CMS releases avg. effectuation report for H1 2019: 10.2 million, down 100K from 2018

Wed, 12/11/2019 - 3:36pm

Effectuated Enrollment for the First Half of 2019

This report provides average monthly effectuated enrollment and premium data for the individual market Federal and State-Based Exchanges for the first six months of the 2019 plan year. The Centers for Medicare & Medicaid Services (CMS) publishes effectuated enrollment data semiannually to provide a more accurate picture of enrollment trends for the Exchanges than indicated by the number of individuals who simply selected a plan during Open Enrollment. For coverage to be considered effectuated, individuals generally must pay the first month’s premium for the plan.

As of September 15, 2019, an average of 10.2 million individuals had effectuated their coverage through June 2019. The average effectuated enrollment for the first six months of 2019 was approximately 85,000 individuals lower compared to the same time period in 2018, which represents a 0.8 percent decrease.

Similar to past years, the number of individuals who effectuated coverage is lower than the number with plan selections at the end of Open Enrollment. The average number of individuals with effectuated coverage for the first half of 2019 was about 1.25 million lower than the number of individuals with plan selections at the end of the 2019 Open Enrollment Period. This reflects a higher rate of enrollment effectuations from plan selections than last year. Effectuated enrollments for the first half of 2018 were about 1.5 million lower than the number of plan selections at the end of the 2018 Open Enrollment Period (as of September 15, 2018). That is, effectuated enrollments as a percent of plan selections were 89% for 2019, up from 87% for the prior 2019 benefit year.

- 2018: 11.75 million QHP selections during Open Enrollment; 10.3 million avg. monthly effectuations for first six months of the year

- 2019: 11.44 million QHP selections during Open Enrollment; 10.2 million avg. monthly effecutations for first six months of the year

In other words, 310,000 fewer people selected policies, but only 225,000 fewer dropped their coverage during the year, which is a higher retention rate. Whether you see this as good or bad news depends on your persepctive, I suppose...

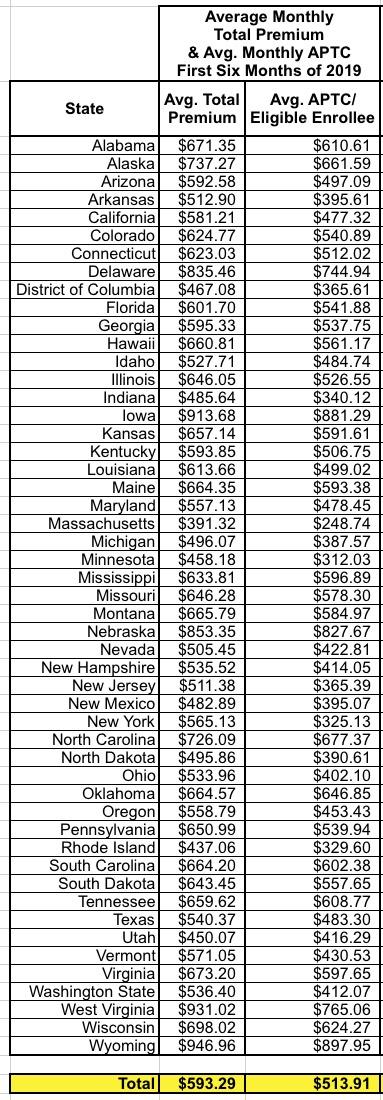

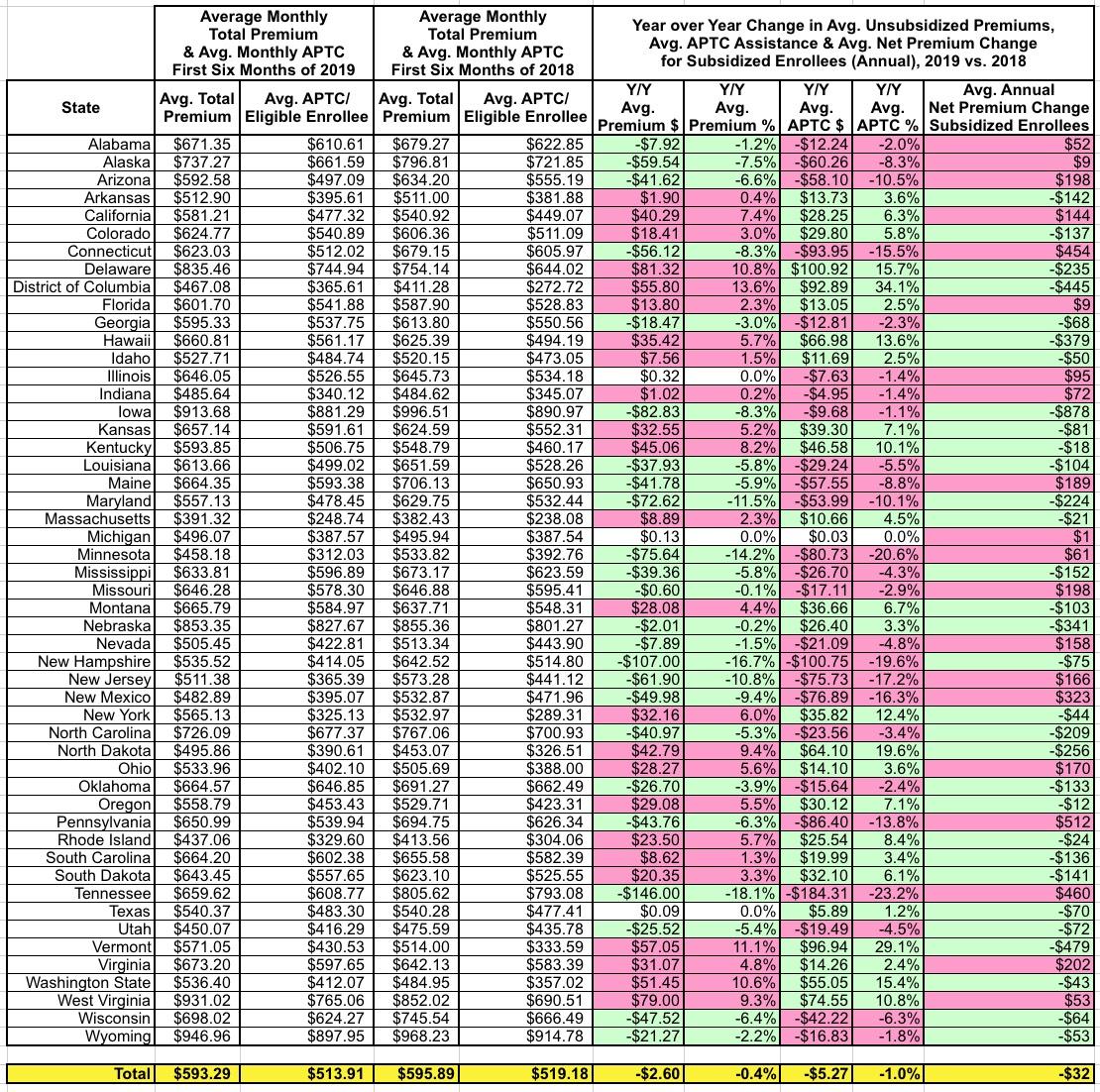

The data released today also show that the average monthly premium per enrollee for the first six months of 2019 was $593.29, a decrease of 0.4 percent compared to the first six months of 2018, while the average monthly amount of advance payments of the premium tax credits (APTC) per eligible enrollee decreased 1.0% to $513.91 when compared with the first six months of 2018 average APTC per eligible enrollee. The average premium and average APTC amounts have been relatively stable since the start of the 2019 plan year, as indicated in the Early 2019 Effectuated Enrollment Snapshot. The proportion of total enrollees who received APTC in the first six months of 2019 slightly increased to 87.0 percent, up from 86.5 percent in the first half of 2018.

So average premiums dropped $2.60/month...but APTC assistance dropped $5.27/month for those receiving it.

Put another way, unsubsidized enrollees are paying $31 less for the year in 2019 , but subsidized enrollees are actually paying $32 more for the year in 2019.

Not a huge price drop or increase either way, but those few extra bucks per month mean a lot more to the subsidized enrollees than the few bucks saved per month do to the full-price crowd...

Background Information

The primary source for the first half of 2019 average effectuated enrollment is payment and enrollment data. Effectuated enrollment is the average number of individuals who had an active policy at any point from January through June of 2019, and who paid their premium (thus effectuating their coverage) as of September 15, 2019. This report includes effectuated enrollment for both State-Based Exchanges and States using the HealthCare.gov platform.

APTC enrollment is the total number of individuals who had an active policy at any point from January through June 2019, who paid their premium, if applicable, and received APTC. APTC is generally available if an individual's estimated household income is between 100 and 400 percent of the federal poverty level, and certain other criteria are met. An individual was defined as receiving APTC if the applied APTC amount was greater than $0; otherwise, an individual was classified as not receiving APTC.

CSR enrollment is the total number of individuals who had an active policy at any point from January through June 2019, who paid their premium, if applicable, and received cost-sharing reductions (CSR). A consumer is generally eligible for CSR if the individual is eligible for APTC, has an estimated household income between 100 percent and 250 percent of the federal poverty level, and is enrolled in a health plan from the silver plan category. American Indians and Alaskan Natives are eligible for CSRs under different criteria.

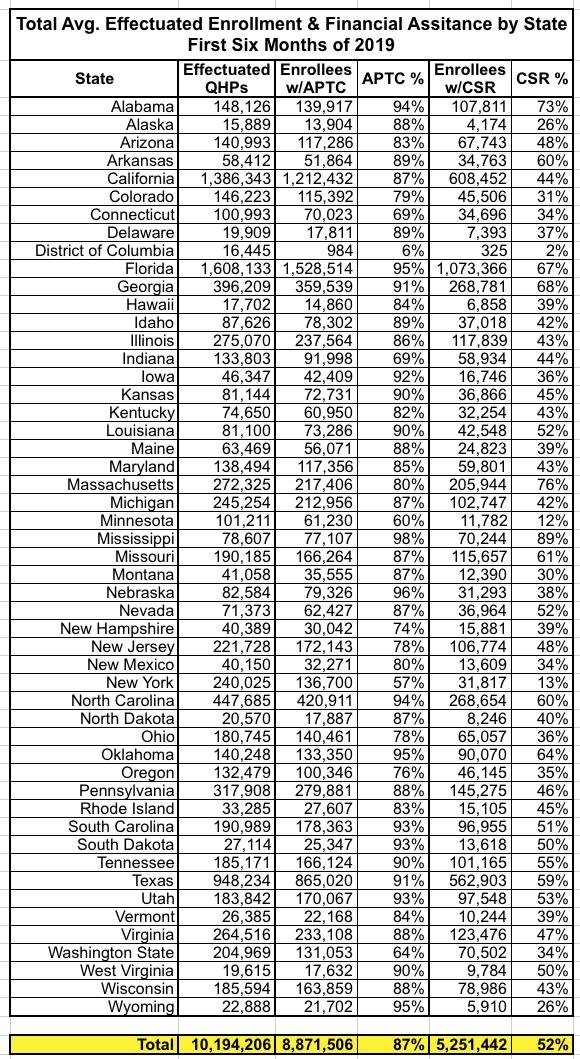

Here's the state-by-state breakout for the first six months of 2019:

As usual, the District of Columbia has barely any enrollees receiving either APTC or CSR since DC residents earning up to 210% FPL anyway. This leaves almost no enrollees earning 210 - 250% FPL (and some of them probably choose Bronze plans anyway). The CSR percent is also very low in Minnesota and New York; in those cases it's because they both have Basic Health Plan programs in place which cover residents earning 138% - 200% FPL

One other noteworthy tidbit underscoring the divide between HC.gov states and state-based exchanges: If you count Nevada as a SBM both years, H1 2019 effectuated enrollment is 110,000 lower than H1 2018 effectuated enrollment...but H1 2019 effectuated enrollment is 25,000 higher in the state-based exchanges. They partially cancel out the HC.gov states, giving the -85,000 net change nationally.

For what I believe is the sixth year running, Massachusetts again has the lowest avg. unsubsidized premiums in the country, while Wyoming has the dubious honor of having retaken the crown for highest average premiums from Iowa.

As noted above, however, due to the weird dynamics of Silver Loading and other plan pricing oddities, however, there's a somewhat inverse relationship between unsubsidized premiums and subsidized premiums. For instance, in Hawaii, premiums went up 5.7% ($35/month)...but APTC assistance went up 13.6% ($67/month), so the average net premium actually dropped by around $32/month or $379 for the year.

Conversely, in Tennessee, average premiums dropped by a whopping 18.1% ($146/month)...but this actually led to net premiums going up around $460 for the year for subsidized enrollees.

This isn't an exact correlation, of course, because there's no way of knowing which specific enrollee at which specific income level chose which specific plan, but it's pretty good as a guideline:

Advertisement