Prepare Thyself: ACA 2.0 is happening. (Part 2 of 3)

Wed, 03/17/2021 - 2:27pm

On Monday I noted that in the wake of the passage and signing of HR 1319 (the American Rescue Plan, or ARP), which includes a dramatic (if time-limited) upgrade & expansion of ACA individual market subsidies, Senate Democrats are hard at work pushing for several other important bills to make President Biden's larger healthcare policy vision a reality on a permanent basis.

The three bills I discussed in Part 1 are:

- Sen. Mark Warner's Health Care Improvement Act of 2021 (S.352)

- Sen. Michael Bennet & Sen. Tim Kaine's re-introduced "Medicare X" Act (S.386, I believe)

- Sen. Jeanne Shaheen's Improving Health Care Affordability Act (S.499)

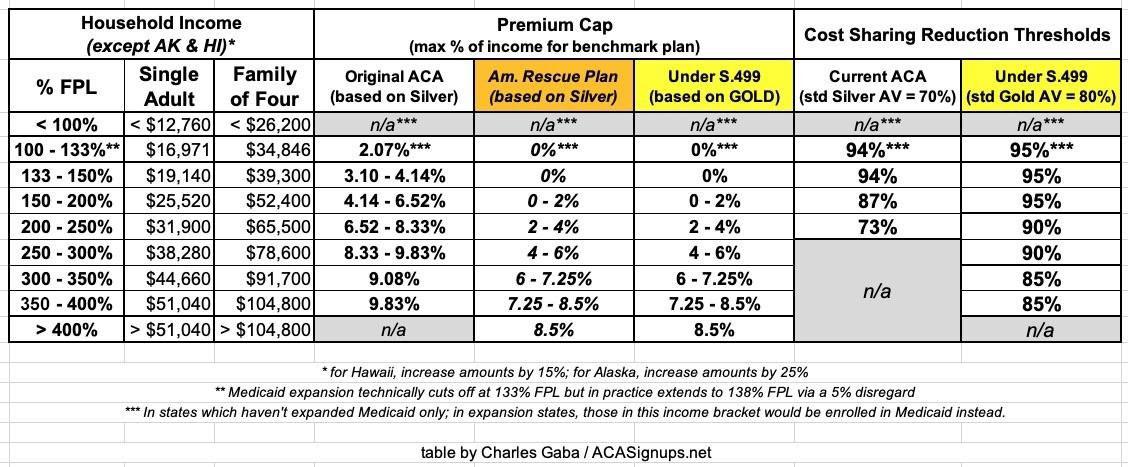

Of the three, the one which seems most likely to actually have a shot at passing both the House and Senate and being signed into law by President Biden during the 2021 - 2022 legislative session is Sen. Shaheen's S.499, which would:

- Permanently codify the 8.5% maximum cap on ACA benchmark Silver plan premiums;

- Permanently codify the beefed-up subsidy formula below the 8.5% threshold;

- Upgrade the ACA individual market benchmark plan from Silver to Gold;

- Expand the ACA's CSR subsidy structure from the current 250% FPL threshold to 400% FPL;

- Upgrade the CSR formula so that all enrollees earning less than 400% FPL would qualify for a Platinum or Gold Plus plan; and...

- Pay for a large chunk of the above by formally appropriating CSR reimbursement funds.

The first two bullets above are also included in Rep. Lauren Underwood's H.R. 369. As I noted in Part 1, the last item would eliminate Silver Loading, which would actually save several hundred billion dollars over the next decade...thus freeing the money up to fund the upgrades.

Here's the table I put together which summarizes the original ACA formulas for premium & cost sharing subsidies; the temporary premium subsidy formula under the ARP; and what both tables would look like under S.499:

If S.499 were to become law, it would check off two major provisions of Pres. Biden's larger proposal.

However...there's a bunch of other stuff on the ACA 2.0 checklist as well, and the House Democrats are also hard at work on them. Behold, the House Energy & Commerce Committee's hearing scheduled for next Tuesday, March 23rd:

HEARING ON "BUILDING ON THE ACA: LEGISLATION TO EXPAND HEALTH COVERAGE AND LOWER COSTS"

Date: Tuesday, March 23, 2021 - 11:00am

Location: Virtual Hearing via Cisco WebEx

Subcommittees: Health (117th Congress)

The Subcommittee on Health of the Committee on Energy and Commerce will hold a legislative hearing on Tuesday, March 23, 2021, at 11 a.m. via Cisco Webex. The hearing is entitled, "Building on the ACA: Legislation to Expand Health Coverage and Lower Costs."

- H.R. 1790, the "Fair Indexing for Health Care Affordability Act"

- H.R. 1796, the "Health Care Enrollment Innovation Act"

- H.R. 1872, the "Marketing and Outreach Restoration to Empower Health Education Act of 2021" or the "MORE Health Education Act"

- H.R. 1874, the "Expand Navigators' Resources for Outreach, Learning, and Longevity Act of 2021" or the "ENROLL Act of 2021"

- H.R. 1875, To amend title XXVII of the Public Health Service Act to eliminate the short-term limited duration insurance exemption with respect to individual health insurance coverage

- H.R. 1878, the "State Health Care Premium Reduction Act of 2021"

- H.R. 1890, the "Health Care Consumer Protection Act"

- H.R. 1896, the "State Allowance for Variety of Exchanges Act of 2021" or the "SAVE Act of 2021"

- H.R. 340, the "Incentivizing Medicaid Expansion Act of 2021"

- H.R. 1738, the "Stabilize Medicaid and CHIP Coverage Act"

- H.R. 1784, the "Medicaid Report on Expansion of Access to Coverage for Health Care Act" or the "Medicaid REACH Act"

- H.R. 1025, the "Kids' Access to Primary Care Act of 2021"

- H.R. 66, the "Comprehensive Access to Robust Insurance Now Guaranteed for Kids Act" or the "CARING for Kids Act"

- H.R. 1791, the "Children's Health Insurance Program Permanency (CHIPP) Act"

- H.R. 1888, the "Improving Access to Indian Health Services Act"

- H.R. 1717, To To amend title XIX of the Social Security Act to make permanent the protections under Medicaid for recipients of home and community-based services against spousal impoverishment.

- H.R.1880 - To amend the Deficit Reduction Act of 2005 to make permanent the Money Follows the Person Rebalancing Demonstration.

- H.R. 1390, the "Children's Health Insurance Program Pandemic Enhancement and Relief Act" or the "CHIPPER Act"

That's right...they'll be having a marathon hearing to discuss not just one or two bills, but eighteen of them. Two years ago, the House passed a similar, but smaller bundle of seven standalone bills as a package; this strikes me as being pretty much the same thing, with three important differences: First, there's more than twice as many mini-bills included; second, the ARP has already passed, which could help grease the skids. And third, the Dems now hold a trifecta in the House, Senate (just barely) and White House.

Some of 18 bills above are more significant than others, and some of them don't even have a formal title yet. There's no guarantee that all of them will make it out of committee or through the full House, of course, and if/when they make it to the Senate side, there's obviously the filibuster situation to contend with...but it's a start. Let's take a look!

- H.R. 1790, the "Fair Indexing for Health Care Affordability Act"

Two years ago, Trump CMS Administrator Seema Verma tweaked one of the more obscure formulas used for determining how much ACA enrollees receive in advance premium tax credits (APTC) each year at different income levels. The Premium Adjustment Percentage Index (PAPI) is a wonky adjustment figure which is the reason why people earning 300-400% FPL have to pay 9.83% of their income instead of the 9.5% laid out in the ACA itself. It's sort of like a "chained CPI" thing except instead of being attached to the Consumer Price Index, it's tied to the relative change in average full-price health insurance premiums compared to 2013. In addition to tax credits, PAPI is also used to adjust the Maximum Out of Pocket (MOOP) amount which ACA enrollees could have to pay for in-network care.

Until last year, PAPI was based purely on the relative change in employer-sponsored insurance premiums. Verma modified it to include the change in individual market premiums as well, and since indy market premiums have increased dramatically more since 2013 than employer premiums, that means a higher adjustment. As a result, APTC subsidies are a bit less generous and the MOOP ceiling is hundreds of dollars higher than it otherwise would be.

H.R. 1790 would require CMS to revert back to the pre-Verma formula, codifying the employer-sponsored PAPI formula instead. Personally, I wish they'd just get rid of it altogether; it's irritating to have to update the APTC tables every year by hundredths of a percentage point.

- H.R. 1796, the "Health Care Enrollment Innovation Act"

This bill would "direct the Secretary of Health and Human Services to award grants to eligible State agencies to promote State innovations to expand health insurance coverage." In short, it would provide $200 million/year for 3 years in state grants to establish the following types of programs:

- Streamline health insurance enrollment procedures...including automatic enrollment and reenrollment of, or pre-populated applications for, individuals without health insurance who are eligible for tax credits...with the ability to opt out of such enrollment.

- Technology to improve data sharing and collection

- Implementation of a State version of an individual mandate

- Feasibility studies (for) comprehensive and coherent State plan for increasing enrollment

The first seems to be along the lines of Maryland's "EZ Enrollment" law, which lets people opt to be enrolled in either Medicaid or a subsidized ACA plan when they file their state taxes. The second bullet would obviously be cheered by a data hound like myself. The third one is eyebrow-raising, as it amounts to openly admitting that the federal individual mandate penalty is not coming back, period (there are four states, plus DC, which have their own mandate penalty as of today: CA, DC, MA, NJ & RI). The last bullet seems pretty vague & open-ended.

- H.R. 1872, the "Marketing and Outreach Restoration to Empower Health Education Act of 2021" or the "MORE Health Education Act"

Like HR 1790, this is another case of repairing damage caused by the Trump Administration. As you may recall, starting in 2017 they gutted the marketing and outreach budget for HealthCare.Gov, eventually paring it down to just 10% of the annual budget under the Obama Administration. Even worse, they then turned around and used some of the money which was supposed to go to promoting ACA Open Enrollment and used it to produce anti-ACA propaganda videos. On top of that, they also expended taxpayer resources and funding to promote non-ACA compliant policies such as short-term and other "junk" plans.

HR 1872 would codify $100 million per year in federal funds to be used specifically to promote, advertise and encourage enrollment in ACA-compliant plans only. It would also require that marketing to be appropriately tailored to different ethnic groups, non-English speakers and so forth. It specifically prohibits using the money to promote junk plans.

The bill would also require the HHS Secretary to establish annual enrollment targets and to provide "biweekly" enrollment reports including various details (this one is interesting because a) even the Trump Administration was pretty good about doing this and b) "biweekly" could mean either every two weeks or twice every week depending on who you ask...)

It also codifies post-Open Enrollment reporting, not just on actual enrollments (which, again, the Trump Admin did do) but also on ACA navigator activities, targets, goals and so forth, as well as marketing, outreach and other demographics and metrics. Finally, it would require an annual report on how CMS spent every dime collected in ACA exchange User Fees...namely, the 2-3% of premiums which go to actually fund the operations of HC.gov.

- H.R. 1874, the "Expand Navigators' Resources for Outreach, Learning, and Longevity Act of 2021" or the "ENROLL Act of 2021"

In addition to gutting & misusing the marketing budget of HealthCare.Gov, the Trump Admin also gutted/misused funds for the Navigator program. HR 1874 would codify $100 million per year to be used exclusively for the ACA Navigator/Counselor program. It would also prevent Navigator grants from prioritizing groups which promote junk plans; requires at least one nonprofit group be included; and requires that the grantees actually have roots in the local community they're serving.

- H.R. 1875, To amend title XXVII of the Public Health Service Act to eliminate the short-term limited duration insurance exemption with respect to individual health insurance coverage

Yes, I believe you're reading that correctly: While it technically allows them to continue to be offered, this bill appears to be designed to effectively eliminate #ShortAssPlans altogether starting in 2023. The full text of the bill is literally one sentence:

Section 2791(b)(5) of the Public Health Service Act (42 U.S.C. 300gg–91(b)(5)) is amended by inserting ‘‘(other than such insurance that is issued, sold, or renewed on or after January 1, 2023)’’ before the period at the end.

Seems innocuous enough, right? Well, let's take a look at Section 2791(b)(5) of the Public Health Service Act, shall we?

(5) Individual health insurance coverage

The term “individual health insurance coverage” means health insurance coverage offered to individuals in the individual market, but does not include short-term limited duration insurance.

By definiing Short-Term, Limited Duration (STLDs) as actual individual health insurance coverage, this bill means that STLDs would be regulated as individual health insurance coverage under the Affordable Care Act. I could be wrong, but I think that means STLDs would have to comply with most if not all of the other ACA individual market regulations...such as guaranteed issue, community rating, essential health benefits, removing annual/lifetime coverage limits and so forth. If so, that would pretty much eliminate the only reason for STLDs to exist in the first place (i.e., offering dirt-cheap premiums for crap coverage).

Some states like California have banned STLDs outright. Others, like Colorado, have simply started requiring STLDs to comply with various ACA requirements. This bill takes the Colorado tact to its logical conclusion...and as long as HR 369 or S.499 are signed into law as well, I'm perfectly fine with kicking #ShortAssPlans to the curb permanently.

- H.R. 1878, the "State Health Care Premium Reduction Act of 2021"

Danger, Will Robinson! This bill would basically provide a whopping $10 billion per year to be used by applying states in one of two types of ways:

‘‘(1) To provide reinsurance payments to health insurance issuers with respect to individuals enrolled under individual health insurance coverage (other than through a plan described in subsection (b)) offered by such issuers.

‘‘(2) To provide assistance (other than through payments described in paragraph (1)) to reduce out of-pocket costs, such as copayments, coinsurance, premiums, and deductibles, of individuals enrolled under qualified health plans offered on the individual market through an Exchange and of individuals enrolled under standard health plans offered through a basic health program established under section 1331.

Hoo, boy. Dave Anderson is gonna be thrilled with this one (that's sarcasm). As Dave notes (and as I'll explain in a subsequent blog post), while reinsurance programs can be useful in certain circumstances and have been useful in a pre-American Rescue Plan world, "In the universe as it will be next week, state reinsurance waivers in 2022 don’t make a ton of sense."

On the other hand, if this money is used for the second category of purposes, that could be very helpful indeed. The ARP subsidy improvements, if made permanent via HR 369 or S.499, would pretty much take care of the premium side of things and much of the deductible/co-payment side of things. The shout-out to the ACA's Basic Health Programs (currently operating in Minnesota and New York only) is interesting.

The bill clarifies that the money is not to be used for enrollees in Grandfathered or Transitional plans, that the states have to apply with a description of how the money would be used, that the requests will be automatically approved if not actively denied by the CMS Administrator within 60 days, that the program will be approved for 5 years, and there's also some safeguard regulations allowing the program to be revoked under certain conditions.

- H.R. 1890, the "Health Care Consumer Protection Act"

The first half of this one is new to me, and could either put the kibosh on one of the other big complaints people have about ACA plans (narrow networks) or it could be a mess, depending on how it's implemented:

To amend the Patient Protection and Affordable Care Act to require Exchanges to establish network adequacy standards for qualified health plans and amend the Public Health Service Act to provide protections for consumers against excessive, unjustified, or unfairly discriminatory increases in premium rates.

SEC. 102. REQUIRING EXCHANGES TO ESTABLISH NETWORK ADEQUACY STANDARDS FOR QUALIFIED HEALTH PLANS.

(a) IN GENERAL.—Section 1311(d) of the Patient Protection and Affordable Care Act (42 U.S.C. 18031(d)) is amended by adding at the end the following new paragraph:

‘‘(8) NETWORK ADEQUACY STANDARDS.—

‘‘(A) CERTAIN EXCHANGES.—In the case of an Exchange operated by the Secretary pursuant section 1321(c)(1) or an Exchange described in section 155.200(f) of title 42, Code of Federal Regulations (or a successor regulation), the Exchange shall require each qualified health plan offered through such Exchange to meet such quantitative network adequacy standards as the Secretary may prescribe for purposes of this subparagraph.

‘(B) STATE EXCHANGES.—In the case of an Exchange not described in subparagraph (A), the Exchange shall establish quantitative network adequacy standards with respect to qualified health plans offered through such Exchange and require such plans to meet such standards.’’.

(b) EFFECTIVE DATE.—The amendment made by this section shall apply with respect to plan years beginning on or after January 1, 2023.

Notice that it doesn't actually define what those Network Adequacy Standards are...that would be left up to HHS Secretary Becerra (he's set to be confirmed tomorrow).

The second part relates to annual premium rate review, which is already regulated to some degree by the ACA:

‘‘(e) PROTECTION FROM EXCESSIVE, UNJUSTIFIED, OR UNFAIRLY DISCRIMINATORY RATES.—

‘‘(1) AUTHORITY OF STATES.—Nothing in this section shall be construed to prohibit a State from imposing requirements (including requirements relating to rate review standards and procedures and information reporting) on health insurance issuers with respect to rates that are in addition to the requirements of this section and are more protective of consumers than such requirements.

‘‘(2) CONSULTATION IN RATE REVIEW PROCESS.—In carrying out this section, the Secretary shall consult with the National Association of Insurance Commissioners and consumer groups.

‘‘(3) DETERMINATION OF WHO CONDUCTS REIEWS FOR EACH STATE.—The Secretary shall determine, after the date of enactment of this section and periodically thereafter, the following:

‘‘(A) In which markets in each State the State insurance commissioner or relevant State regulator shall undertake the corrective actions under paragraph (4), based on the Secretary’s determination that the State regulator is adequately undertaking and utilizing such actions in that market.

‘(B) In which markets in each State the Secretary shall undertake the corrective actions under paragraph (4), in cooperation with the relevant State insurance commissioner or State regulator, based on the Secretary’s determination that the State is not adequately undertaking and utilizing such actions in that market.

‘(4) CORRECTIVE ACTION FOR EXCESSIVE, UNJUSTIFIED, OR UNFAIRLY DISCRIMINATORY RATES.—In accordance with the process established under this section, the Secretary or the relevant State insurance commissioner or State regulator shall take corrective actions to ensure that any excessive, unjustified, or unfairly discriminatory rates are corrected prior to implementation, or as soon as possible thereafter, through mechanisms such as—

‘‘(A) denying rates;

‘‘(B) modifying rates; or

‘‘(C) requiring rebates to consumers.‘‘(5) NONCOMPLIANCE.—Failure to comply with any corrective action taken by the Secretary under this subsection may result in the application of civil monetary penalties under section 2723 and, if the Secretary determines appropriate, make the plan involved ineligible for classification as a qualified health plan.’’.

In other words: If the HHS Secretary decides a state insurance commissioner is doing a good job regulating insurance premium rates, they'll leave them alone, but if they think the insurance commissioner is doing a crappy job, the HHS Secretary has the right to step in and take action instead. I'm guessing some states will cry "States Rights!" and sue over this one; this is one area where having the California Attorney General as HHS Secretary could be useful.

- H.R. 1896, the "State Allowance for Variety of Exchanges Act of 2021" or the "SAVE Act of 2021"

When the ACA was first signed into law in 2010, it included a buttload of money (that's a technical term) in grant money to help individual states establish their own ACA exchange platforms. Only around 20 states actually took the feds up on it (and of those, several never got around to completing the process). The rest stuck with the federal exchange, HealthCare.Gov.

Of the states which did create their own ACA exchange, about half of them had serious technical problems out of the gate; in fact, five states (MD, MA, NV, OR & HI) were such a money pit of suckage that they ended up scrapping their exchanges entirely after the first year or two. Maryland, Massachusetts and Nevada have since created brand-new ACA exchanges (with their own money, I believe) which are working just fine, while Kentucky's prior Republican Governor, Matt Bevin, shut down their beloved "kynect" exchange for no reason whatsoever. In the meantime, that original grant money has long since dried up.

Since then, however, things have changed dramatically. Nevada, Pennsylvania and New Jersey have all split off from HC.gov with minimal drama. Kentucky's new Democratic Governor is dusting kynect off again this year, and both New Mexico and Virginia are set to launch their own state-based exchanges in the fall as well. State-based ACA exchanges have gone from being a hindrance to hotness, just as I predicted would happen 5 1/2 years ago.

Well, HR 1878 would provide $200 million in grants over for more states to set up their own ACA exchange over a 2-year period. They'd have up to the end of 2024 to apply, and would have to be fully self-funded by January 1st, 2026. That's...pretty much it. It doesn't really lay out how much each state could request, although it's my understanding that after flushing hundreds of millions of dollars down the drain back in 2010 - 2013, a state can whip up a state-based ACA exchange "out of the box" for like $30 million these days.

- H.R. 340, the "Incentivizing Medicaid Expansion Act of 2021"

A couple of weeks ago I noted that the ARP basically attempts to flat-out bribe the twelve states which are still refusing to expand Medicaid under the ACA by bumping up the share of all Medicaid costs paid for by the federal government by a full five points if they finally do so. Since non-ACA Medicaid enrollment is much higher then ACA expansion enrollment (and mostly consists of more expensive enrollees), this means the ARP payoff would be considerably more than the states would have to pay to expand the program (remember, they have to cover 10% of the cost to expand).

Well, HR 340 would sweeten the pot even more: It would cover that remaining 10% expansion cost for the first 3 years, and from 1-10% of the cost for the next few years, meaning these states wouldn't have to start paying a dime until at least 2025 and wouldn't have to start covering the full 10% until around 2029, I believe.

If this bill were to pass on top of the ARP, that'd mean up to another $6.8 billion windfall for these dozen states...just for doing what they should've done seven years ago in the first place.

NOTE: This post is getting kind of long so I'm breaking the other nine bills into a separate Part 3 post...stay tuned...

Advertisement