Oregon: *Final* Avg. Unsubsidized 2024 #ACA Rate Change: +6.2% (updated)

Tue, 09/05/2023 - 10:15am

(original post: 5/22/23)

Via the Oregon Dept. of Consumer & Business Services (Division of Financial Regulation):

Salem – Oregon consumers can get a first look at requested rates for 2024 individual and small group health insurance plans, the Oregon Department of Consumer and Business Services (DCBS) announced today.

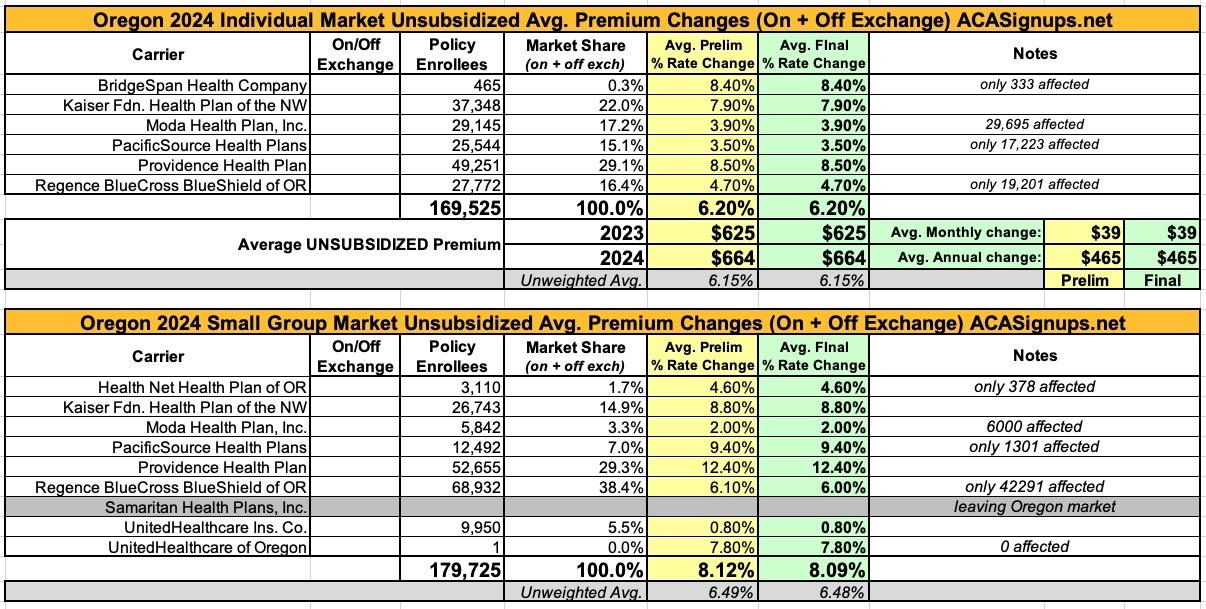

In the individual market, six companies submitted rate change requests ranging from an average 3.5 percent to 8.5 percent increase, for a weighted average increase of 6.2 percent. That average increase is slightly lower than last year's requested weighted average increase of 6.7 percent.

In the small group market, eight companies submitted rate change requests ranging from an average 0.8 percent to 12.4 percent increase, for a weighted average increase of 8.1 percent, which is higher than last year's requested 6.9 percent average increase.

The Oregon Reinsurance Program continues to help stabilize the market and lower rates. Reinsurance lowered rates by at least 6 percent for the sixth straight year.

See the attached chart for the full list of rate change requests.

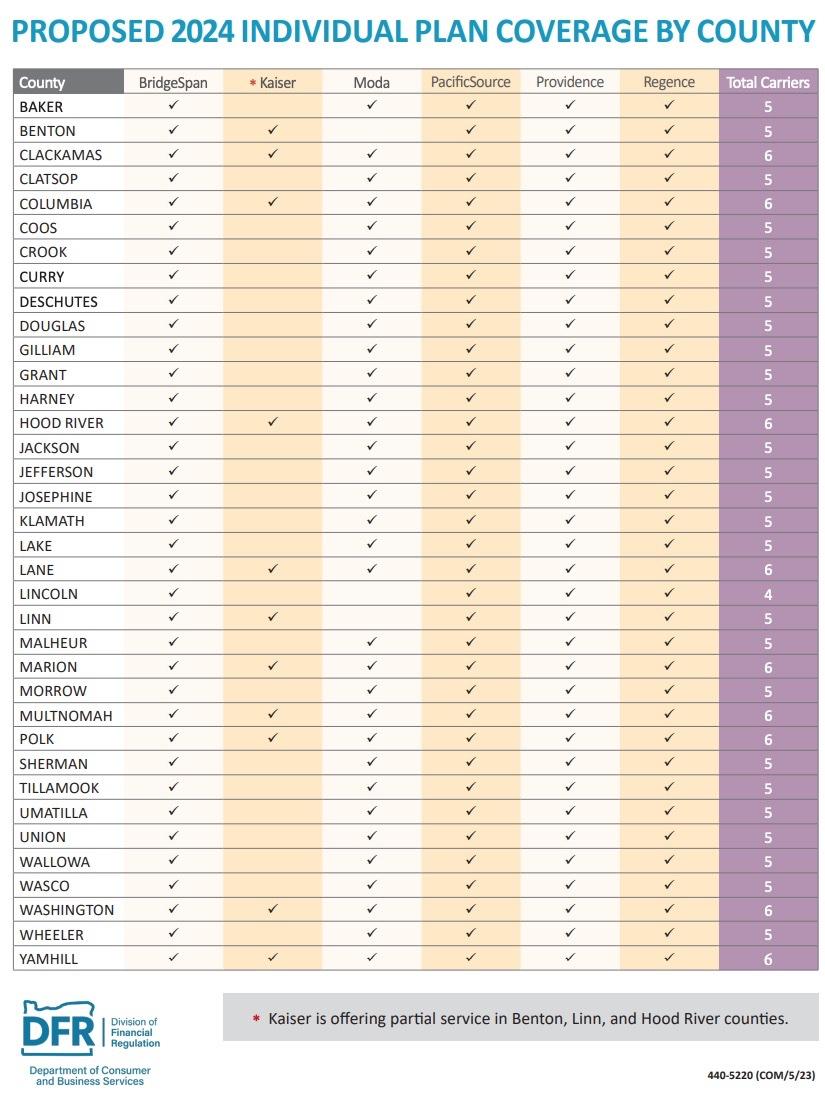

“We continue to have a strong and competitive insurance marketplace with at least four carriers offering plans in every Oregon county," said Insurance Commissioner and DCBS Director Andrew Stolfi. “In light of the high inflation and increasing labor costs across the country, we are encouraged that the individual market's overall average requests were lower than last year. We still have a lot of options for Oregonians to choose from and the Oregon Reinsurance Program continues to allow Oregonians to find reasonable rates."

Virtual public hearings about the 2024 requested health insurance rates will be held July 17-18 from 1:30-4:30 p.m. A web address to watch the public hearings will be posted at oregonhealthrates.org. At the hearings, each insurance company will provide a brief presentation about its rate increase requests, answer questions from Division of Financial Regulation (DFR) staff, and hear public comment from Oregonians. The public also has the opportunity to comment on the proposed rates at any time at oregonhealthrates.org now through June 30.

“We look forward to putting these rate requests through a rigorous public review, and we encourage the public to join the virtual public hearings and provide feedback on their health insurance plans," Stolfi said.

The requested rates are for plans that comply with the Affordable Care Act for small businesses and individuals who buy their own coverage rather than getting it through an employer. For the second year in a row, every county has at least four companies available for people to buy insurance on the individual market. Deschutes County, which has four companies in 2023, is proposed to have five in 2024.

Over the next two months, the division will analyze the requested rates to ensure they adequately cover Oregonians' health care costs. DFR must review and approve rates before they are charged to policyholders.

Preliminary decisions are expected to be announced in July, and final decisions will be made in August after the public hearings and comment period ends.

Here's the spreadsheet. It's worth noting that some of the carriers state that not all of their current enrollees will be impacted by rate changes, since not every plan they offer will be seeing a rate increase. What's more curious, however, is that in some cases they report that more people will be impacted than they currently have enrolled (see Moda on both markets):

UPDATE 9/05/23: The Oregon DFR has posted the final/approved rate decisions, and they've left both the individual and small group requests virtually untouched (only 1 small group carrier had its request modified and even that was only by a slight amount):

Here's the justification for the rate hikes cited by some of the individual market carriers;

BRIDGESPAN:

The following components are significant factors contributing to the proposed rate change: healthcare inflation and utilization increases, market morbidity increase and changes in benefits.

Healthcare Inflation and Utilization Increases: These adjustments refer to what is commonly known as healthcare trend. They reflect contractual changes in the carrier’s payments to healthcare providers and expected changes in the volume and types of services utilized by a carrier’s members.

Market Morbidity Increase: Medicaid redetermination and an otherwise shrinking market would lead to an increase in market average morbidity as relatively sicker members will enter and healthier members will leave the market.

Changes in Benefits: These adjustments refer to changes in covered benefits or plan design changes. Member-cost sharing changes resulted in leaner plans, leading to a decrease in the average plan factor.

PROVIDENCE:

Trend: Healthcare inflation is expected to increase. This estimate is based on expected changes to provider contract arrangements and utilization increases that includes both the volume and the mix of services.

Providence anticipates continued COVID-19 booster shots. With the end of the emergency order, we anticipate paying higher ingredient costs, adding 0.3% to trend.

REGENCE:

The following components are significant factors contributing to the proposed rate change: healthcare inflation and utilization increases, market morbidity increase and favorable financial experience.

Healthcare Inflation and Utilization Increases: These adjustments refer to what is commonly known as healthcare trend. They reflect contractual changes in the carrier’s payments to healthcare providers and expected changes in the volume and types of services utilized by a carrier’s members.

Market Morbidity Increase: Medicaid redetermination and an otherwise shrinking market will lead to an increase in market average morbidity as relatively sicker members will enter and healthier members will leave the market.

Favorable Financial Experience: Each year, RBCBSO evaluates its most recent financial results in the Oregon Individual market and incorporates that information into pricing.

Advertisement