District of Columbia: *Final* unsubsidized 2020 #ACA premiums: 8.7% higher (down from +11.2%)

Sat, 09/21/2019 - 11:38am

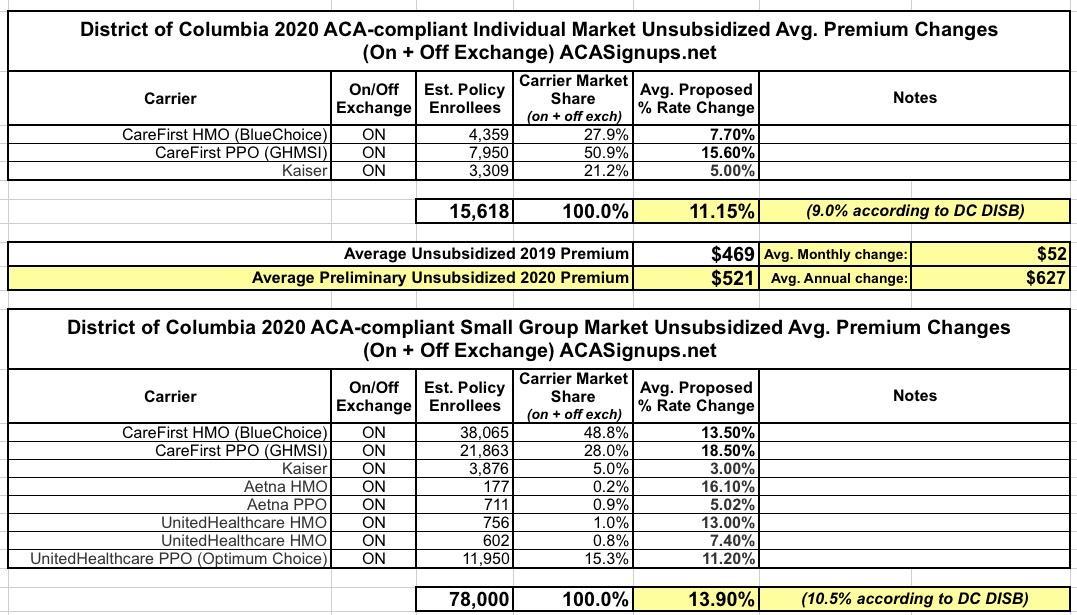

Back in mid-June, the DC Health Benefit Exchange Authority posted the preliminary, requested average unsubsidized 2020 premium changes for the Individual and Small Group markets:

Overall individual rates increased an average of 9.0 percent and small group rates increased an average of 10.5 percent. In the individual market, CareFirst proposed an average increase of 7.7 percent for HMO plans, and 15.6 percent for PPO plans. Kaiser proposed an average increase of 5.0 percent. For small group plans, CareFirst filed average rate increases of 13.5 percent for HMO plans and 18.5 percent for the PPO plans. Kaiser small group rates proposed an average increase of 3.0 percent. Aetna filed for an average increase of 16.1 percent for HMO plans and 5.0 percent for PPO plans. Finally, United proposed an average increase of 13.0 percent and 7.4 percent for its two HMOs and 11.2 percent for its PPO plans.

This is what it looked like at the time:

While the press release put the weighted average increase at 9.0% on the individual market and 10.5% for the small group market, when I ran my own weighted averages they came in at 11.2% and 13.9% respectively.

I didn't think much of it at the time since there are sometimes minor methodology factors I'm not aware of, and these were just preliminary requests anyway.

Then, in August, there were public hearings and a presentation about the rate review by DC regulators, and while they were a bit confusing, in the end it looked like the average rate changes would be modified to increases of 8.8% on the individual market and 14.7% on the small group market.

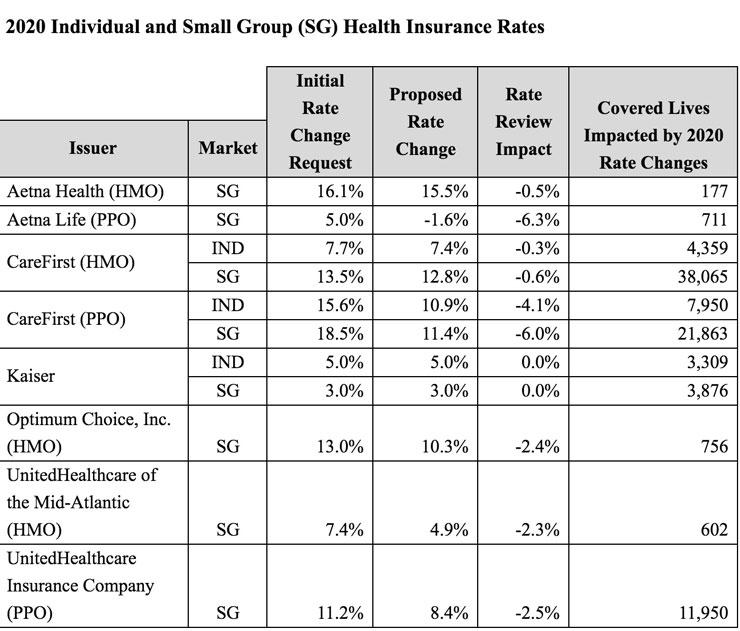

Today, however, the final, approved rate changes were publicly posted, and while both markets saw lower rate increases than originally requested, there's still a very strange discrepancy between my numbers and the DC Dept. of Insurance, Securities & Banking:

Press Release: District Announces 2020 Health Insurance Rates

Today, the District of Columbia Department of Insurance, Securities and Banking (DISB) announced the approved individual and small business health insurance rates for 2020. After the Department’s review, most insurers decreased their initial rate proposals, which will save District residents more than $18 million.

Based on the Department’s review and public feedback, three out of four insurers reduced their rates from their initial filings. The decreases from the initial filed rates were as much as 6.3 percent; overall, rates will increase by 7.6 percent for individual coverage and 8.4 percent for small group coverage. Aetna, CareFirst BlueCross BlueShield, Kaiser Permanente and UnitedHealthcare, the same insurance companies that offered plans in 2019, will have plans available on DC Health Link.

“We are committed to providing consumer protection and effective regulatory oversight of health insurance offerings for the residents and employers in the District,” said Department Commissioner Stephen Taylor. “This includes fair rates and non-discriminatory coverage. We performed a thorough review of 156 small group plans and 25 individual plans to ensure that they meet the District’s standards and provide non-discriminatory, accessible and affordable health insurance for our residents.”

The Department reviewed proposed 2020 health plan rates from the four insurance companies. The new rates were approved after the Department considered the input received from insurers, government and non-profit organizations and the testimonies provided by consumers and actuaries during two public hearings. At an August 22 hearing, actuaries presented their findings and members of the public had an opportunity to share their stories and discuss the proposed 2020 rates.

“The DC Health Benefit Exchange Authority (DCHBX) advocates for the lowest possible premiums for our DC Health Link customers and we thank Commissioner Taylor for considering our recommendations and for approving rate changes that are generally lower than initially proposed by insurers,” said DCHBX Executive Director Mila Kofman, J.D. “We also applaud Commissioner Taylor for hosting public hearings for District residents and small businesses to provide comments on the impact of premium increases.”

DC Health Link open enrollment for individuals and families begins November 1, 2019, and runs through January 31, 2020. Visit DCHealthLink.com or call 1-855-532-5465 for help enrolling.

More information about the approved 2020 health insurance plan rates.

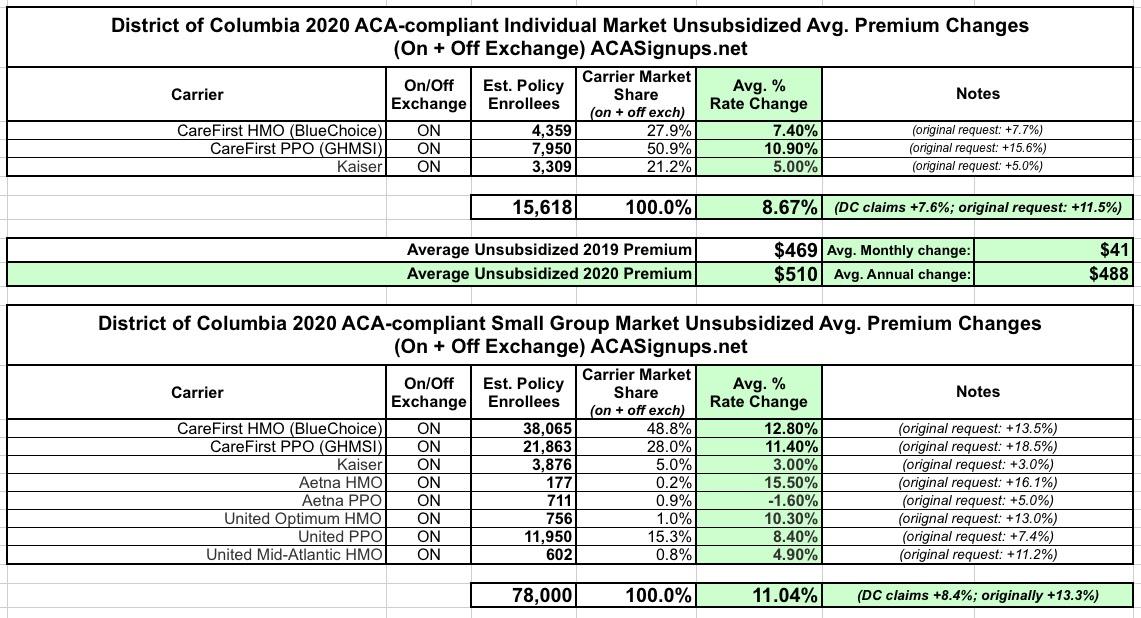

DC has a merged Individual/Small Group risk pool, so the lumping together of the table above makes sense. HOWEVER, when I plug the hard numbers into my own spreadsheet for each market, this is what I get:

Once again, the raw data puts the Individual market increases at 8.7% (down from the original 11.2%) and the small group market at 11.0% (down from 13.9%).

I have no idea what accounts for the difference between my numbers and theirs; I'll post an update if/when I find out.

UPDATE: OK, thanks to an anonymous tipster, I think I have my answer. DC DISB may be simply posting unweighted averages, which would just be silly.

- Individual Market: 7.4% + 10.9% + 5.0% = 23.3%. Divide by 3 carriers and you get 7.8%.

- Small Group Market: Add up all 8 carrier percentages and you get 64.7%. Divide by 8 and you get 8.1%.

Of course, these are still slightly different from what DISB claims in their press release (7.6% and 8.4%), but it's a whole lot closer. It's possible there's some rounding involved.

If you go back to the original requested rates, it's the same thing:

- Individual: 28.3 / 3 = 9.4% (official claim: 9.0%)

- Small Group: 87.7 / 8 = 11.0% (official claim: 10.5%)

So, there you go. If this was coming from a reporter it'd be one thing, but this is an official press release from the DC regulatory department itself. Perhaps they didn't have the effectuated numbers for each carrier at the time and thus were unable to weight the averages, but if so, they should have noted that in the press release.

It's also possible that there's some other factor I'm missing here...I've inquired and will update if I get an explanation.

Advertisement