How To Give A Healthcare Wonk Heartburn

Thu, 07/30/2015 - 11:38am

Back in June, I was both geeked and severely disappointed at the same time by Healthcare.Gov's brand-new Rate Review searchable database for listing the policy premium change requests by the hundreds of insurance companies operating both on and off of the ACA exchanges.

On the plus side:

- You can search by either ACA-compliant or "Transitional" policies (although there don't seem to be any transitional listing listed, and these won't be an issue after next year anyway)

- You can search by all 50 states as well as DC...and even the U.S. territories such as Guam, American Samoa etc (although the territories aren't covered by the ACA exchanges anyway)

- You can search by company name or "NAIC Number"

- You can search by filing date range (01/01/2016 is the only one to focus on at the moment)

- You can filter things out by individual or small group policies, or by other text-based criteria

- You can sort the filings by company name, issuer ID, product name, submission date, requested rate increase, approved rate increase or status (basically, active or withdrawn)

- The details for each filing are laid out in a consistent, neat, clean format, with the requested % change clearly listed, and in many cases, the actual number of covered lives impacted by the rate change are included.

The points bold-faced above are obviously of the greatest concern to me.

However, there's still a few major problems with the RateReview site, most of which I laid out in June:

- The Big One: ONLY requests for increases above 10% are included.

This can lead to an incredibly warped image of the true rate increase picture. Reporters, politicians and other interested parties who search for the rate changes in any state would come away from HC.gov's rate review site assuming that every company is jacking up prices by more than 10%. Not only aren't the <10% requests listed, they're not even referenced to as a footnote; they might as well not even exist as far as this database is concerned.

To use Connecticut as an example, according to the HCgov site, the half-dozen companies listed there are the only ones offering individual policies, with increases ranging from 10.09% to 32.9%...when, in fact, the actual weighted average from the eleven companies selling individual policies in the state is just 5.2%.

As I noted in June, I realize that the HHS Dept. is only required to list the >10% requests legally, in order to allow for public comment and regulatory review, but they could at least list the other ones. Not doing so is just shooting yourselves in the foot PR-wise (not to mention being kind of unfair to the companies which requested nominal hikes or, in some cases, are even lowering their prices).

- While some of the actual requests include the number of covered lives impacted, not all of them do...and there doesn't appear to be any rhyme or reason involved. While there are specific fields at the top for some data (Effective Date, Review Status, Requested Increase, Includes Exchange Plans, etc), the actual number of people/members/covered lives is sometimes included in the "justification" text at the bottom, but sometimes isn't, and is worded differently by each company

One other thing making me tear my hair out:

- Some of the companys have multiple filings for different products with different rate requests...but the same number of "covered lives" for each.

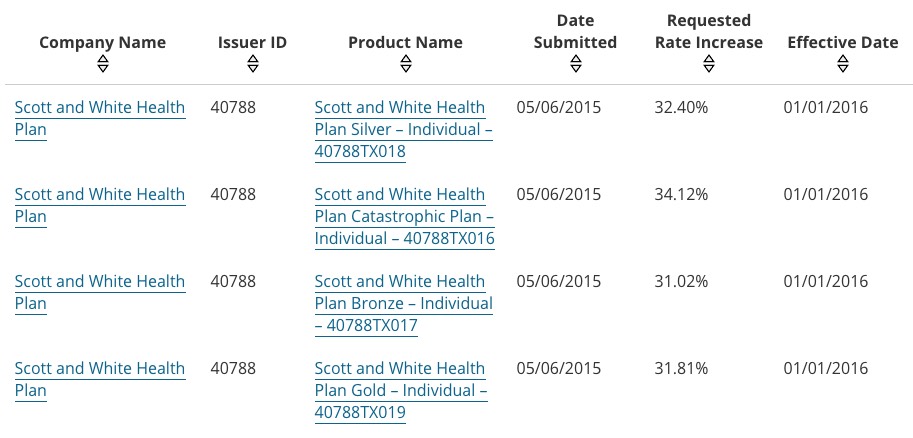

Here's what I'm talking about: If you go to the rate review site, select ACA Compliant > Texas > 01/01/2016 and then filter it to only list active filings, you'll see not one, but four listings for "Scott & White Health Plan":

Now, obviously they've decided to break out their requests by metal level: Silver, Bronze, Gold & Catastrophic (apparently S&W either isn't offering Platinum...or if they are, asked for a <10% increase, which goes back to the first problem above).

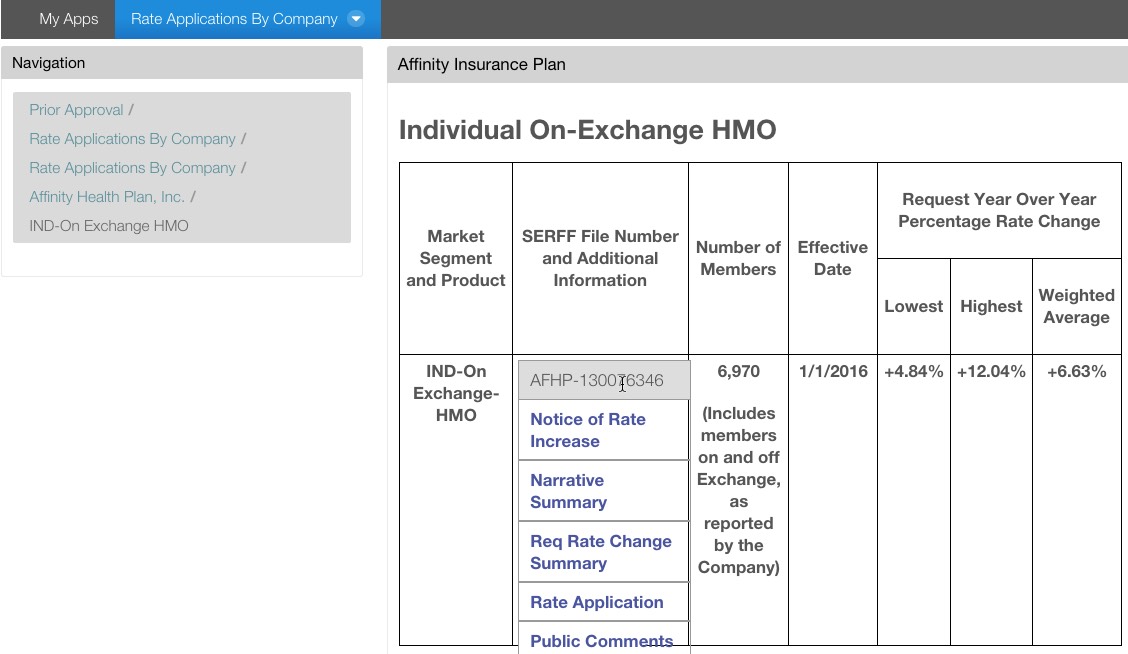

However, when you click on any of the actual requests, here's the text:

The Scott& White Health Plan is requesting an average rate increase of 32.3% to the Individual HMO Rating Pool. There are 24,294 covered individuals as of January 2015. 10.0% of the 32.3% increase is due to health care cost inflation, 14.3% of the increase pertains to changes in Risk Adjustment and Reinsurance assumptions, 2.7% is due to changes in fees, and the remaining 5.3% is due to actual and expected unfavorable experience.

Note that none of the 4 individual metal level requests here actually are 32.3%; they're each either slightly higher or lower. It's also extremely unlikely that exactly 24,294 people happened to enroll in each of the 4 metal levels. Obviously what happened here is that Scott & White's overall average request is 32.3% for all of their metal levels, and they have 24,394 people enrolled total across all 4 levels.

That's fine...but why not actually say so? Either have a single filing of 32.3%, or give the covered lives tally for each individual filing. Don't mix and match!

In any event, these are all fixable issues. Hopefully they'll add all of the filings (regardless of whether they're >10%, <10% or even reductions) next year, and will make the "number of covered lives" an official, required field. We'll see.

In the meantime, much of the missing filing data can be found at the individual state insurance department / commissioner websites. Unfortunately, the quality, comprehensiveness and ease-of-use of these sites ranges from fantastic to migraine-inducing. Here's a roundup of a few to give you an idea:

NEW YORK:

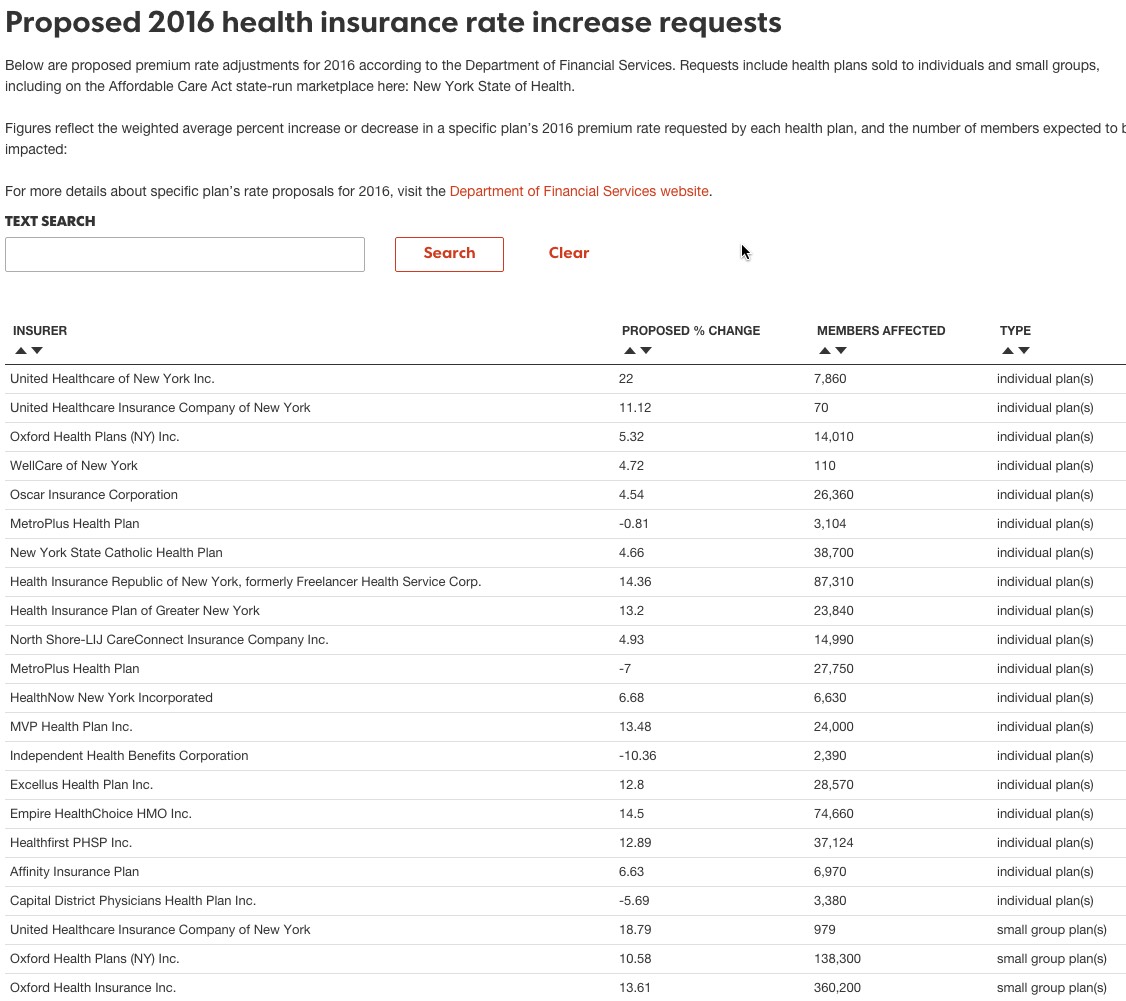

The official Dept. of Financial Services website is kind of clunky to use (you have to do a lot of drilling-down to get to each individual company, one at a time), but once you get there, it's pretty cut & dried, and lists the most crucial info up front:

Notice how it tells you whether it's ON or OFF exchange, HMO or PPO, the WEIGHTED average increase (that's important) and, crucially, the number of COVERED LIVES, in a simple table. Yay! You also have the option of clicking through to the actual PDF forms, but that's exactly what I'm trying to avoid.

However, the Gannett NY News Organizations have taken this one step further with their fantastic NYDatabases.com portal. Check this out:

Now THAT'S what I'm talking about! Every company neatly listed with the proposed % change, number of people impacted and the type (individual/small group), all sortable. If every state had a site like this, it would make my job (as well as that of many healthcare reporters) much, much easier.

FLORIDA:

Florida's Office of Insurance Regulation site includes what should be an easy-to-use Forms/Rate Filing searchable database. Here's the problem, though: There are two ways to search it: "Quick" or "Advanced". The Quick Search requires you to enter the individual company name...which can be a problem when you have a company operating under multiple, very similar names in different areas. For instance, here's what happens if you search for "Humana":

Note that there's another 5-6 similar listings in addition to these. Which one do I want? Is "Humana Health Plan of Florida Inc." the same as "Humana Insurance Company"? How about "Humana Medical Plan Inc."? Assuming that each of these are a separate division (and have separate filings), why are there 2 or more of some, and which is the "correct" one?

Then, when I do pick one, they have a comprehensive listing. The good news is that I can filter it down to just 2016, just rates, just individual policies and so on...but in some cases, there's still multiple listings. Finally, again, some filings include the covered lives while others don't (apparently in Florida, that's considered a "trade secret" by some companies).

TEXAS:

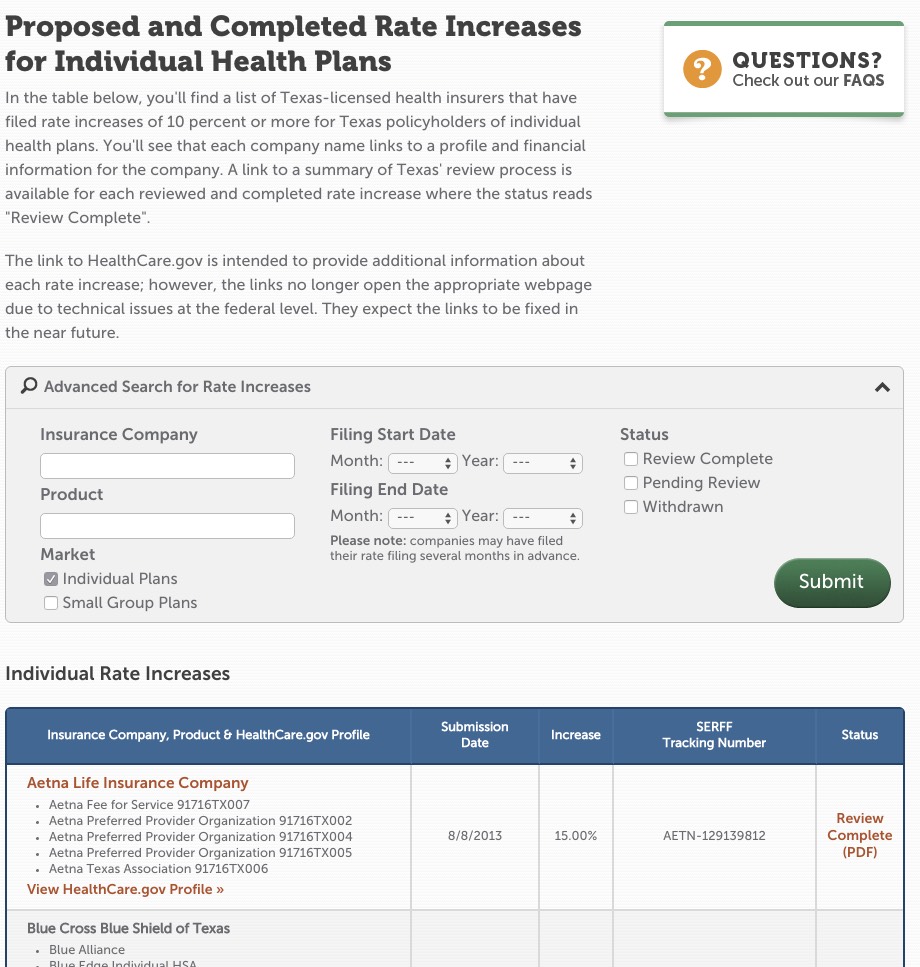

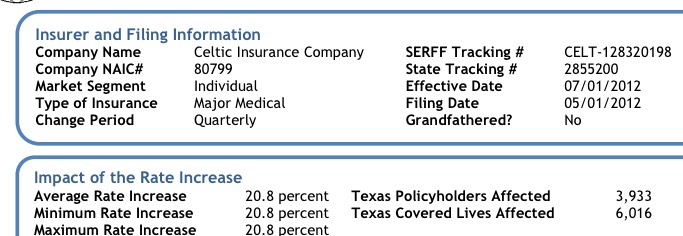

You would probably think that Texas, being a deep-red states which despises Obamacare and isn't exactly known for being "public service friendly", would have a crappy insurance review website.

The good news is that it's actually pretty slick, comprehensive and easy to use! It loads quickly, has a logical layout, lets you search by company, filing date, individua/sm. group and status, and lists them all by company. The individual filings even state exactly how many covered lives are impacted (and as a bonus, distinguishes these from the number of policyholders). Excellent all around!

The bad news is that 1) as noted in the first screenshot above, they still only list filings over 10% (making it no more useful than HC.gov) and 2) it's horribly out of date; the most recent filing included is from 2013. I assume that they decided to stop bothering and let the HC.gov site take over for 2014 and beyond...which would be fine, if HC.gov actually included all of the filings and listed the covered lives affected for every filing.

ALABAMA:

Hmmm...well, here's their Insurance Dept. website. Under "Consumers" is a link for "Health Insurance Plans for Individuals" which takes you to...a PDF listing the various companies offering individual market policies, which I guess is handy (although it hasn't been updated since October 1, 2013...the same day the ACA exchanges launched...hmmmm....)

There's also a link to Alabama's "Health Insurance Website". Hmmmm...it's not there.

If you go to the "Rate Bulletin Search" it looks promising...except:

The Alabama Department of Insurance will continue to place Home Owners, Automobile, Worker Comp and Medical Malpractice manuals on this page. All other manuals can be viewed using SERFF's Public Access.

Ah-hah! Here we go: SERFF's Public Access database! Let's try that out. First I'll give the "Health Plan Binder" option a shot...

Oh. Never mind. OK, let's go back to the "general" SERFF search. At first this looks pretty straightforward...

But then comes the "type of insurance" drop-down list...with over 100 options to choose from.

- A01 Annuities - Assumption Agreement

- A02.1G Group Annuities - Deferred Non-Variable and Variable

- A02.1I Individual Annuities- Deferred Non-Variable and Variable

- A02G Group Annuities - Deferred Non-variable

- A02G Group Annuities - Deferred Non-variable Benefit

- A02I Individual Annuities - Deferred Non - Variable

- A02I Individual Annuities- Deferred Non-Variable

- A03G Group Annuities - Deferred Variable

- A03G Group Annuities - Deferred Variable Benefit

- A03I Individual Annuities - Deferred Variable

- A04G Group Annuities - Immediate

- A04I Individual Annuities - Immediate

- A05G Group Annuities - Immediate Non-Variable

- A05I Individual Annuities - Immediate Non - Variable

- A05I Individual Annuities- Immediate Non-Variable

- A06.1G Group Annuities - Immediate Non-Variable and Variable

- A06.1I Individual Annuities- Immediate Non-Variable and Variable

- A06G Group Annuities - Immediate Variable

- A06G Group Annuities - Immediate Variable Benefit

- A06I - Individual Annuities - Immediate Variable

- A06I - Individual Annuities - Immediate Variable Benefit

- A06I Individual Annuities - Immediate Variable

- A07G Group Annuities - Special

- A07I Individual Annuities - Special

- A08G Group Annuities - Unallocated

- A10 Annuities - Other

- Annuity

- CR02G Group Credit - Credit Disability

- CR02I Individual Credit - Credit Disability

- CR03G Group Credit - FMLA

- CR04G Group Credit - Life

- CR04I Individual Credit - Life

- CR07 Credit - Other

- H01 Health - Assumption Agreement

- H02G Group Health - Accident Only

- H02I Individual Health - Accident Only

- H03G Group Health - Accidental Death & Dismemberment

- H03I Individual Health - Accidental Death & Dismemberment

- H04 Health - Blanket Accident /Sickness

- H05 Health - Champus /Tricare Supplement

- H06 Health - Conversion

- H07G Group Health - Specified Disease - Limited Benefit

- H07I Individual Health - Specified Disease - Limited Benefit

- H08I Individual Health - Intensive Care - Limited Benefit

- H09G Group Health - Organ & Tissue Transplant - Limited Benefit

- H10G Group Health - Dental

- H10I Individual Health - Dental

- H11G Group Health - Disability Income

- H11I Individual Health - Disability Income

- H12 Health - Excess/Stop Loss

- H13I Individual Health - Short Term Care

- H14G Group Health - Hospital Indemnity

- H14I Individual Health - Hospital Indemnity

- H15G Group Health - Hospital/Surgical/Medical Expense

- H15I Individual Health - Hospital/Surgical/Medical Expense

- H16G Group Health - Major Medical

- H16I Individual Health - Major Medical

- H17G Group Health - Prescription Drug

- H18G Group Health - Sickness

- H18I Individual Health - Sickness

- H19G Group Health - Travel

- H19I Individual Health - Travel

- H20G Group Health - Vision

- H20I Individual Health - Vision

- H21 Health - Other

- HOrg02G Group Health Organizations - Health Maintenance (HMO)

- HOrg02I Individual Health Organizations - Health Maintenance (HMO)

- HOrg03 Health Organizations - Other

- Health

- L01 Life - Assumption Agreement

- L02I Individual Life - Endowment

- L03G Group Life - Special

- L03I Individual Life - Special

- L04G Group Life - Term

- L04I Individual Life - Term

- L05G Group Life - Universal

- L05I Individual Life - Universal

- L06G Group Life - Variable

- L06I Individual Life - Variable

- L07G Group Life - Whole

- L07I Individual Life - Whole

- L08 Life - Other

- L09G Group Life - Flexible Premium Adjustable Life

- L09I Individual Life - Flexible Premium Adjustable Life

- LTC01 Long Term Care - Assumption Agreement

- LTC02I Individual Long Term Care - Home Care Only

- LTC03G Group Long Term Care

- LTC03I Individual Long Term Care

- LTC04G Group Long Term Care - Nursing Home

- LTC04I Individual Long Term Care - Nursing Home

- LTC05.1I Individual Assisted Living Care

- LTC05G Group Long Term Care - Nursing Home & Home Care

- LTC05I Individual Long Term Care - Nursing Home & Home Care

- LTC05I Individual Long Term Care - Nursing Home & Home Health Care

- LTC06 Long Term Care - Other

- Life

- ML01 Multi-Line - Assumption Agreement

- ML02 Multi-Line - Other

- MS01 Medicare Supplement - Assumption Agreement

- MS02G Group Medicare Supplement - Pre-Standardized

- MS02I Individual Medicare Supplement - Pre-Standardized

- MS04G Group Medicare Supplement - Medicare Select

- MS04I Individual Medicare Supplement - Medicare Select

- MS05G Group Medicare Supplement - Standard Plans

- MS05I Individual Medicare Supplement - Standard Plans

- MS06 Medicare Supplement - Other

- MS07G Group Medicare Supplement - Medicare Select 2010

- MS07I Individual Medicare Supplement - Medicare Select 2010

- MS08G Group Medicare Supplement - Standard Plans 2010

- MS08I Individual Medicare Supplement - Standard Plans 2010

- MS09 Medicare Supplement - Other 2010

The good news is that you can choose more than one; if you stick to just the "Health" group it cuts it down like so:

- H01 Health - Assumption Agreement

- H02G Group Health - Accident Only

- H02I Individual Health - Accident Only

- H03G Group Health - Accidental Death & Dismemberment

- H03I Individual Health - Accidental Death & Dismemberment

- H04 Health - Blanket Accident /Sickness

- H05 Health - Champus /Tricare Supplement

- H06 Health - Conversion

- H07G Group Health - Specified Disease - Limited Benefit

- H07I Individual Health - Specified Disease - Limited Benefit

- H08I Individual Health - Intensive Care - Limited Benefit

- H09G Group Health - Organ & Tissue Transplant - Limited Benefit

- H10G Group Health - Dental

- H10I Individual Health - Dental

- H11G Group Health - Disability Income

- H11I Individual Health - Disability Income

- H12 Health - Excess/Stop Loss

- H13I Individual Health - Short Term Care

- H14G Group Health - Hospital Indemnity

- H14I Individual Health - Hospital Indemnity

- H15G Group Health - Hospital/Surgical/Medical Expense

- H15I Individual Health - Hospital/Surgical/Medical Expense

- H16G Group Health - Major Medical

- H16I Individual Health - Major Medical

- H17G Group Health - Prescription Drug

- H18G Group Health - Sickness

- H18I Individual Health - Sickness

- H19G Group Health - Travel

- H19I Individual Health - Travel

- H20G Group Health - Vision

- H20I Individual Health - Vision

- H21 Health - Other

- HOrg02G Group Health Organizations - Health Maintenance (HMO)

- HOrg02I Individual Health Organizations - Health Maintenance (HMO)

- HOrg03 Health Organizations - Other

- Health

But...now what? OK, I can cut it down further by removing "Group", as well as removing "Dental", "Vision" and "Disability" I suppose...

- H01 Health - Assumption Agreement

- H02I Individual Health - Accident Only

- H03I Individual Health - Accidental Death & Dismemberment

- H04 Health - Blanket Accident /Sickness

- H05 Health - Champus /Tricare Supplement

- H06 Health - Conversion

- H07I Individual Health - Specified Disease - Limited Benefit

- H08I Individual Health - Intensive Care - Limited Benefit

- H12 Health - Excess/Stop Loss

- H13I Individual Health - Short Term Care

- H14I Individual Health - Hospital Indemnity

- H15I Individual Health - Hospital/Surgical/Medical Expense

- H16I Individual Health - Major Medical

- H18I Individual Health - Sickness

- H19I Individual Health - Travel

- H21 Health - Other

- HOrg02I Individual Health Organizations - Health Maintenance (HMO)

- HOrg03 Health Organizations - Other

- Health

...but that still leaves me with nearly 20 categories. If I try selecting just "Health" (last one) I get no results. So...what do I do now?

Anyway, I'll leave it at that. Obviously it would take forever to do an analysis of all 50 state sites. Some are better/easier to use/more comprehensive than others; this is just a taste.

The bottom line is this: If you're wondering why I haven't plugged in all 50 states into the "Where Things Stand" table, this should give some insight. Yeesh.

Advertisement