Updated: New York: The Mystery of NY DFS's "55% Lower" Obsession

Wed, 08/14/2019 - 10:40am

Over the weekend, the New York Department of Financial Services issued a press release announcing approved 2020 ACA-compliant Individual and Small Group premium rate changes:

DFS ANNOUNCES 2020 PREMIUM RATES: LOWERS OVERALL REQUESTED RATES FOR INDIVIDUALS AND SMALL BUSINESSES TO PROTECT CONSUMERS AND FUEL A COMPETITIVE HEALTH INSURANCE MARKETPLACE

- New York Rates for Individuals More Than 55% Lower Than Before Implementation of the Affordable Care Act, After Adjusting for Inflation and Before Federal Tax Credits

- DFS Reduced Overall Insurers' Requested Rate for Individual Coverage from 9.2% to 6.8%, a Reduction of 26%, Saving Consumers over $50 Million

- DFS Cuts Overall Insurers' Requested Rate for Small Group Coverage from 12.2% to 7.9%, a Reduction of 35%, Saving Small Businesses over $313 Million

- Overall, Consumers Who Receive Tax Credits for the Most Popular Silver Plan Will See No Increase in Premiums in 2020

I already posted my writeup about NY's 2020 rate changes, but something about the "55% Lower than Before the ACA" bullet kept bothering me about the press release, so I decided to do a little research:

DFS TAKES ACTION TO ENSURE A CONTINUED HEALTHY AND COMPETITIVE 2019 NEW YORK HEALTH INSURANCE MARKET DESPITE CONTINUED WRONGFUL FEDERAL ATTACKS ON THE AFFORDABLE CARE ACT

New York Rates for Individuals More Than 55% Lower Than Before Implementation of the Affordable Care Act, After Adjusting for Inflation and Before Federal Tax Credits

DFS ANNOUNCES 2018 HEALTH INSURANCE RATES IN A CONTINUED ROBUST NEW YORK MARKET

Rates for Individuals More Than 55% Lower Than Before Implementation of the Affordable Care Act, After Adjusting for Inflation and Before Federal Tax Credits

DEPARTMENT OF FINANCIAL SERVICES ANNOUNCES 2017 HEALTH INSURANCE RATES

Rates for individuals more than 55% lower than before establishment of New York’s Health Exchange, adjusted for inflation.

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES ANNOUNCES 2016 HEALTH INSURANCE PREMIUM RATES, INCLUDING RATES FOR NY STATE OF HEALTH

Individual Rates for 2016 Remain Nearly 50% Lower than Before Establishment of New York’s Health Exchange

SUPERINTENDENT LAWSKY ANNOUNCES SETTING OF 2015 HEALTH INSURANCE RATES FOR NEW YORK, INCLUDING RATES FOR HEALTH BENEFITS EXCHANGE

Individual Rates for 2015 Will Continue to Be More than 50 Percent Lower on Average than Before Establishment of the Health Exchange

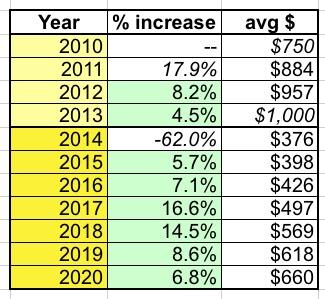

For six years straight, the New York DFS has claimed that even after the annual increases, average premiums for the upcoming year will be 50-55% lower than they were prior to the establishment of the New York State of Health exchange (aka, the state ACA exchange) starting in 2014. This sounds particularly curious given that premiums have obviously increased each of those years, by an average of 5.7% in 2015, 7.1% in 2016, 16.6% in 2017, 14.5% in 2018, 8.6% for 2019 and, as they just announced, 6.8% in 2020. That's a cumulative 75% average increase over six years.

So how could premiums in 2020 still be "less than 55%" of what they were prior to the ACA exchange launch (that is, as of 2013)?

Well, I decided to backtrack a bit further...and that's where things get a bit more complicated. Here's the press release announcing 2014 premiums...the first time all Individual and Small Group Market policies had to be fully ACA-compliant:

GOVERNOR CUOMO ANNOUNCES APPROVAL OF 2014 HEALTH INSURANCE PLAN RATES FOR NEW YORK HEALTH BENEFIT EXCHANGE

- 17 Health Insurers Have Rates Approved to Provide Coverage on the Exchange

NEW YORK, NY – Today, Governor Andrew M. Cuomo announced that the Department of Financial Services (DFS) has approved health insurance plan rates for 17 insurers seeking to offer coverage through New York’s Health Benefits Exchange, including eight new entrants into the market that do not currently offer commercial health insurance plans. Last year, Governor Cuomo took action to issue an Executive Order establishing the New York Health Benefit Exchange, which is expected to help more than one million uninsured New Yorkers access quality, affordable health care coverage.

As an aside: I had forgotten that the NY exchange was originally created via executive order by Cuomo, which means it could hypothetically be dissolved by a future GOP Governor. Fortunately, the state legislature resolved this earlier this year by codifying NYSoH into law anyway.

...On average, the approved 2014 rates for even the highest tier of plans individual New York consumers could purchase on the exchange (gold and platinum) represent a 53 percent reduction compared to last year’s direct-pay individual rates. The fact that these average individual rates are effectively being cut more than in half is primarily because a greater number of uninsured individuals are expected to obtain coverage in the individual insurance market – lowering overall premiums. 1 (Note: That 53 percent reduction does not include the impact of federal financial assistance for individuals meeting certain income thresholds who are purchasing coverage on the exchange, which would lower costs even further for many consumers.)

Furthermore, despite the fact that health care costs per capita are approximately 18 percent higher in New York than the national average, the average approved rates for the benchmark individual “silver plan” in New York would be in line with (nearly 10 percent lower) the nationwide average previously forecast by the independent, non-partisan Congressional Budget Office (CBO) for when health care reform is implemented.

The problem in trying to post "average rate hikes" for 2014 specifically is that pre-ACA individual market policies were quite different, even in New York where they already had Guaranteed Issue, Community Rating and a certain threshold of Essential Health Benefits mandated by state law. This was addressed in the footnote of the press release:

...1 It is challenging to compare existing premium rates to those that have been approved for 2014. The 2014 health insurance plans are for new products with new rates. However, plans in the existing “direct-pay” market where individual New York consumers who do not have insurance through their employer can purchase coverage have relatively uniform terms with high standards for the level and quality of coverage provided. These existing “direct-pay” plans are generally comparable to 2014 gold and platinum plans. For the lower-cost tiers of individual coverage (silver, bronze, and catastrophic), the approved 2014 rates would represent a even greater reduction than 53 percent compared to last year’s average direct pay rates – however, those plans are not directly comparable to existing offerings.

My reading of this is basically: Let's say the average 2013 Individual Market plan ("direct-pay" as they called it at the time) in New York cost $1,000/month, and the 2014 ACA-compliant Gold/Platinum plans averaged $470/month. That would be a 53% reduction. Of course, ACA Silver and Bronze plans cost considerably less than Gold or Platinum...and Bronze/Silver have always made up the vast bulk of ACA market policies chosen anyway. By 2016 only 7.8% of exchange enrollees selected Gold or Platinum plans combined (it's only gone down further since then, and some states don't even offer Platinum anymore).

To the best of my estimates, by back-filling the average premiums for the past six years using the annual percentage hikes above, it looks like they averaged around $376/month in 2014.

So how much were they in 2013? Unfortunately, I don't have that exact number from official records. All I have to go by is this article by Roni Caryn Robin and Reed Ableson in the New York Times from July 2013:

State insurance regulators say they have approved rates for 2014 that are at least 50 percent lower on average than those currently available in New York. Beginning in October, individuals in New York City who now pay $1,000 a month or more for coverage will be able to shop for health insurance for as little as $308 monthly. With federal subsidies, the cost will be even lower.

That "$1,000/month" figure doesn't say that it's the weighted average...and it's not even statewide, it's just for New York City specifically; more rural parts of the state likely paid even higher rates at the time. Still, it's better than nothing.

If I go back even further, I get average incrases of 8.2% for 2012 and 4.5% for 2013, but without knowing what the base dollar amount is that doesn't help much. I wasn't able to find the 2011 rate hike press release, but I did find this L.A. Times article by Noam Levey in 2010, which states:

Premiums in New York are now the highest in the nation by some measures, with individual health coverage costing about $9,000 a year on average. And nearly one in seven New Yorkers still lacks health coverage, a greater proportion than before the law was passed.

$9,000/year is $750/month.

Assuming that's accurate, here's the New York individual market rate hikes from 2010 - 2020 as far as I can figure:

Assuming I have everything correct here, it looks like 2020 premiums will "only" be 33% lower than they were in 2013...but again, the PR specifies after adjusting for inflation. Inflation since 2013 is around 10.1%, so that $1,000 would be around $1,101 today. This puts 2020 rates at 40% lower than pre-ACA rates.

All in all, NY DFS's "55% lower" may seem like an exaggeration, but again, that $1,000 figure for 2013 is very vague. Higher upstate premiums in 2013 could have made the actual average higher, although it'd have to be $1,500/month in order for the "55% lower w/inflation" claim to be undeniably accurate.

The bigger question I have is why they didn't just say "at least 40% lower" for 2020...and why they've been obsessed with this "55%" figure for so many years even when rates were clearly at least 60% lower than pre-ACA prices several years ago.

UPDATE 8/20/20: Annnnd they're still doing it:

Individual Market

Rates for individuals are more than 55% lower than prior to the establishment of the New York State of Health in 2014, adjusting for inflation but not counting federal financial assistance that the ACA makes available to many consumers purchasing insurance. Approximately 323,000 New Yorkers are currently enrolled in individual commercial plans.

Advertisement