of which has exactly 10,000 enrollees. Two of them are asking for a 20% and 15% increase respectively. Since those are both above 10%, they'll both show up on the Rate Review site: