HHS Formally Announces launch of 2017 Open Enrollment Window Shopping...

Mon, 10/24/2016 - 2:27pm

***COUNTDOWN TO OPEN ENROLLMENT ***

More Than 70 Percent of Consumers Can Find Marketplace Plans for Less than $75 Per Month

With Start of Window Shopping, Americans Can Now Check Out Options for 2017 Coverage

With window shopping beginning today, Health Insurance Marketplace consumers can now visit HealthCare.gov to check out their options for 2017 coverage in advance of the start of Open Enrollment on November 1. A new report released today shows that 72 percent of Marketplace consumers in states using HealthCare.gov will be able to find plans with a premium of less than $75 per month and 77 percent will be able to find plans with premiums below $100, taking into account financial assistance. The report also shows that consumers will have options, with an average of 30 health insurance plans to choose from.

“Thanks to financial assistance, most Marketplace consumers this year will find plan options with premiums between $50 and $100 per month,” said HHS Secretary Sylvia M. Burwell. “Millions of uninsured Americans qualify for financial assistance, and so could as many as 2.5 million Americans currently paying full price for off-Marketplace coverage. I encourage anyone who might need 2017 coverage to visit HealthCare.gov and check out this year’s options for yourself.”

Thanks in large part to the Marketplace, in early 2016, the share of Americans without health insurance fell to 8.6 percent, the lowest level in our nation’s history. This year’s Open Enrollment offers the chance to build on that progress and further improve access to care and financial security.

Financial Assistance and Shopping Help Keep Coverage Affordable

Eighty-five percent of current Marketplace consumers receive tax credits that bring down the cost of coverage, and, nationwide, about the same percentage of Marketplace-eligible uninsured Americans also have incomes that could qualify them for tax credits. In addition, an estimated 2.5 million people currently paying full price for health insurance in the off-Marketplace individual market could be eligible for tax credits if they purchase 2017 coverage through the Marketplace.

Tax credits increase dollar-for-dollar with the cost of a consumer’s benchmark plan, so they protect the large majority of consumers from rate increases. For example, a 27-year-old in Dallas, Texas with an income of $25,000 paid $143 per month to purchase the benchmark (second-lowest cost silver) plan in 2016. For 2017, that same 27-year-old would pay almost the exact same amount for benchmark coverage, despite a premium increase of $16 per month, because tax credits also increase to compensate.

In addition to financial assistance, shopping helps keep coverage affordable for consumers. If every returning consumer nationwide selected the lowest-cost plan within the same metal level they picked last year, average premiums paid (taking into account financial assistance) would fall by $28 per month – 20 percent – compared to 2016. In fact, many consumers do not choose the lowest-cost plan available, which is why it’s important that shopping also lets consumers compare plans based on factors like provider network, prescription drug coverage, and total out-of-pocket costs. But this calculation confirms that affordable options for 2017 coverage are available to consumers who choose to shop around to find a better deal.

This year, HealthCare.gov consumers will have the option to choose from an average of 30 plans. Like last year, there will be an average of 10 plans per issuer. Four out of five (79 percent of) consumers will also be able to choose between multiple issuers, and all consumers will be able to choose among plans with different combinations of premiums, out-of-pocket costs, networks of hospitals and physicians, and prescription drug coverage options. For people with employer-sponsored health insurance, plan choice is typically narrower; for example, in 2015, 30 percent of people with employer coverage had only one plan option.

As the Marketplace Goes Through a Transition Year, Experiences Vary Widely Across States

Through 2016, Marketplace rates remained well below initial projections from the independent Congressional Budget Office, and well below the cost of comparable coverage in the employer market. Nationwide, average Marketplace premiums for 2017 are increasing more than they have in the past two years. Even with these adjustments, premiums remain roughly in line with projections issued by the Congressional Budget Office during the debate over the Affordable Care Act (ACA).

Adjustments this year reflect issuers bringing their rates in line with observed costs, now that two years of data are available. In addition, some of the ACA’s programs designed to support the new market in its early years are ending this year, putting additional one-time pressure on premium growth. Issuers are continuing to adapt to a new market that looks very different than it did before the ACA: one where they compete based on price and quality, rather than by finding the healthiest customers. Efforts to undermine the ACA, such as certain states’ decisions not to expand Medicaid and Congressional actions to block funding for the law, contribute to higher premiums as well. And some states have long faced unique challenges in reining in health care costs.

For the median HealthCare.gov consumer, the benchmark second-lowest silver plan premium is increasing by 16 percent this year, before taking into account the effects of financial assistance; that is, half of HealthCare.gov consumers are seeing increases less than, and half greater than, 16 percent. But experiences across states vary widely. For example, in Arkansas, Indiana, Michigan, Nevada, New Hampshire, New Jersey, North Dakota, and Ohio, as well as in California and Massachusetts (which do not use the HealthCare.gov platform), benchmark premiums are rising by 7 percent or less. In most of these states, Marketplaces are also strongly competitive, and several have seen issuers expanding their service areas, as with Molina in Ohio or Humana in Michigan. These examples illustrate that there are parts of the country where Marketplaces are already maturing, reaching stable price points, and enjoying robust competition.

Conversely, some states are experiencing high benchmark premium growth, resulting in a HealthCare.gov average higher than the median increase. A number of the states in this group, including Arizona, Hawaii, Illinois, Kansas, and Pennsylvania, are places where 2016 rates were especially far below the national average or especially far below the cost of comparable coverage in the employer market.

Fortunately, financial assistance and the ability to shop around for coverage protect most consumers across the country from headline rate increases. “Before the ACA, many consumers were unable to get health coverage at all, and the individual market offered no easy way to shop and compare plans,” said Kevin Counihan, CEO of the Health Insurance Marketplace. “Because of the Marketplace, consumers can shop around to find coverage that fits their needs and get tax credits to help pay for it. Thanks to shopping and financial assistance, consumers will continue to have robust options for quality, affordable coverage for 2017, even in places where premium increases are high.”

The Affordable Care Act Is Strengthening Coverage, and Improvements Could Drive Further Progress

The Marketplace is one of many ways the ACA continues to improve health care affordability, access, and quality.

Affordability. The latest available data show employer premiums are continuing to rise at the low rates observed since the ACA was enacted. This year, the average family premium for the more than 150 million Americans with employer coverage is $3,600 lower than it would be if pre-ACA premium growth had continued.

Access. More than 20 million American adults have gained coverage as a result of provisions of the Affordable Care Act. In addition, more than 3 million children have gained coverage since 2008, thanks in large part to the ACA and improvements to the Children’s Health Insurance Program.

Quality. For those who already had coverage, the ACA provided new protections, including guaranteed limits on out-of-pocket costs, no limits on annual or lifetime coverage, and preventive services without cost sharing. The ACA is also strengthening health care quality, with large drops in patient harms and preventable hospital readmissions for Medicare beneficiaries.

“Our nation has made historic progress under the ACA, and now we want to build on that progress to further improve affordability, access, and quality,” said Secretary Burwell.

The President has taken a number of steps to improve the ACA, and thinks we can do even more, such as: expanding Medicaid in states that have declined to do so; providing more tax credits for middle-income families and young adults to further improve affordability; adding a public plan fallback to give people more options in places where there still are just not enough insurers to compete; and supporting innovation by states. But this Open Enrollment, we are focused on getting as many uninsured people covered as we can.

Open Enrollment, which starts November 1 and ends on January 31, 2017, provides another opportunity for Americans to find affordable coverage for them and their families. Learn more on HealthCare.gov.

**********

USER’S GUIDE: TIPS FOR MEDIA USING WINDOW SHOPPING TO UNDERSTAND MARKETPLACE OPTIONS

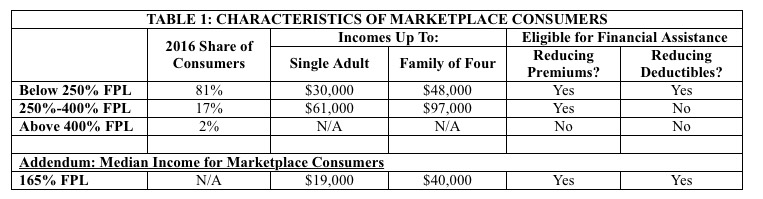

To make shopping easier for consumers, HealthCare.gov asks for information about expected family income and then shows consumers plan information – including premiums, deductibles, and out-of-pocket limits – that reflects the financial assistance they qualify for. To use window shopping to understand consumers’ choices, it is important to search options for families with incomes typical of Marketplace consumers. Premiums and deductibles displayed without inputting income are not representative of Marketplace consumers’ options.

The table below shows the distribution of Marketplace consumers in 2016. The typical Marketplace consumer has an income of 165 percent of the federal poverty level (FPL): about $40,000 for a family of four, and $19,000 for a single adult. Consumers at these income levels qualify for financial assistance that reduces premiums as well as deductibles and other cost sharing.

Getting Ready for Open Enrollment

We’re putting the finishing touches on our plans for Open Enrollment. Between now and November 1, you’ll see a series of announcements from us about what’s new, what’s better, and what to expect during this Open Enrollment – including new tools for consumers, new outreach tactics and targeting strategies, and more information about continued access to affordable coverage. Today’s announcement is the fourth in this series. The first, on September 27th, focused on outreach to young adults; the second, on October 4th, focused on outreach to off-Marketplace consumers eligible for financial help; and the third, on October 13th, focused on new outreach strategies and tactics.

Americans can sign up for affordable health plans that meet their needs and their budgets at HealthCare.gov or their state Marketplace websites beginning November 1. Open Enrollment runs through January 31, 2017. Health coverage can start as soon as January 1, 2017 for consumers who sign up by December 15, 2016.

Advertisement