It's been a year and a half since my last exclusive piece for healthinsurance.org, but I'm back, baby!

In my latest story for them, I explain that while the "ACA Sabotage!" card which Democrats have been playing against the GOP all year is very much real, it's also harder to explain to people in light of seemingly modest premium rate changes for 2019.

To understand both the reality and the difficulty in conveying it, read on!

As I noted back in June, the Ohio Insurance Dept. doesn't seem to like providing a whole lot of detail about their insurance rate filings on their website; at the time, they only stated the following regarding the preliminary 2019 individual market rate filings:

In 2018, 8 companies sold health insurance products on the exchange in Ohio and 42 counties had just one insurer with an additional 20 counties having only two.

For 2019, 10 companies have filed rates and forms for the Department to review and all 88 counties will have at least one insurer. Preliminary filings show 16 counties with just one insurer and 33 counties with two.

CMS Administrator Seema Verma is difficult to get a read on. On the one hand, she glories in trashing the ACA every chance she gets while happily endorsing nearly every effort to undermine or sabotage it, including repeal of the individual mandate, slashing the marketing and outreach budgets and so forth. Last year she was even busted trying to (effectively) blackmail the insurance carriers at large by offering to push through CSR reimbursement payment in return for them supporting the GOP's Obamacare repeal bill.

Vermont's situation is unusual compared to most other states for a couple of reasons. First of all, VT is one of only two states (Massachusetts is the other one) which has merged their Individual and Small Group market risk pools into one to help stabilize both markets. This is something I wish every state would do, frankly, although it's probably a lot easier to do in deep blue states (and Vermont having such a small population probably made it easier as well).

A few weeks ago, I posted about New Jersey's preliminary 2019 ACA-compliant individual market rate filings. At the time, the official New Jersey Dept. of Banking & Insurance specifically stated that:

Because Congressional Republicans repealed the ACA's Individual Mandate Penalty, carriers were planning on increasing 2019 premiums by 12.6% on average, in part to account for the adverse selection which was expected to happen next year.

However, thanks to the Democratically-controlled New Jersey state legislature and Governor swiftly reinstating the ACA individual mandate, actual 2019 rate filings are only expected to increase rates an average of 5.8%, saving the average unsubsidized indy market enrollee around $470 apiece next year.

Finally, the NJ legislature also passed, and Governor Murphy signed into law, a robust reinsurance bill which, if approved by CMS, is expected to lower unsubsidized 2019 premiums by an additional 15 percentage points, for a final 2019 average premium reduction of around 9.2%.

It's also important to understand that New Jersey's portion of the funding for the proposed reinsurance program will be coming from the revenue generated by the reinstated mandate penalty itself.

The good news was that average unsubsidized 2019 ACA individual market premiums were expected to drop by about 5.7% after years of double-digit rate hikes.

The bad news was that due specifically to various types of deliberate sabotage by the Trump Administration and Congressional Republicans (primarily repeal of the individual mandate and expansion of #ShortAssPlans), that 5.7% drop was still a good 12 points or so higher than it otherwise would have been.

The ugly news was that due specifically to the Trump Administration's utterly unnecessary decision to freeze Risk Adjustment fund transfers in response to a lawsuit out of New Mexico, 2019 premiums would be hundreds of dollars higher still than they should have been for Blue Cross Blue Shield of Tennessee's 113,000 enrollees:

UPDATE: As noted in the comments below, it looks like Anthem won't be expanding to cover the entire state after all. Even so, this is a major improvement in the situation.

Every year, Virginia is the first state out of the gate with their preliminary healthcare premium rate changes for the following year, posting the initial rate requests in early May. For 2019, it originally looked like the carriers were asking for a statewide average increase of 15.2%, but I later corrected this to 13.4%.

However, these were just preliminary numbers. The requests still have to go through the rate review process, and the carriers often make other changes as well before the final deadlines pass.

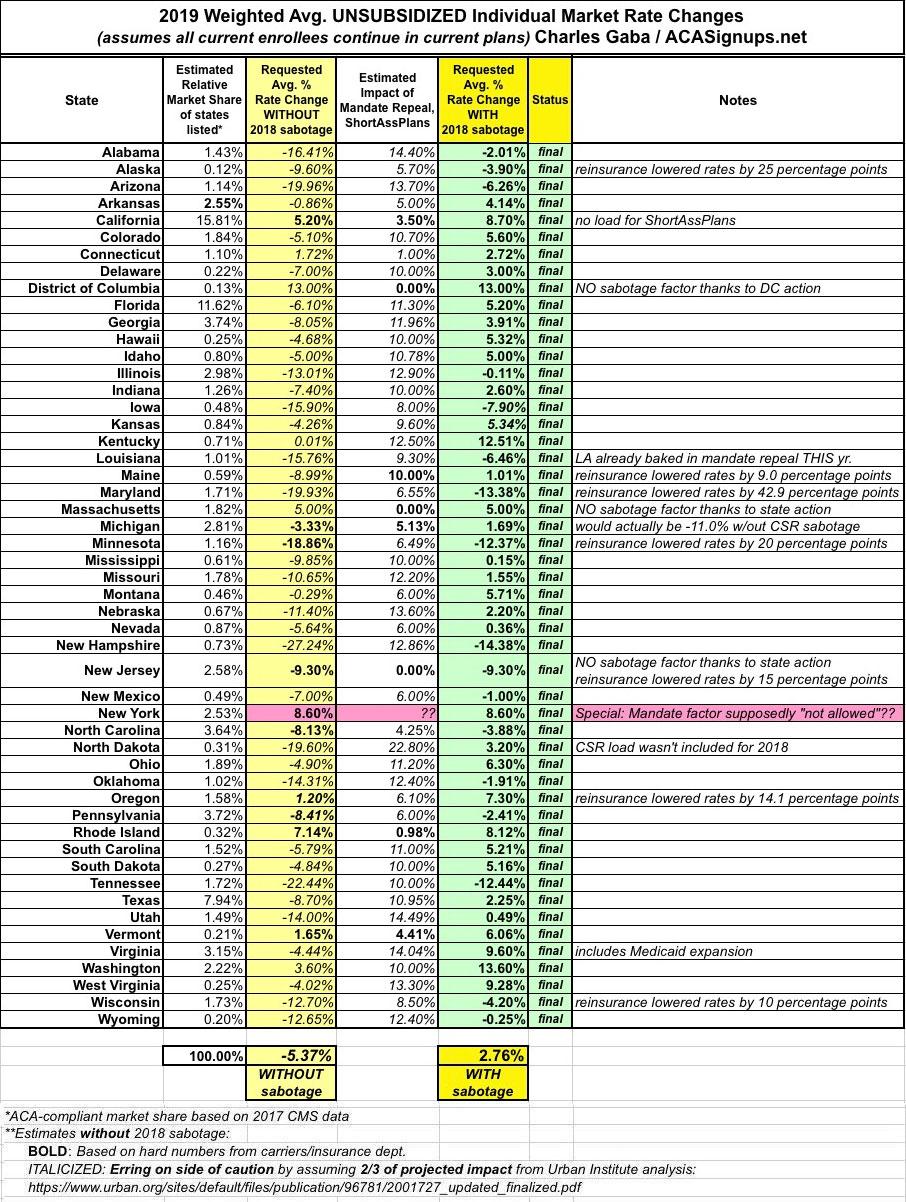

As regular readers know, each year I analyze hundreds of insurance carrier rate filings for the following year, then crunch the numbers to get an estimate of how much average premiums will increase (or in a few cases, decrease!) statewide.

As they also know, last year and again this year I've expanded on this by breaking out the portion of the annual rate increase which can be tied directly to sabotage efforts by the Trump Administration and Congressional Republicans. For 2018, this boiled down to roughly 17 points of the total nationwide increase being sabotage-related. It varied greatly by state, carrier and plan, but nationally, I estimated that without last year's ACA sabotage efforts, average premiums would have gone up around 11% instead of around 28%.

Annnnnnnnd finally, the least-populated state of them all...which also happens to be suffering from the highest average monthly premiums for unsubsidized individual market enrollees: Wyoming.

There's only a single carrier in the Equality State (seriously...that's their motto; who knew?), Blue Cross Blue Shield. They're actually looking to lower rates by just a smidge (0.25% on average).

Assuming just 2/3 of that to play it safe, that still means that unsubsidized enrollees would have been looking at roughly a 12% drop in their 2019 premiums without those measures...a difference of over $120/month, or a whopping $1,400 more apiece next year. Ouch.