Three GOP senators — Shelley Moore Capito, Susan Collins, and now Lisa Murkowski — all will vote "no" on the new plan to repeal and then replace the Affordable Care Act.

Why it matters: This guarantees what was already widely expected: that Senate Republicans wouldn't be any more successful with a straight repeal plan, without a replacement, than they were with the repeal-and-replace legislation that stalled yesterday. Republicans could only lose two votes.

What's next: Senate Republicans are still likely to schedule the vote — even if it fails — because they have to prove to conservative groups (and President Trump) that they've tried everything.

Then again, who the hell knows...

UPDATE 7/18/17: REPOSTING since Mitch McConnell is now back to a "repeal with a 2-year delay" strategy:

A few months ago, tech/media journalist Simon Owens interviewed me for a profile piece he wanted to write about ACASignups.net...basically, the whole story of how a Michigan website developer somehow became a national data/analysis source for All Things Obamacare. I had a couple of similar stories written about myself and the site by Sarah Kliff of Vox and Miranda Neubauer of TechPresident, but those were both over 3 years ago, in the midst of that insane first Open Enrollment Period, when the site was at peak media attention. I've been cited/quoted quite a bit since then, but most of that has been about the actual data and analysis, which of course makes sense.

UPDATE 7/20/17: The CBO score of BCRAP 2.0 has just been released, and while there are some tweaks/changes to their conclusions here and there, they still project about 22 million people to lose coverage by 2026 if BCRAP 2.0 is signed into law. They still expect about 15 million Medicaid enrollees to lose coverage by 2026. The only significant change on the "net loss of coverage" front is that they estimate that instead of 7 million people losing individual market coverage, they now project a net indy market reduction of 5 million...but also now expect about 2 million people with employer-based coverage to lose that, resulting in a net loss of...22 million.

I don't know if CAP plans on recrunching their numbers, since the BCRAP 2.0 bill still doesn't include the Cruz amendment which is supposedly going to be part of the final version voted on, but in the meantime, I'd imagine all numbers below could be updated by simply lowering all Individual Market column numbers by 29%...and just adding those numbers over to a new, Employer Coverage column.

Back on March 24th, a couple of hours after Paul Ryan pulled the House GOP's first ACA repeal vote, I posted the following:

CELEBRATE A FEW HOURS. Then come back and read this.

TRUMP'S PLAN B: Do everything he can to sabotage the ACA, then blame Democrats.

... there's the other doomsday possibilities, like Trump issuing an executive order stopping payment on CSR reimbursement payments to carriers.

I'll be addressing all of this and much more in the near future, of course, including my own suggestions for how the ACA should be changed to repair/improve the situation.

For the moment, however, I'm very tired, it's a beautiful Friday afternoon, and I'm going to go play with my kid for a few hours. I think I've earned it.

...and included this clip from the underrated film "Dead Again":

I've had to spend most of the afternoon/evening taking care of my kid (he has a 2-hour karate class Monday evenings), so I'm just now getting a chance to actually read the CBO's score of the GOP Senate's BCRAP bill, beyond their general summary of the score which I simply posted verbatim (with a handful of highlights and notes) earlier today.

There's a lot to digest; I'm sure everyone's already heard the main lowlights/takeaways: 22 million losing coverage by 2026 (14 million kicked off of Medicaid, 7 million losing individual market coverage, 1 million miscellaneous/rounding, I presume), "deficit savings" of around $321 billion (giving Mitch McConnell $202 billion to try and buy the votes he needs from a handful of "moderate" Senators) and so on. I'll be writing my full analysis for tomorrow, though there's probably not much point in it, since every other healthcare reporter will already have beaten me to the punch.

However, there's one little bit which infuriates me so much I have to get it off my chest right now. But first, the setup:

(I don't have time for a full analysis right now, so I'm just highlighting some key points and making a couple of notes for the moment...plenty of other reporters/bloggers/wonks are furiously writing analysis right now as well, of course)

The Congressional Budget Office and the staff of the Joint Committee on Taxation (JCT) have completed an estimate of the direct spending and revenue effects of the Better Care Reconciliation Act of 2017, a Senate amendment in the nature of a substitute to H.R. 1628. CBO and JCT estimate that enacting this legislation would reduce the cumulative federal deficit over the 2017-2026 period by $321 billion. That amount is $202 billion more than the estimated net savings for the version of H.R. 1628 that was passed by the House of Representatives.

Louise Norris gave me a heads' up regarding the Indiana 2018 rate filings. Anthem BCBS and MDwise, which currently have around 46,000 and 30,800 exchange enrollees each, are dropping out next year, meaning nearly 77,000 people will have to shop around. Anthem is sticking around the off-exchange market....but only in a handful of counties. Norris indicates around 64,687 total Anthem enrollees; minus the 46K on-exchange, that leaves roughly 18.7K off-exchange enrollees, virtually all of whom are expected to drop due to Anthem dropping out of all but 5 counties (plus, of course, the large rate hike).

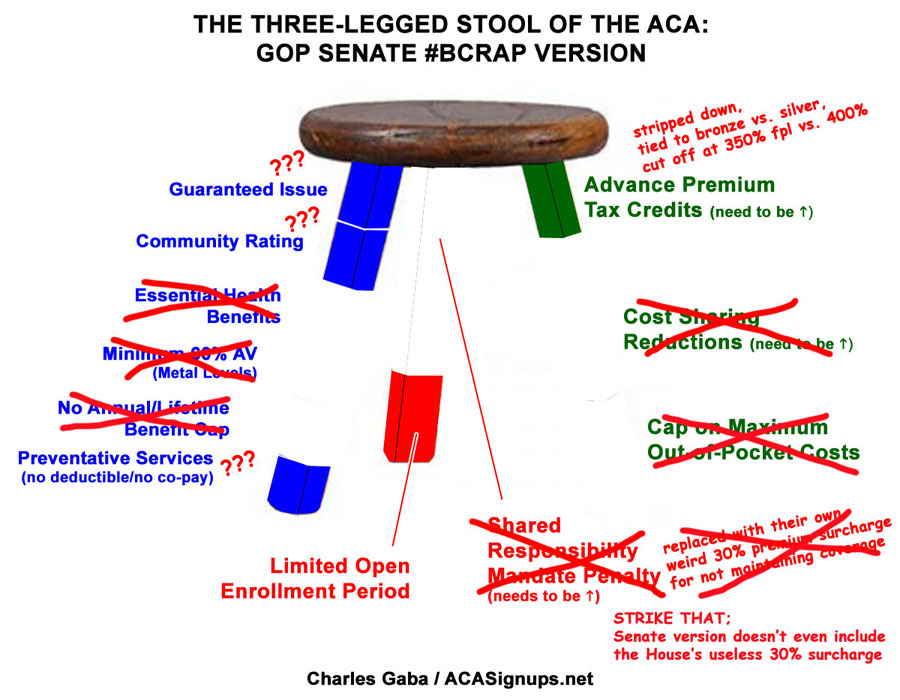

The other day it looked like the GOP Senate's BCRAP bill was going to take a hatchet to all 3 legs of the ACA's "three-legged stool", by getting rid of some provisions outright (CSR assistance and the Individual Mandate), weakening and slashing others in half (premium tax credits) and, most cynically, allowing virtually open-ended waivers which would allow individual states to wipe out many others (essential health benefits, minimum AV ratings, annual/lifetime benefits and the ACA's cap on maximum out of pocket costs). Here's what I figured this would make the "stool" metaphor look like:

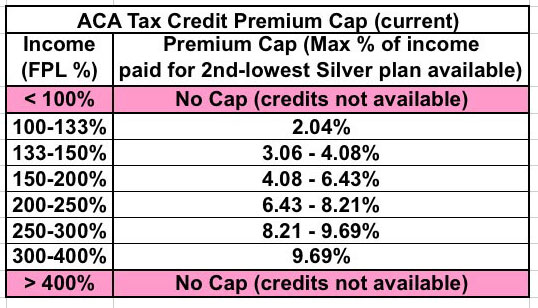

So, like everyone else, yesterday I was poring over the BCRAP text, and one of the first things which caught my eye was the individual market tax credit structure table, to see how it compares with the ACA's formula. Here's how it stands under the ACA...again, these percentages are based on the benchmark Silver policy...

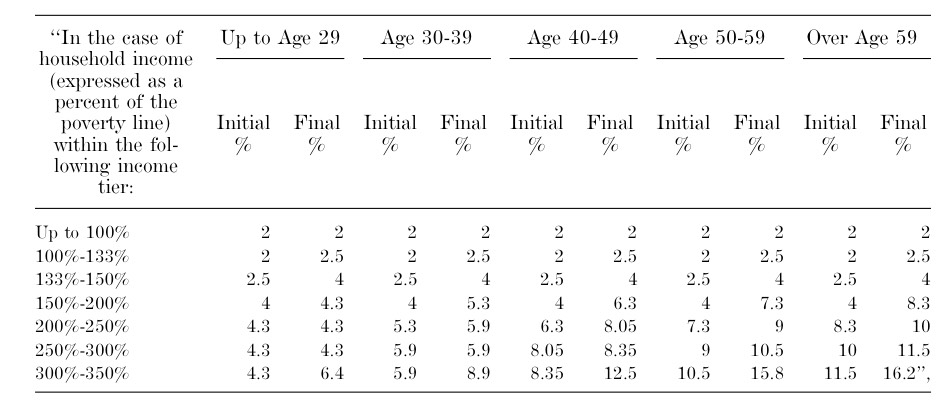

...and here's the BCRAP table, based on the benchmark Bronze policy:

After reviewing it for a few minutes late yesterday morning, I posted a tweet noting that under the ACA, a 60-year old earning about 300% of the Federal Poverty Line...roughly $37,000/year...only has to pay up to around $3,600/year in premiums for a Silver plan (9.69% of their income)...but under BCRAP, that same 60-year old would have to pay up to $6,000/year for a Bronze plan (16.2% of their income).

The tweet went viral...I think it was retweeted like 1,000 times or so over the next few hours.