New Analysis: Middle-class ACA enrollees are royally screwed if IRA subsidies expire next year

Tue, 10/22/2024 - 6:40pm

Back in June, I ran a state-by-state analysis which provided estimates of just how much various households would see their net individual market premiums jump starting in 2026 if the upgraded financial subsidies originally included in the American Rescue Plan Act (and later extended by the Inflation Reduction Act) are allowed to expire at the end of 2025, as is currently scheduled to happen without legislative action.

This week, the Robert Wood Johnson Foundation (RWJF)* has published their own take on the financial impact on enrollees if the IRA subsidies are allowed to expire. In this case, however, they're approaching it from a slightly different angle: They're focusing specifically on the approximately 1.7 million ACA exchange enrollees who earn more than 400% of the Federal Poverty Level (FPL).

*Disclosure: RWJF is a sponsor of this website.

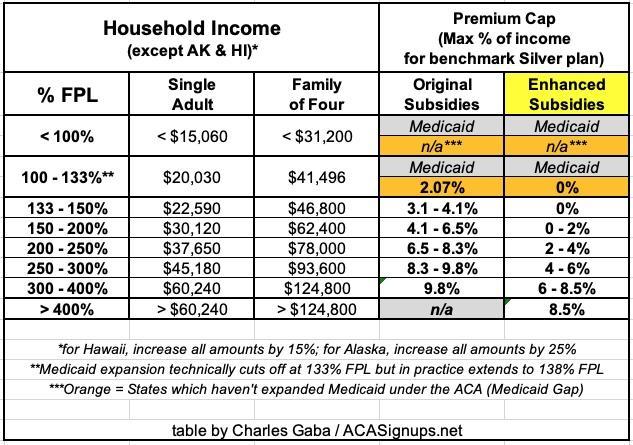

As a refresher, under the original subsidy formula of the ACA, enrollees who earn between 100 - 400% FPL are eligible for financial subsidies to reduce their monthly premiums on a sliding scale. The original ACA subsidies were somewhat generous for those earning 100 - 200% FPL and less so for those between 200 - 400% FPL...but disappeared entirely for any household earning more than 400% FPL. Earning even $1 more than the 400% FPL cutoff meant having to pay full price.

All of that changed thanks to the ARPA (and later the IRA). Under the new, far more generous subsidy formula, the premium subsidies are still available on a sliding scale, but a much more generous one at all levels...and significantly, there's no longer an arbitrary cut-off at 400% FPL. Under the IRA subsidy formula, no one has to pay more than 8.5% of their income for the benchmark Silver plan (as long as they're legally eligible otherwise).

However, what happens if we revert back to the original formula starting in January 2026? Remember, not only would those earning over 400% FPL have to start paying full price again, they'd have to pay full price including 6 years of medical inflation. The ARPA/IRA formula went into effect (retroactively) to the beginning of 2021, which means that if it expires at the end of next year, enrollees earning more than 4x the poverty level will be hit with the rate hikes from 2021, 2022, 2023, 2024, 2025 and 2026 in one shot.

What would that mean in practice? Here's what RWJF has to say about it:

Key Takeaways:

- For 50-year-old individuals earning 401% of the federal poverty level (FPL), $60,391 in 2024, enrolled in the second-lowest cost silver plan in their ZIP code, premiums would increase by a national average of 53% if enhanced premium tax credits expire.

- The average statewide second-lowest cost silver plan (SLS) premiums would at least double for 50-year-old individuals earning 401% FPL in five states: Alaska, West Virginia, Wyoming, Vermont, and Connecticut.

- In ZIP codes where 20% of the total U.S. population resides, premiums for the second-lowest cost silver plan would increase by 75% or more for a 50-year-old if enhanced premium tax credits expired for individuals above 401% FPL. In only 12% of U.S. ZIP codes scattered across 14 states, where 16% of U.S. residents reside, would a 50-year-old consumer experience a premium increase of less than 25% for the second-lowest cost silver plan.

...The enhanced PTCs have the largest dollar impact on three (not mutually exclusive) types of enrollees: 1) those with incomes above 400% FPL, 2) older adults, and 3) those who live in states, or areas of a state, where premiums are relatively high. If the enhanced PTCs are allowed to expire, these populations would experience massive increases in premiums.

People with incomes above 400% FPL

For those with incomes above 400% FPL, the impact of the enhanced PTCs is transformative. Previously, people in this income category received no tax credit at all and faced the full cost of coverage, a situation commonly referred to as the "subsidy cliff." Not surprisingly, enrollment for this population was very low because few could afford premiums, which in some situations comprised 20% of their income or more. Yet, with the enhanced PTCs, premium costs for this group are capped at 8.5% of income. Currently, a person with an income of $60,391 (Plan Year (PY) 2024, 401% FPL) would pay no more than 8.5% of their income for coverage, which translates to a monthly premium of $428. Approximately 1.7 million individuals with incomes above 400% FPL got coverage in the ACA marketplace in 2024, a trend that is expected to continue in 2025.

Older adults

Older adults, a large and growing share of marketplace enrollees, are also major beneficiaries of the enhanced PTCs because they face higher costs of coverage. In 2024, approximately 7.5 million adults over age 50 enrolled in marketplace coverage, more than one-third of the total enrollment. The largest group of enrollees were aged 55-64 years. Given demographic and labor force trends, the share of enrollees who are older is likely to continue to grow. Older enrollees face higher costs because ACA premiums are generally age-rated. In most states there is a 3:1 ratio of premiums for the oldest versus the youngest enrollees, meaning that the premium of a 60-year-old is triple the price of the premium of a 24-year-old. For many older enrollees, the enhanced tax credits have made it possible for them to afford coverage.

Residents of high-cost states

Finally, the enhanced PTCs have a heightened importance in states where the cost of coverage is high relative to the national average. In states like Alaska, West Virginia, and Wyoming, healthcare costs are high due to factors such as the health status of residents, lack of competitiveness in provider markets, or supply chain costs associated with long distances. Rural areas, in general, are more likely to be high-cost, a problem discussed in a recent assessment of the importance of the tax credits in farm states.

House & Senate Democrats as well as VP Kamala Harris support making the upgraded subsidies permanent. House & Senate Republicans, including Donald Trump, want to allow them to expire at the end of 2025.

I urge folks to read the entire analysis, and vote accordingly.

Advertisement