As I noted a few days ago, now that the 2019 ACA Open Enrollment Period is actually underway and the approved individual market premium rate changes have been posted publicly for every state, I'm finally able to go back and wrap up my 2019 Rate Hike Project for the nine states which I was still missing final numbers for.

As I further noted, the approved rates in most of those states didn't change much compared to the preliminary/requested rate changes I had already analyzed earlier this year:

I realize this may seem a bit late in the game seeing how the 2019 ACA Open Enrollment Period has already started, but I do like to be as complete and thorough as possible, and there were still 9 states missing final/approved premium rate change analyses as of yesterday which I wanted to check off my 2019 Rate Hike Project list.

Fortunately, RateReview.HealthCare.Gov has finally updated their database to include the approved rate changes for every state, which made it easy to take care of most of these.

Nebraska has a slightly confusing siutation, which is surprising since Medica is the only carrier offering ACA policies in the state, When I first took a look at the requested premium changes for 2019 back in August, it looked like the average was around 1.0%...that was based on splitting the difference between the 3.69% and -2.60% listings, since the filing form was redacted and I didn't know what the relative market split was between Medica's product lines.

I realize this may seem a bit late in the game seeing how the 2019 ACA Open Enrollment Period has already started, but I do like to be as complete and thorough as possible, and there were still 9 states missing final/approved premium rate change analyses as of yesterday which I wanted to check off my 2019 Rate Hike Project list.

Fortunately, RateReview.HealthCare.Gov has finally updated their database to include the approved rate changes for every state, which made it easy to take care of most of these.

However, while state insurance regulators left one of the three carriers offering individual market policies alone, they knocked the other two down substantially: CareSource was lowered from around 13.1% to 9.5%, while Highmark Blue Cross Blue Shield was lowered from an average of 15.9% to 9.0%.

I realize this may seem a bit late in the game seeing how the 2019 ACA Open Enrollment Period has already started, but I do like to be as complete and thorough as possible, and there were still 9 states missing final/approved premium rate change analyses as of yesterday which I wanted to check off my 2019 Rate Hike Project list.

Fortunately, RateReview.HealthCare.Gov has finally updated their database to include the approved rate changes for every state, which made it easy to take care of most of these. In addition, in a few states the insurance department has also posted their own final/approved rate summary.

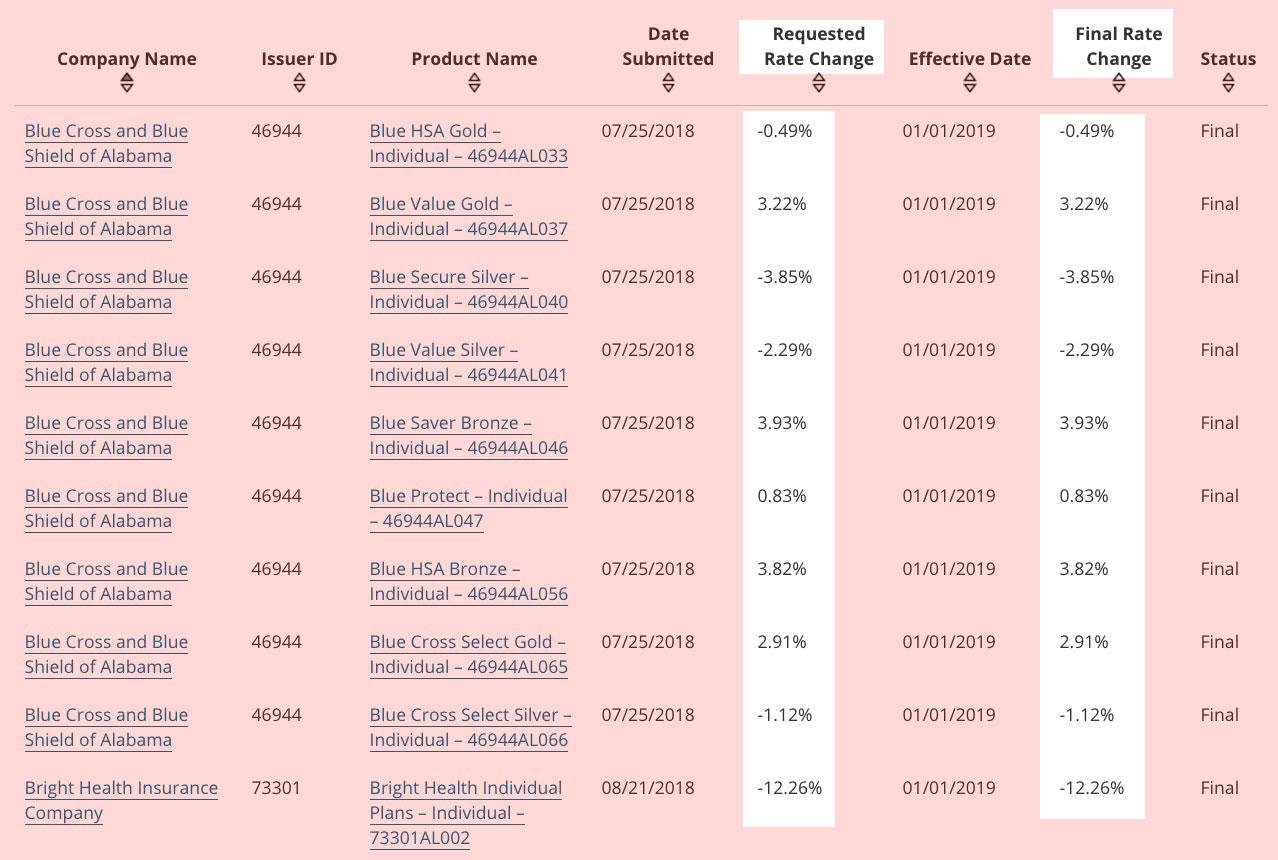

I realize this may seem a bit late in the game seeing how the 2019 ACA Open Enrollment Period has already started, but I do like to be as complete and thorough as possible, and there were still 9 states missing final/approved premium rate change analyses as of yesterday which I wanted to check off my 2019 Rate Hike Project list.

Fortunately, RateReview.HealthCare.Gov has finally updated their database to include the approved rate changes for every state, which made it easy to take care of most of these. Making things even easier (although not necessarily better from an enrollee perspective), in three states the approved rates are exactly what the requested rates were for every carrier: Alabama, Mississippi and Utah:

This is about as minor a rate filing update as I've had, but I'm posting it separately in the interest of completeness.

Insurance carriers in my home state of Michigan originally submitted their requested 2019 ACA individual market rate filings back in June. At the time, the average premium increase being asked for was pretty nominal, around 1.7%, with a smaller-than-average #ACASabotage factor of around 5% due to the ACA's Individual Mandate being repealed and #ShortAssPlans being expanded by the Trump Administration.

Today, just two days before the 2019 Open Enrollment Period actually begins, the Michigan Dept. of Financial Services finally posted the approved 2019 rate filings...and practically nothing ended up changing.

OK, this is a pretty minor update, but in the interest of completeness I should post it.

In mid-September, the Washington State insurance commissioner posted the approved 2019 average ACA individual market premium changes for carriers statewide, coming in at 13.8% overall.

The only problem is that the report only included the seven on-exchange ACA market carriers. The four carriers which offer off-exchange policies (which are pretty much identical and are part of the same risk pool, but don't qualify for tax credits) weren't included. They make up roughly 23% of Washington State's total individual market.

Today, just a few days before Open Enrollment begins, the WA Insurance Commissioner posted the complete approved rate change information. The overall average has dropped slightly, to 13.6%:

Eleven insurers approved to sell 74 plans in Washington's 2019 individual market

13.57 percent average rate increase approved

As regular readers know, every spring/summer I spend countless hours poring over the annual insurance carrier rate filings, plugging in increases (and occasionally decreases) in ACA-compliant premium changes for every carrier in every state. I actually do this twice for most states (and occasionally even three times), as the process moves from preliminary/requested rate changes to "semifinal" rates to "final/approved" rates throughout the fall.

For 2018 and again for 2019, I've taken this one step further; instead of simply running the overall weighted average premium changes in each state, I've also attempted to break out what portion of the change is caused by various factors...in particular, what portion is caused by legislative or regulatory changes by Congressional Republicans and/or the Trump Administration.

One of the great strengths and dangers of the ACA is that it includes tools for individual states to modify the law to some degree by improving how it works at the local level. The main way this can be done is something called a "Section 1332 State Innovation Waiver":

Section 1332 of the Affordable Care Act (ACA) permits a state to apply for a State Innovation Waiver to pursue innovative strategies for providing their residents with access to high quality, affordable health insurance while retaining the basic protections of the ACA.

State Innovation Waivers allow states to implement innovative ways to provide access to quality health care that is at least as comprehensive and affordable as would be provided absent the waiver, provides coverage to a comparable number of residents of the state as would be provided coverage absent a waiver, and does not increase the federal deficit.

OK, I had kind of forgotten about this. Back in early June, insurance carriers in Pennsylvania submitted their preliminary 2019 ACA market premium change requests. At the time, they averaged around a 4.9% increase statewide, which seemed pretty impressive under the circumstances.

Then, late July, the PA insurance department issued a press release stating that state regulators had modified the 2019 requests, and that the new, revised average was much lower...a mere 0.7% average rate hike. However, the individual carriers as well as the insurance department made it very clear that this nominal increase included a 6 point rate increase to account for the ACA's individual mandate being repealed and the Trump Administration's expansion of non-ACA compliant short-term and association plans.