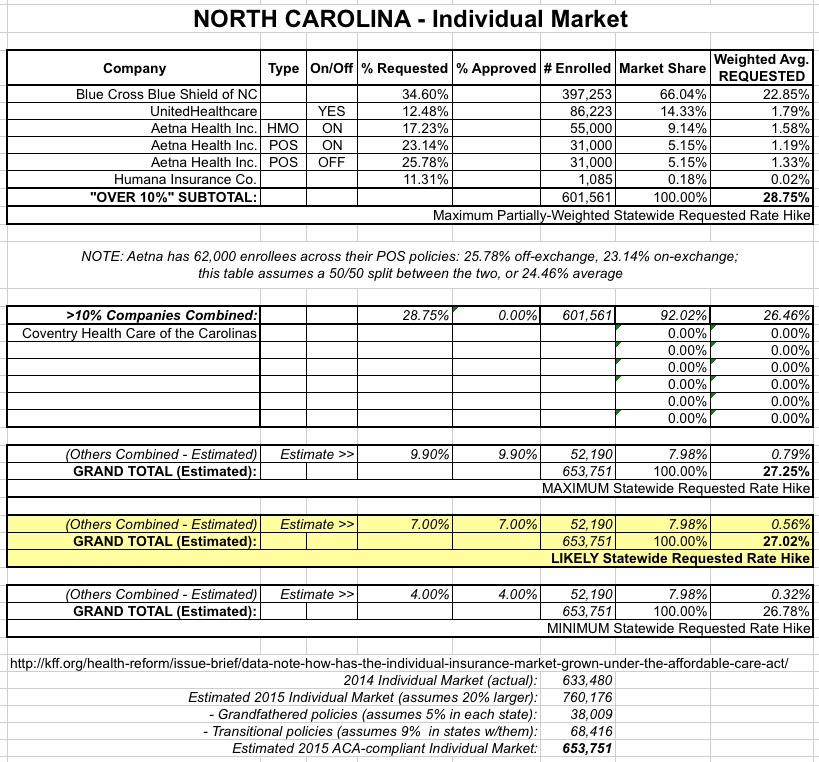

Way back in May, Blue Cross Blue Shield of North Carolina submitted their initial 2018 rate requests to the state insurance department, and noted at the time that they'd normally only be requesting an 8.8% average rate increase...but that due specifically to Donald Trump's threat to cut off CSR reimbursement payments, they were asking for a 23.3% increase instead. I noted that this meant that about 60% of their increase request was caused by Trump's CSR threat.

Then, in August, they gave a somewhat more positive news update: They were lowering their requested rate hike to 14.1%. Basically, their latest numbers had come in and the balance sheet was doing quite a bit better than they had previously thought:

Blue Cross said May 25 that the 22.9 percent rate increase was based on the subsidies ending, along with claims data from the first quarter of 2017. It projected an 8.8 percent rate increase with the subsidies remaining in place.

Quick recap: As of 2013, the pre-ACA individual market consisted of around 10.7 million people. The vast majority of the policies these folks were enrolled in were not ACA-compliant for one reason or another, including not covering one or more of the 10 Essential Health Benefits (EHBs) required by the ACA, having annual/lifetime caps on benefits or any number of other reasons.

Under ACA regulations, non-compliant policies which people were enrolled in prior to March 2010 (when President Obama signed the ACA into law) were grandfathered in...that is, insurance carriers could continue to offer them to existing enrollees for as long as they wanted to, and existing enrollees could stay on them for as long as they wished, but they couldn't be offered to anyone else, and once a current enrollee dropped out of a grandfathered plan they aren't allowed to rejoin it later on. The number of "grandfathered" enrollees has gradually declined since 2013, of course, as people either move to other coverage, die off (hey, it happens) or the carriers decide to discontinue the policies altogether.

In late May, I noted that Blue Cross Blue Shield of North Carolina, which holds a near monopoly on the individual market in NC with around 95% of total enrollment, had submitted an initial rate hike request for 2018 averageing 22.9% overall. What was remarkable at the time is that while most carriers were pussyfooting around using euphamisms about the reasons for their excessive increase requests, BCBSNC was among the first to come right out and state point-blank that it's the Trump Administration's deliberate sabotage of the market--primarily via the threats to cut off CSR payments and to not enforce the individual mandate--that are responsible for over 60% of the increase. This is from their blog, not mine:

For 2017, North Carolina's unsubsidized, weighted average individual market rate hikes came in at around 24.2%. With carriers like Aetna, United Healthcare, Humana and Celtic all dropping out of the NC exchange market, there wasn't much math to do in order to find a weighted average: The only individual market carriers left were Blue Cross Blue Shield of NC, Cigna and "National Foundation Life Insurance", which is basically a non-entity shell company related to "Freedom Life", the less said about the better. Since Cigna only had around 1,200 indy market enrollees at the time (less than 0.5% of the total market share), that pretty much left BCBSNC as the only game in town, so their 24.3% hike was the whole shebang for the state.

While I've been embroiled in the sturm und drang at the national level, Louise Norris of healthinsurance.org has been reporting on some important stuff happening at the state level:

As of 2017, Hawaii no longer has a SHOP exchange for small businesses. The State Department of Labor and Industrial Relations has an FAQ page about this.

...Hawaii’s waiver aligns the ACA with the state’s existing Prepaid Health Care Act. Under the Prepaid Healthcare Act, employees who work at least 20 hours a week have to be offered employer-sponsored health insurance, and can’t be asked to pay more than 1.5 percent of their wages for employee-only coverage (as opposed to 9.69 percent under the ACA in 2017).

Blue Cross Blue Shield of North Carolina originally requested an 18.8% rate hike back in June, but after the Aetna pullout, they revised their request upwards to 24.3%. Cigna, which is expanding onto the ACA exchange next year, followed suit by bumping up their request from 7% to 15%.

I haven't seen any formal announcement from the NC Dept. of Insurance yet, but BCBSNC just posted the following blog entry announcing their 2017 rates...and it certainly looks like the 24.3% request was indeed granted as is:

Blue Cross and Blue Shield of North Carolina customers purchasing ACA plans on the individual market will see an average increase of 24.3 percent in their premiums for 2017, compared to this year’s rates. That’s higher than our original rate filing back in May (an 18.8 percent increase).

For the two carriers that are expected to participate in the exchange in 2017, the proposed average rate hikes for 2017 are:

Blue Cross Blue Shield of North Carolina: 18.8 percent 24.3 percent (new rates were filed in late August)

Cigna: 7 percent (based on current off-exchange plans) 15 percent (new rates were filed)

Aetna had proposed an average rate increase of 24.5 percent, but that is no longer applicable for exchange enrollees, as Aetna’s plans will not be available in the North Carolina exchange in 2017.

North Carolina's individual market, which only had 5 carriers participating to begin with this year, suffered a double blow recently when both UnitedHealthcare (155,000 enrollees) and Humana (3,272 enrollees) announced that they were dropping out of the market entirely next year (Celtic is also leaving the state, but they have literally just 1 person enrolled state-wide anyway). Fortunately, nature abhors a vacuum, so Cigna Health & Life Insurance decided to join the exchange for 2017. Cigna is already selling off-exchange individual policies, but only has fewer than 1,300 people enrolled in them at the moment. There's also a carrier called "National Foundation Life Insurance" which is raising rates 17.4%...but doesn't have a single person enrolled at the moment anyway, so I'm not sure what to make of that.

When UnitedHealthcare announced last month that they were making good on their threat last fall to pull out of the individual market in over two dozen states next year, it caused shockwaves across the health insurance industry. It is an important development, as around 800,000 people will be impacted.

When Humana announced last week that they plan on pulling out of the individual market in at least 5 states next year, it was interesting and a bit of a bummer, but not nearly as earthshattering, because only about 25,000 people will have to shop around and find a new carrier.

Today, it is my duty to announce that Celtic insurance has also decided to pull out of the entire individual insurance market (both on and off-exchange) across at least 6 states, including:

Two more health insurers in North Carolina are asking to increase their already-proposed rate increases.

UnitedHealthcare, which had requested an average rate increase of 12.5 percent, now is asking regulators to allow an an average increase of 20.4 percent. The range is 2.5 percent to 50.3 percent.

Humana had requested 11.3 percent and is now asking for an average of 24.9 percent.