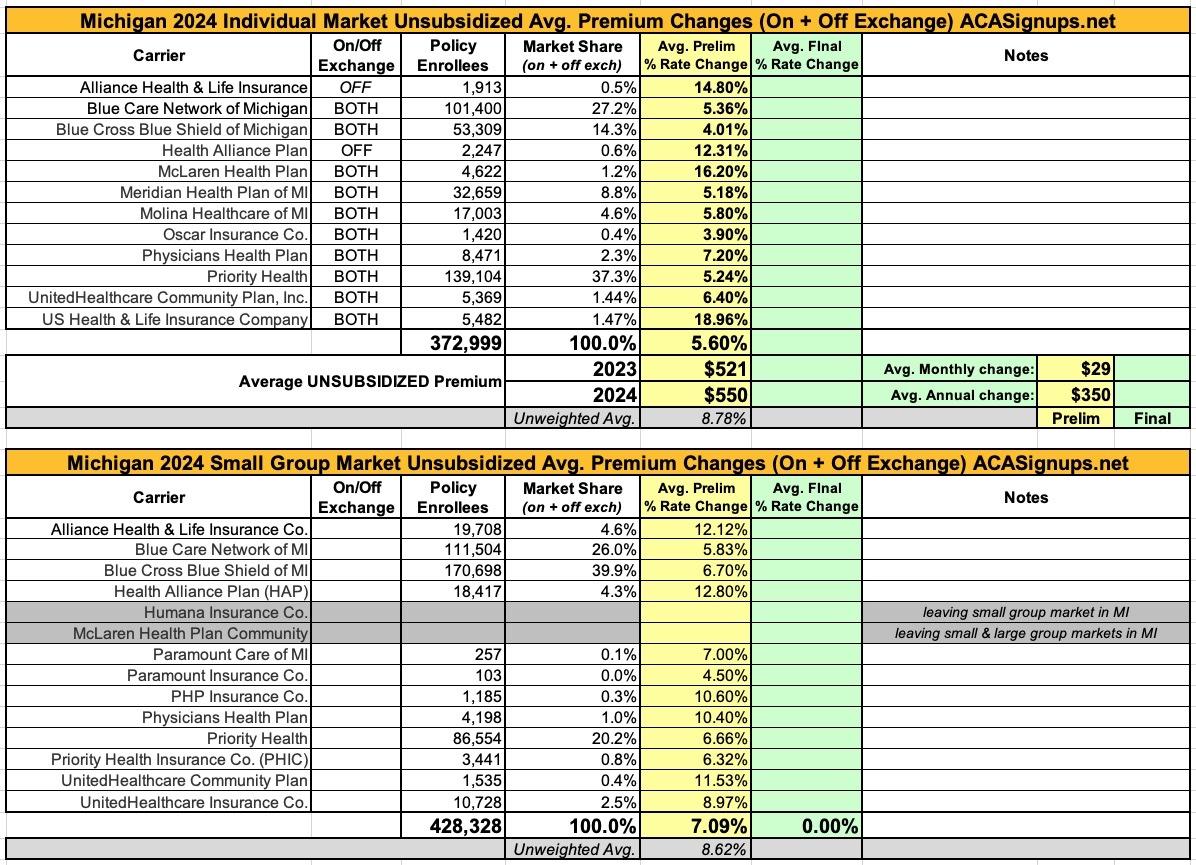

Michigan: Preliminary Avg. Unsubsidized 2024 #ACA Rate Change: +5.5%

Tue, 06/06/2023 - 8:07am

7/10/23: See update below

The Michigan Dept. of Financial Services hasn't issued any press release yet, but nearly all 2024 preliminary rate filings for the MI individual and small group markets are available via the SERFF database.

The only one missing as of today is UnitedHealthcare Community Plan, Inc.; they have most of their 2024 forms on record but there's no Actuarial Memo or URRT form included for the individual market, so I can't seem to find their actual requested rate changes or their enrollment as of March 2023.

In any event, I'm not seeing anything too odd here. Unlike other states with preliminary filings so far this year, Michigan carriers are seeking a fairly reasonable 5.6% average rate hike on the individual market and 7.0% for the small group market.

It's worth noting that two of the three indy market carriers asking for double-digit rate hikes (Alliance and HAP) both only offer off-exchange policies. The third, MacLaren, is also pulling out of the small group market entirely. It's also possible that Humana is dropping out of the small group market, although I'm not sure about that one.

One number I'm a little suspicious of is Priority Health's supposed 159K enrollment in the individual market. The numbers add up from their filing but I find it difficult to believe that they've quietly grown to have nearly as much individual market enrollment as BCBSM & BCN combined. Huh.

UPDATE 7/10/23: Michigan DIFS posted the official preliminary rate chart today; there were some slight modifications to a few of the rate changes and enrollment numbers, but nothing more than a rounding error. The biggest change was to Priority Health's enrollment (it's been knocked down to 139K) as well as filling in UHC Community Plan's enrollment number.

I actually get a weighted average of 5.6% vs. DIFS's 5.5%, probably because they round the rate changes off to the nearest tenth of a percent.

Blue Care Network:

BCN is filing a year-over-year average rate increase for 2024 for all individual products that were offered in 2023 of 5.36%. Significant drivers of the rate change include:

- Medical inflation and increased utilization as described in Section 5 of this memorandum

- Restates and true up of experience

- Risk Adjustment

- Plan Benefit Changes

Additional detail around the assumptions utilized in the rate development process is included in the following sections of this memorandum.

Blue Cross Blue Shield of MI:

BCBSM is filing a year-over-year average rate increase for 2024 for all individual products that were offered in 2023 of 4.01%. Significant drivers of the rate change include:

- Medical inflation and increased utilization as described in Section 5 of this memorandum

- Restates and true up of experience

- Risk Adjustment

- Plan Benefit Changes

Additional detail around the assumptions utilized in the rate development process is included in the following sections of this memorandum.

Meridian:

The following describes and quantifies the significant drivers underlying the proposed rate change for 2024. This breakdown is intended only for explanatory purposes and is distinct from the development of rates, as described in the subsequent sections of this memorandum.

- Trended single risk pool experience and degree of healthcare management (-5.8% premium impact versus 2023 filed rates)

The individual single risk pool experience underlying the rate projections has been updated. The filed rates reflect expectations for utilization trends and healthcare management applied to experience. There is a full description of utilization trend and other projection factors applied to experience in Sections 6, “Trend Factors” and 7, “Adjustments to Trended EHB Allowed PMPM.” There is a full description of the Health Cost Guidelines in Section 8, “Manual Rate Adjustments”.- Unit Cost trend (7.8% premium impact versus 2023 filed rates)

Expected unit cost levels and reimbursement arrangements with providers have changed between 2022 and 2023.- Benefit Design and CSR Subsidies (-2.8% to 1.5% premium impact versus 2023 filed rates, varies by plan)

Meridian's 2024 rates assume no change in covered EHB or non-EHB benefits relative to benefits offered in 2023.The rates do reflect updated projections of actuarial value and cost sharing by plan, as described in Section 12, “Plan Adjusted Index Rate.” Premium rates continue to reflect the expectation that Meridian will not be reimbursed by the U.S. Department of Health and Human Services (HHS) for cost-sharing on CSR Silver plans. Enrollment projections reflect updated expectations regarding member plan selections by metal and CSR level.- Administrative Expenses and Profit (4.6% premium impact versus 2023 filed rates)

See Section 12, “Plan Adjusted Index Rate”, for details on projected non-benefit expenses.- Updated expectations regarding the impacts of COVID-19 in the rating period (-1.0% premium impact versus 2023 filed rates)

2024 rates reflect updated expectations regarding both direct expenditures and indirect cost impacts associated with the COVID-19 pandemic in the rating period.- Other

There are other components of the rate change. These components include capitation contracts and interactions

Physicians Health Plan:

- Actual 2022 individual ACA market claims experience

- Changes to plan benefit designs in 2024, which cause different rate increases by plan

- Changes to plan liability load due to the 2023 to 2024 change in membership distribution of CSR plans

- Updates to geographic rating factors, which cause different rate changes by region

- Anticipated medical and prescription drug cost inflation and utilization trends

- Changes in taxes, fees, and administrative expenses

- Anticipated changes to risk adjustment transfer payments

- Changes in prescription drug rebates

- Changes in market morbidity

McLaren (small group):

Re: Notification of Discontinuation of Small Group and Large Group Products

Dear Director Fox:

McLaren Health Plan Community (“McLaren”) is providing notice under MCL 500.2212b MCL 500.3712 of its intent to discontinue providing all small group and large group products in Michigan effective December 31, 2023. McLaren will continue to service groups through the end of their plan year, but in no case later than December 31, 2024.

McLaren regrets to inform the Department of Insurance and Financial Services (“DIFS”) of this decision, however, to ensure the long-term profitability and stability of its overall book of business, McLaren is shifting its focus to government program sponsored products. We appreciate the support from DIFS over the years.

...2. Market Impact – McLaren has the following membership in its small group and large group offerings:

- Small Group – 1,059 (approximately 115 small groups)

- Large Group – 11,003 (approximately 40 large groups)

Plans we are withdrawing:

McLaren is exiting the small group and large group in its entirety. We intend to discontinue offering coverage for all groups with renewal dates beginning on or after December 31, 2023. Groups that renewed prior to December 31, 2023 will continue coverage until the end of the plan year (carrying into 2024). We do not intend to file rates and plans for the small group or large group markets for coverage beginning in 2024.

Advertisement