New Mexico exchange considering offloading two ACA albatrosses

Wed, 02/15/2023 - 3:32pm

New Mexico's state-based ACA exchange, BeWell NM, has posted a powerpoint from a special Board of Director's meeting that they had last week.

For the most part it's unremarkable and full of inside baseball wonkery:

- They're replacing WebEx with Zoom for video meetings

- They're gonna split their Comms & Outreach into two separate divisions

- They're preparing for the upcoming Medicaid Unwinding project

There's two items which are more noteworthy, however.

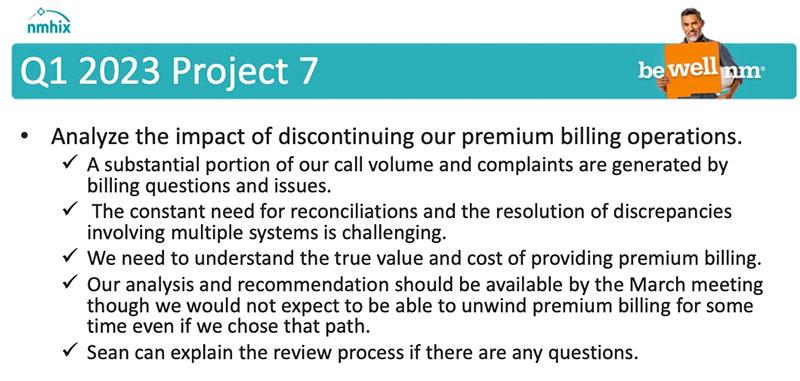

First, New Mexico is one of only three state-based marketplace (SBM) which handle premium bill payments as well as enrollment functions. The other two are Rhode Island and Massachusetts. Washington State's HealthPlanFinder tried dealing with payments within the exchange itself as well for a few years but eventually gave up on it due to it causing too many technical & administrative headaches.

To the best of my knowledge, BeWell NM is the only other state exchange which has attempted to incorporate payments into its system. I believe HealthCare.Gov was originally supposed to be set up to handle premium payments as well, but the payment button was greyed out for the first couple of years, and as of today, if you click the "Pay your first premium" button it will just take you directly to your insurance carrier's website instead.

Well, according to the NM Hix BoD slide deck, it looks like they may be following Washington State's lead by deciding billing is more trouble than it's worth as well:

Interestingly, this discussion is happening at the same time that exchange vendors are pushing for future SBMs to include billing functionality when they go live:

There may be a “tech refresh,” says Miller, who says he’s excited to see what other capabilities states may be exploring. Miller has been pushing for states to handle consumer billing, which Softheon can support. Some states did try to manage billing in the past, but found it to be difficult, he points out.

I have mixed feelings about integrated billing. On the one hand, it no doubt is more convenient for the enrollees (assuming it works properly), has a lower administrative burden, and likely leads to a higher retention rate with fewer enrollees falling between the cracks.

On the other hand...well, there's the various bullet points listed in the slide above, plus there's already enough confusion by the public about the distinction between the ACA exchanges and the actual insurance policies they're enrolling in. Many people don't seem to understand that the exchange is simply the platform through which they enroll in the program and qualify for financial help; private insurance carriers are still the ones responsible for their coverage.

In any event, there's another item which I also found interesting:

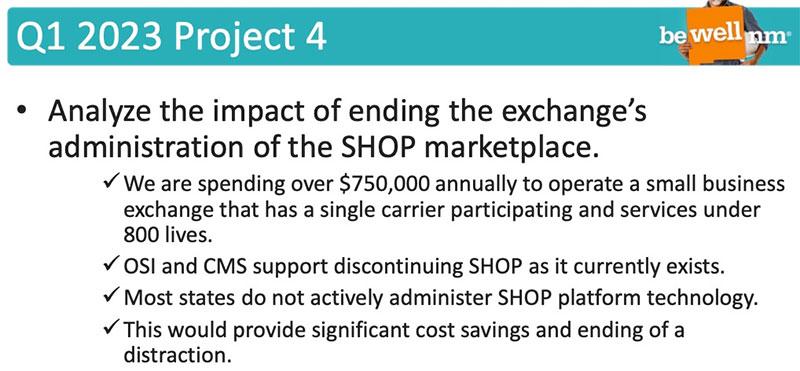

I haven't written about the ACA's Small Business Health Options Plan (SHOP, although it should really be SBHOP which is kind of awkward) in quite some time...with good reason.

The SHOP provision was supposed to be sort of like the small group market version of the ACA's individual market exchanges: Small employers could enroll their employees & dependents in a small group plan using the SHOP exchanges and receive financial assistance in the form of tax credits if their business qualified.

However...the SHOP program never really took off outside of a handful of states. In fact, to my knowledge the Centers for Medicare & Medicaid Services have never given SHOP enrollment data so much as a footnote mention in any of their enrollment reports over the past nine years. The closest thing to an official data point mentioned at the federal level was way back in 2015, when then-HealthCare.Gov head Kevin Counihan mentioned that around 85,000 people were enrolled in SHOP plans nationally.

Of course, that was eight years ago; enrollment is certainly higher today than it was then. Covered California, for instance, recently reported having over 78,000 SHOP enrollees themselves. The DC Health Link exchange reports around 87,000 SHOP enrollees there (this is disproportionately high for DC's tiny population for two reasons: First, DC requires all small group enrollment to be handled on exchange; second, because an "eat your own dog food" provision of the ACA requires members of Congress and their staff to enroll in coverage via the DC SHOP exchange if they want to receive their Federal Employee Health Benefit discount. I know New Hampshire had around 8,000 people enrolled in their SHOP plans in 2021, and so on.

According to Louise Norris, as of 2021, there were 11 states which still offered SHOP enrollment...and even then, only six of them actually handle SHOP enrollment through their exchanges (CA, CT, DC, MA, NM & RI). The rest either always offloaded SHOP enrollment directly to the insurance carriers/brokers or recently started doing so. As far as I can figure, there's probably no more than 300,000 or so people enrolled in SHOP plans nationally.

Anyway, it looks like New Mexico only has around 800 residents enrolled in their SHOP exchange statewide...while spending three quarters of a million dollars to administer their program. That breaks out to over $900 apiece, which is admittedly absurdly inefficient, so unless New Mexico plans on dramatically ramping up SHOP enrollment quickly, I'd say it would make sense for them to follow in the footsteps of Colorado, New York and other states and drop administration of it entirely.

Advertisement