The Connecticut ACA exchange, AccessHealthCT, issued a press release today reminding Connecticut residents in general of the December 15th deadline for January 1st coverage. They also stressed, however, that while most current enrollees will be automatically renewed into either their existing policy, there are about 26,000 current enrollees who can't be auto-renewed because their carrier is leaving the exchange in 2017:

On December 1st, AHCT’s automatic renewal process began. The AHCT eligibility system will automatically enroll into 2017 coverage customers who have selected auto-renew and whose plans are still available. “But, there are 26,000 people who currently have coverage through AHCT who cannot auto-renew and must take action to renew their 2017 plans,” Wadleigh noted. Wadleigh reminds all customers “they should shop around and compare your options for 2017– that’s the purpose of the marketplace.”

As I've noted before, Connecticut has an unusual policy for reporting 2017 QHP selections. Instead of reporting the number of renewing enrollees + new additions, they start out by assuming every current enrollee will be renewed for the upcoming year, add the new additions and the subtract those who actively choose not to renew their policy. Technically, this makes it look like Connecticut has already broken 100,000 enrollees for 2017--over 80% of their enrollment target number--even though we're only 4 weeks into the enrollment period. As a result, I can't really give an accurate "enrolled for 2017" number until the third week of December, when every state has officially entered their autorenewed enrollees into the system.

Yesterday, the Access Health CT board meeting presentation gave the 2017 QHP selection tally as (I think) 9,455 renewals plus 6,630 new additions for a total of 16,085 people, though it's a little confusingly presented.

They don't really break out the "renewal" number, so I'm not certain what the total is, but assuming the 9,455 figure is accurate, that brings it up to 16,498, or 970/day.

If I'm reading this correctly, it looks like they currently have 85,250 people enrolled in effectuated exchange policies. 9,455 have actively renewed/re-enrolled into either their existing policy or a different one, plus another 5,570 brand-new enrollees who have signed up, for a total of 15,025 QHP selections for 2017.

What's confusing me is that they also say that "100,275 are currently enrolled"...which you only get by adding all 3 of those numbers together, which makes little sense to me.

First, it sounds like ConnectCare (the largest carrier on the CT exchange) is jumping on the "standardized plan" bandwagon, by offering what they call "Passage" exchange plans:

HMO-style, $5 co-pay for Primary Care Physician (PCP) visits (pre-deductible)

The Silver "Passage" plan would have a flat $50specialist co-pay

High-quality PC network included

Simple/easy to understand standardized plans

also offering "Passage" plans to small group / Medicare enrollees

--Standardized plans help but not enough; still lots of confusion about process, what's included/not included, etc; launching 4 retail "ConnectiCare Centers" to help people shop, enroll, member services, billing/payment issues, health/wellness assessments, education/outreach events

--CliniSanitas: Multicultural health delivery for hispanic/etc. members (3 centers; 100% bilingual services)

Over the past week or so there was a lot of tense negotiations and confusion about whether or not ConnectiCare, the 2nd largest carrier on Connecticut's exchange and the largest in CT's individual market overall, would bail on participating on AccessHealthCT next year. They bumped up their rate hike request not once but twice, from 14.3% to 17.4% to 27.1%, and when state regulators stuck with 17.4% and refused to budge any higher, they threatened to file a lawsuit and drop out of the exchange. As of last Friday, it looked like they were indeed pulling out.

Days after declaring it would leave the state’s health insurance exchange, ConnectiCare has decided not to drop out of the marketplace, much to the relief of many — including Gov. Dannel P. Malloy.

Lots of stuff happening fast & furious these days as #OE4 approaches. Instead of individual posts, I'm gonna cram 7 state updates into a single one...and am also cheating a bit by cribbing off of excellent work by Louise Norris over at healthinsurance.org (which is fair, since she also gets some of her data from me as well):

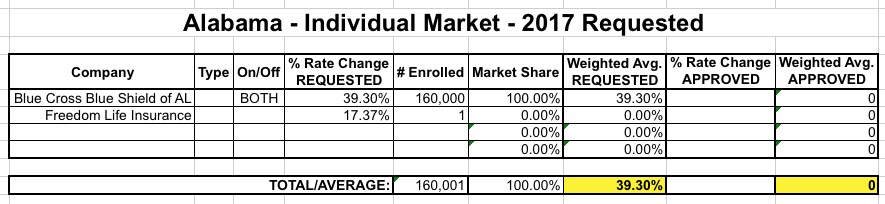

ALABAMA: Here's what my requested rate hike table looked like for Alabama on August 1st:

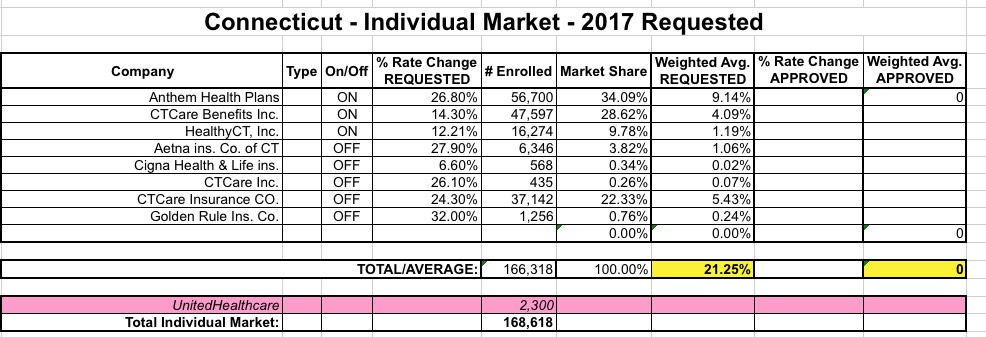

The Connecticut average requested rate hike has jumped around a lot over the summer. It started out at roughly 21.3% back in June, then increased to 22.2% after the HealthyCT Co-Op announced they were closing up shop. Then, several of the carriers submitted revised rate hike requests, bumping the average up further to around 26.8%.

Well, over the holiday weekend, the CT Mirror reports that the CT Dept. of Insurance released their response to the requests. There were also yet more last-minute filing changes. I've updated the spreadsheet with both the final requests as well as the approvals...but there are a copule of major blank spaces I still have to fill in:

Most Connecticut health insurance plans sold through individual and small group markets will undergo steep rate hikes next year, although in some cases, the prices will not go up by as much as carriers had sought.

OK, make that four states in which at least one major carrier has submitted an updated rate filing request since I originally estimated the statewide average.

Shortly after that, however, HealthyCT became the latest ACA-created Co-Op to fail, meaning their 16,000 or so current enrollees will have to shop around for new coverage next year. I revised the numbers accordingly and the average request bumped up a bit to 22.2%...

ACCESS HEALTH CT PROVIDES TRANSITIONAL MEDICAL ASSISTANCE ENROLLMENT UPDATE

2,846 individuals have enrolled in a new healthcare plan

Hartford, Conn. (July 8, 2016) - Access Health CT (AHCT) CEO Jim Wadleigh provided an update today on enrollment of approximately 13,811 parents and caregivers who will lose their Transitional Medical Assistance (TMA) on July 31st when they no longer meet the HUSKY A eligibility requirements due to a change in legislation last year. As of July 7, 2016, 2,846 individuals have enrolled in a new healthcare plan via the exchange. Of those, 1,966 applications have been re-determined eligible for coverage in a HUSKY program through the integrated eligibility system with the Department of Social Services, and 880 have enrolled in a Qualified Health Plan (QHP) with AHCT.