District of Columbia: Preliminary 2019 ACA rate hike request: 15.5%, "significant impact" from mandate repeal

Mon, 06/04/2018 - 10:11am

Several quick tidbits out of the District of Columbia from the DC Health Benefit Exchange Authority May board meeting:

- Their preliminary 2019 premium rate filings were originally due by May 1st, but this was bumped out until June 1st. Not available publicly yet, however.

- The board voted unanimously to restrict Short-Term, Limited Duration plans to no more than 3 months at a time and to make them non-renewable in order to prevent them from further damaging the ACA individual market. They basically went with the parameters laid out under the newly-signed Maryland law. This won't become official unless the DC Council approves it, however (which I strongly suspect will happen).

- The board also voted unanimously to once again extend the 2019 Open Enrollment Period out to a full 3 months as they did for 2018, by declaring the period from 12/16/18 - 1/31/19 a Special Enrollment Period tacked onto the official 11/1/18 - 12/15/18 OEP.

- Oh, and they also reported the monthly ACA exchange enrollment as of May:

- 17,314 people enrolled in effectuated individual market plans (down just 10% from 19,289 who selected QHPs as of 1/31/18)

- 77,056 people enrolled in effectuated small group market plans (most of these are Congressional staffers)

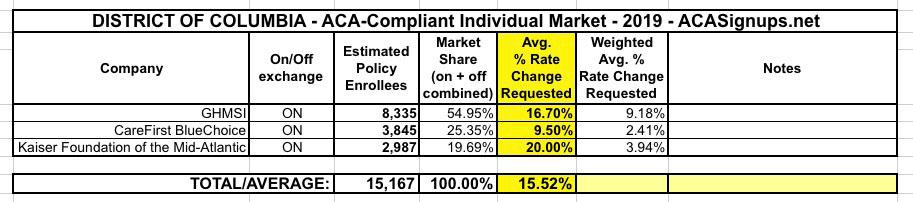

UPDATE: Well, what do you know! It turns out the 2019 rate filings are available for the District of Columbia after all!

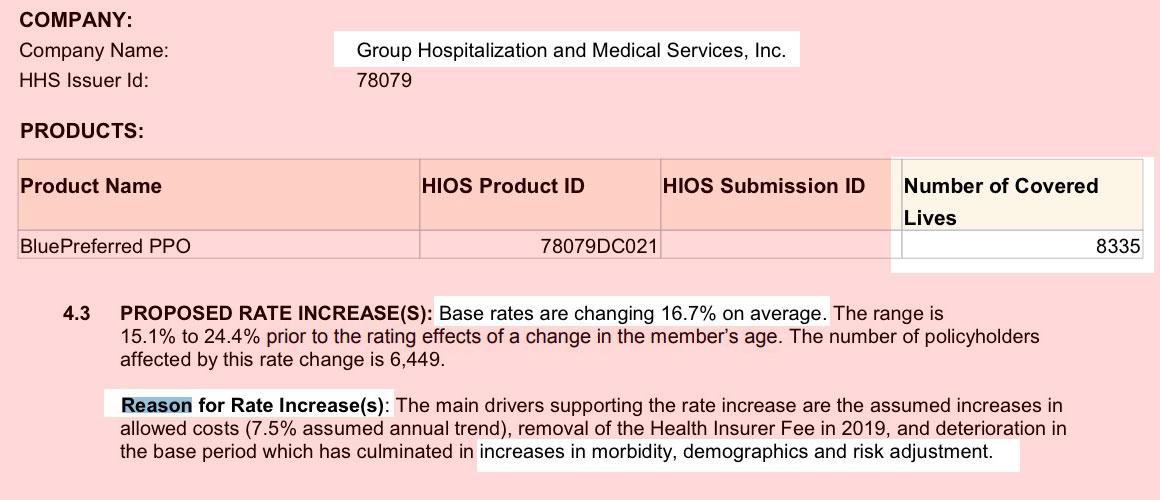

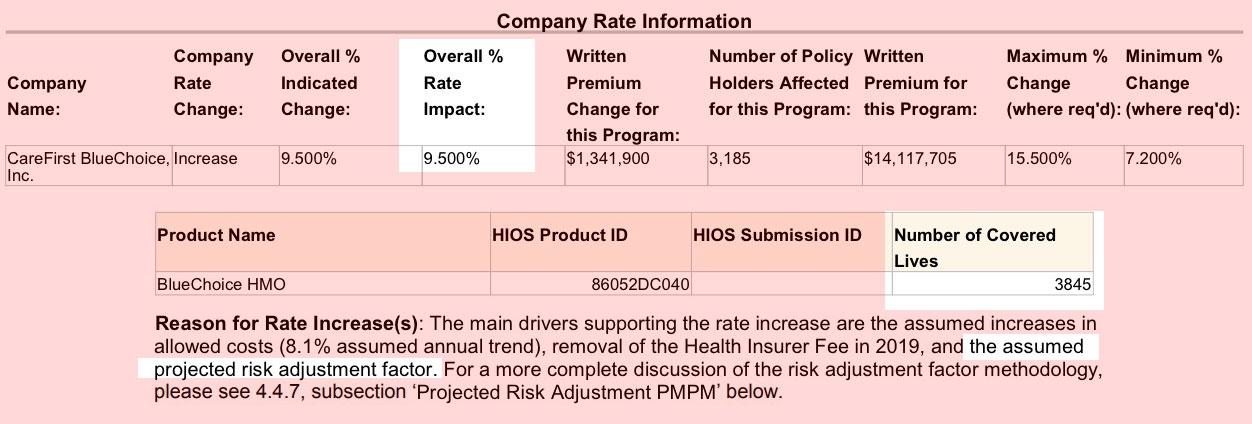

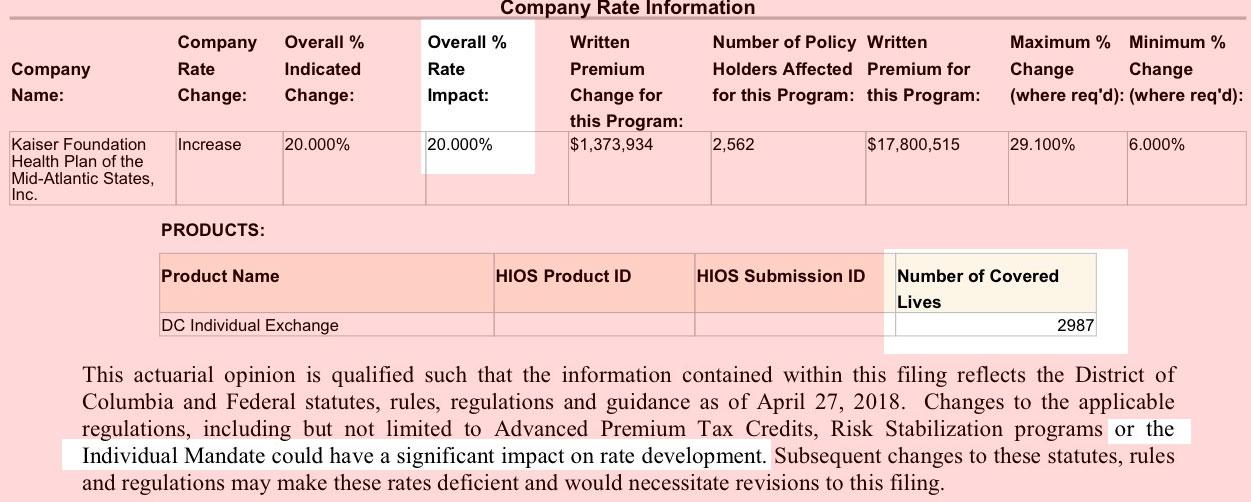

There's only three carriers on the individual market, and the forms seem pretty straightfoward: 15.5% overall (I'm not sure where the "missing" 2,100 enrollees are...perhaps one of the carriers is dropping one of their plans altogether).

None of the carriers go into a lot of detail about the impact of either the ACA mandate being repealed or #ShortAssPlans, but two of them do make vague references and Kaiser (which also happens to be asking for the largest increase) does warn that it had a "significant impact" on their filing.

In the absence of any hard data, I'm once again looking at the Urban Institute analysis, which projected around a 13.6% rate impact overall due specifically to mandate repeal & short-term plan expansion (of course, if the DC Council approves the new regulation, that may change). If so, this suggests that without those factors, DC premiums would only be going up about 2% next year.

Advertisement