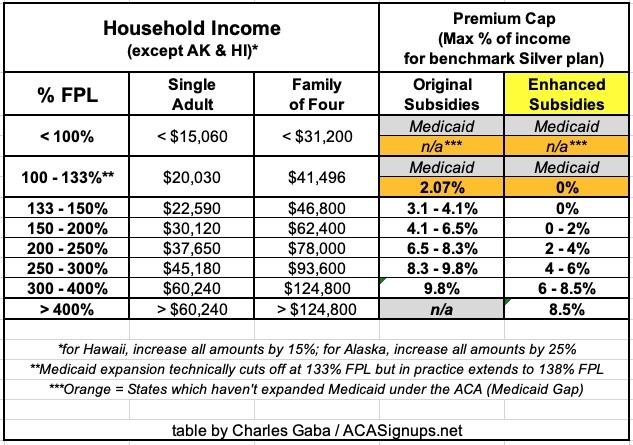

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

This is, of course, extremely important since household income is one of the most critical factors in calculating how much financial assistance enrollees receive (or if they're eligible for Advance Premium Tax Credits (ATPC) at all).

If you've ever wondered why healthcare wonks (myself included) almost never even bring up the ACA's Catastrophic Level plans and why the only time I ever discuss Platinum Plans is in the context of high-CSR enrollees being eligible for "Secret Platinum" plans (labeled as Silver), this table should explain why.

Next up: Age brackets, gender, racial/ethnic groups and urban/rural communities. I'm also throwing in the stand-alone Dental Plan table here for the heck of it since I don't know where else to include it.

I don't have a ton to say about any of these, really. It's always interesting to me to see that 1.7% of ACA exchange enrollees are 65 or older. Not sure why they aren't on Medicare but I'm sure there are logical reasons.

Now it's time to move on to the actual demographic breakout of the 2024 Open Enrollment Period (OEP) Qualified Health Plan (QHP) enrollees.

First up is breaking out new enrollees vs. existing enrollees who either actively re-enroll in an exchange plan for another year or who passively allow themselves to be automatically renewed into their current plan (or to be "mapped" to a similar plan if the current one is no longer available).

The table below has the data for both Qualified Health Plans (QHPs) in all 50 states + DC as well as Basic Health Plan (BHP) enrollment in Minnesota and New York only, compared to the 2023 OEP.

The official 2024 ACA Open Enrollment Period (OEP) ended last night in most states, but millions of Americans are still eligible to #GetCovered!

This is the best OEP ever for the ACA for several reasons:

The expanded/enhanced premium subsidies first introduced in 2021 via the American Rescue Plan, which make premiums more affordable for those who already qualified while expanding eligibility to millions who weren't previously eligible, are continuing through 2025 via the Inflation Reduction Act;

A dozen states are either launching or expanding their own state-based subsidy programs to make ACA plans even more affordable for their enrollees;

And remember, millions of people will be eligible for zero premium comprehensive major medical policies.

If you've never enrolled in an ACA healthcare policy before, or if you looked into it a few years back but weren't impressed, please give it another shot now. Thanks to these major improvements it's a whole different ballgame.

Here's some important things to know when you #GetCovered for 2024: