New York: Final avg. 2022 #ACA rate changes:+3.7% individual market; +7.6% sm. group; DIFS saves NY residents over $600M

Mon, 10/11/2021 - 2:24pm

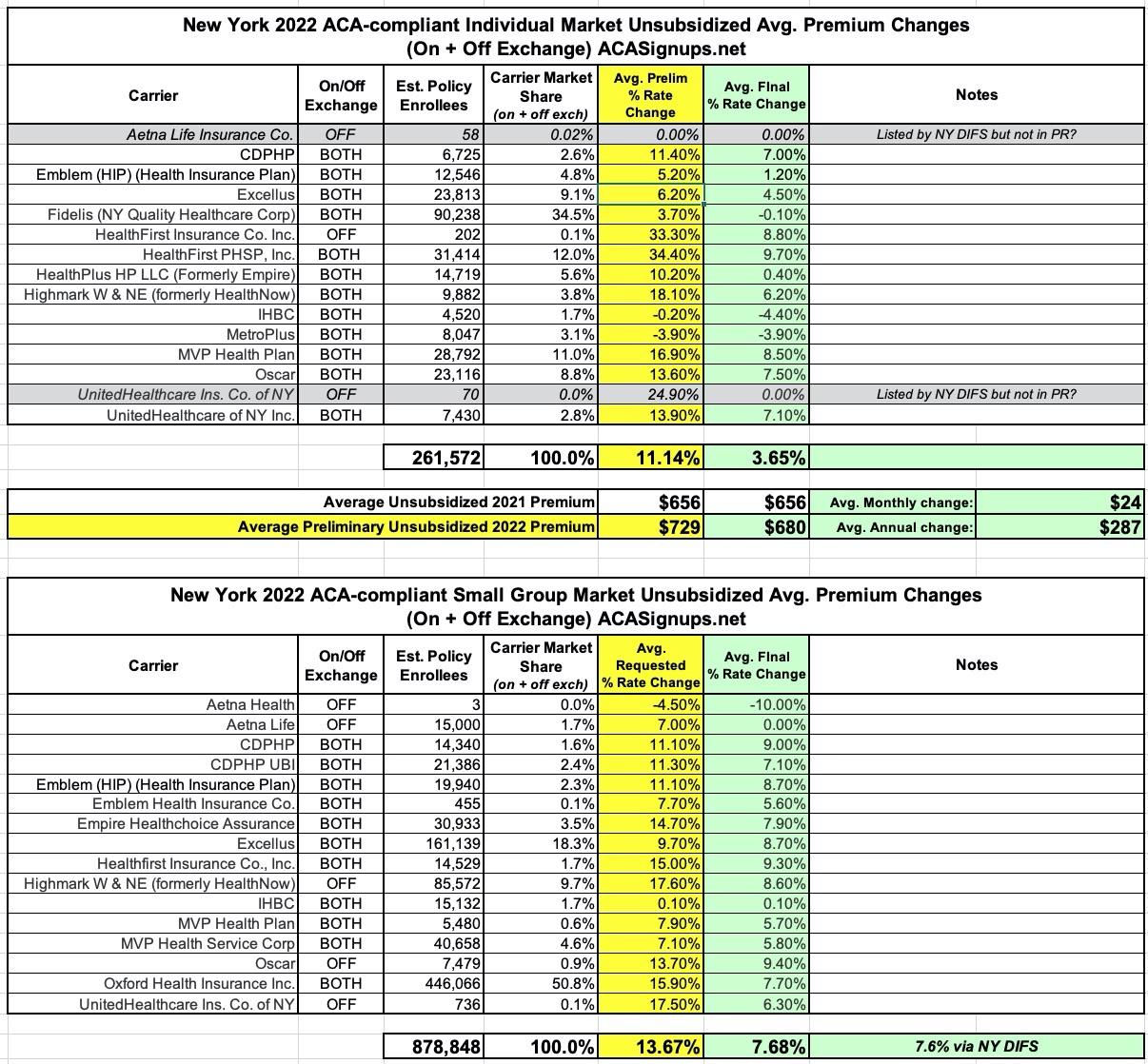

OK, I'm a wee bit behind on this one (the press release is dated August 13th!), but here's the final, approved 2022 premium rate changes for New York's individual and small group markets:

DFS ANNOUNCES 2022 HEALTH INSURANCE PREMIUM RATES, SAVING NEW YORKERS $607 MILLION

- As Health Care Costs Return to Pre-Pandemic Levels, DFS Protects Consumers Against Unjustified Rate Increases

- Rate Increases for Individual New Yorkers Held to 3.7%, a 67% Reduction in Insurers’ Requested Rates, Saving Consumers Over $138 Million

- Rate Increases for Small Groups Reduced By 46%, Saving Small Businesses Over $468 Million

- Increased Federal Subsidies Available through NY State of Health Mean More New Yorkers Will See Lowest Premium Levels in Recent Years

Superintendent of Financial Services Linda A. Lacewell announced today that the New York State Department of Financial Services (DFS) continues to protect consumers by reducing health insurers’ 2022 requested rates, despite health care costs increasing to pre-pandemic levels. Rates in the individual market will increase by only 3.7%, saving consumers over $138 million. In the small group market, insurers requested premium increases of 14.0% on average, which DFS reduced to 7.6%, saving small businesses over $468 million. Over 1.1 million New Yorkers are enrolled in individual and small group plans.

“New York has made huge strides in fighting the pandemic and ensuring New Yorkers are vaccinated. As the state continues to reopen, people have been seeking long-postponed non-essential and elective health services, increasing costs and putting pressure on premiums. However, particularly due to the economic fallout from the pandemic, we must strive to ensure that quality, affordable health care remains available to all New Yorkers,” said Superintendent Lacewell. “I’m proud of the work DFS has done to scrutinize these rate applications and save over $600 million in premium costs for New Yorkers. We will continue our other cost-reducing initiatives such as the Administrative Simplification Workgroup and the DFS Drug Advisory Board. Also, the Biden administration has restored confidence in the Affordable Care Act by increasing premium subsidies that will allow more people to purchase coverage and receive the health care they need.”

Enhanced Federal subsidies under the American Rescue Plan, enacted on March 11, 2021, lowers the cost of coverage available through NY State of Health to the lowest it has been in recent years. The amount of these tax credits depends on your income and where you live. For example, an individual earning $35,000 per year in New York City who was eligible for a tax credit of $359 per month, or $4,308 per year, is now eligible for a tax credit of $478 per month, or $5,736 per year. The law is designed so that no one will pay more than 8.5% of their income toward the benchmark plan available in their county. Over 60% of NY State of Health enrollees currently receive the federal Advance Premium Tax Credit (APTC).

As in prior years, the continued rise of health care costs is the main driver of premium rates. Medical claims decreased significantly in 2020 due to the postponement of elective and non-emergency services, but medical claims have increased in 2021 as New Yorkers catch up on medical appointments and postponed services. As a result, medical claims trends, the rate at which medical costs and utilization increase, have returned to pre-pandemic levels. The 2022 individual rates announced today are consistent with pre-pandemic premium rate increases. Drug costs account for the largest share of medical expenses (38.7%), followed by inpatient hospital costs (17.3%), primary care (8.1%), outpatient hospital costs (7.9%), and radiology (5.7%).

Individual Market

Approximately 264,000 New Yorkers are currently enrolled in individual commercial plans. DFS reduced insurers’ total weighted average increase requested for individuals by 67%, from 11.2% to 3.7%, the second lowest increase ever approved, saving consumers over $138 million. These rates will be further reduced for many consumers who are eligible for federal tax credits. Last year, 58% of individuals who enrolled in a Qualified Health Plan on the Marketplace received the federal Advance Premium Tax Credit (APTC). That number has grown to 63% in 2021 and is expected to grow further in 2022 as a result of the American Rescue Plan. Individuals who purchase the benchmark silver plan and receive the APTC are effectively held harmless from the impact of premium increases.

These rate decisions do not include the Essential Plan, available only through the NY State of Health, which as of June 1, 2021 has no premium for lower-income New Yorkers who qualify. More than 893,000 New Yorkers were enrolled in the Essential Plan as of May 31, 2021. While the full impact of the expanded subsidies is not expected to be fully realized until 2022, they are already having an effect. Individual enrollment, which typically decreases after March, increased in June by just over 1%, and more than 140,000 individuals are already benefitting from the enhanced tax credits.

...Small Group Market

Almost 900,000 New Yorkers are enrolled in small group plans, which cover employers with up to 100 employees. Insurers requested an average rate increase of 14.0% in the small group market. DFS cut the weighted average requested rate increases by 46% to 7.6% for 2022, saving small businesses over $468 million. A number of small businesses will also be eligible for tax credits that may lower those premium costs even further.

Hmmm...the actual rate filings only total up to 262,000 on the indy market and 879,000 for small group plans, but whatever. Oddly, there's two carriers on the individual market which appear in the NY DIFS rate filings as offering plans in 2022 but which don't show up in the press release. Then again, they only have 58 and 70 current enrollees respectively, so perhaps they just decided to drop out at the last minute or something? Huh.

Advertisement